Report Overview

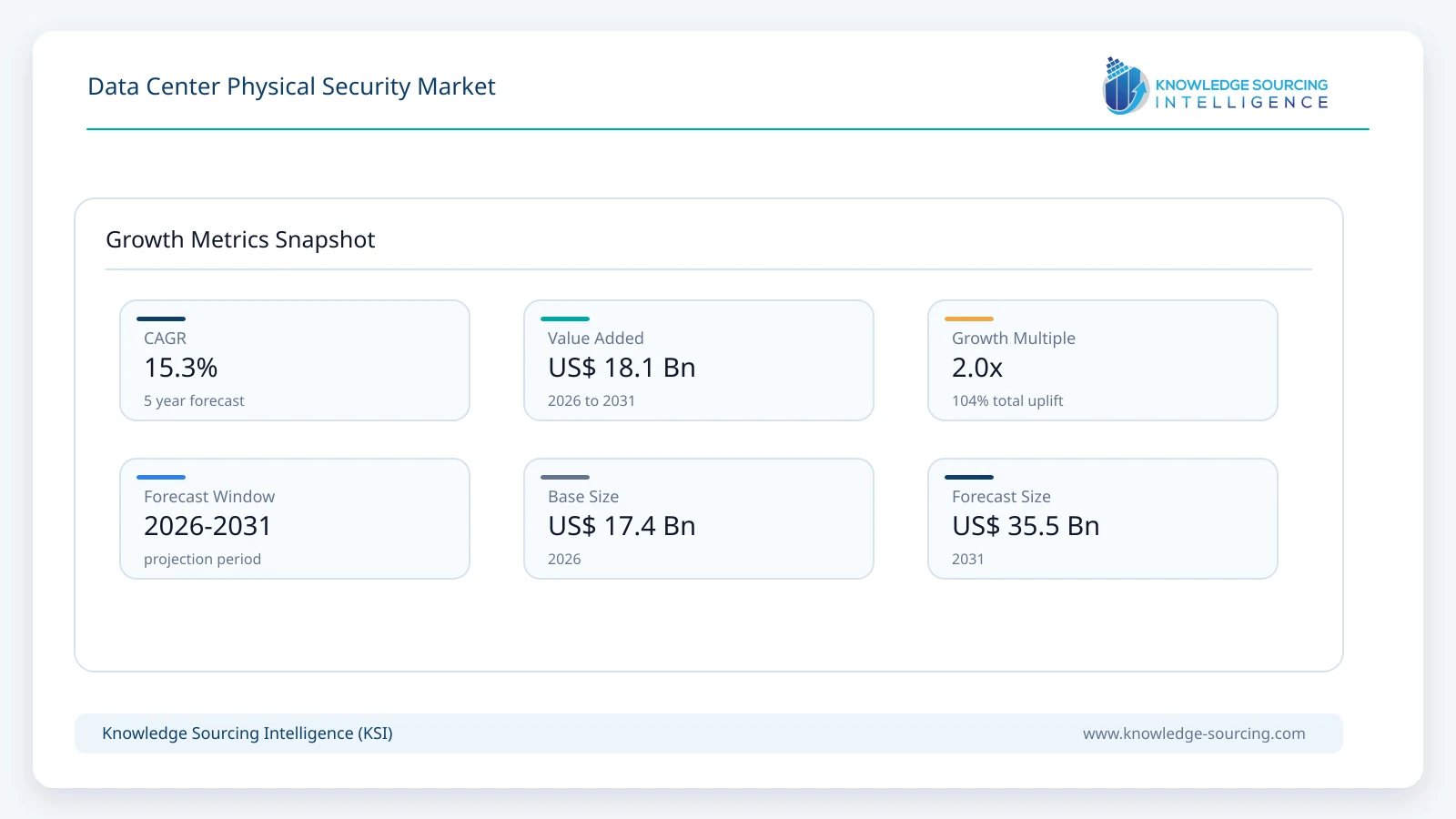

The Data Center Physical Security Market is forecast to grow at a CAGR of 15.30%, reaching USD 35.51 billion in 2031 from USD 17.43 billion in 2026.

Highlights:

- 1Rising investments in hyperscale, colocation, and edge computing infrastructure continue to strengthen demand for integrated physical security systems.

- 2Access control systems remain a commercially important solution category because identity verification forms the foundation of facility security.

- 3Asia Pacific presents substantial long-term opportunities supported by new data center construction and expanding digital infrastructure investments.

- 4AI-assisted video analytics, centralized monitoring platforms, and integrated building management systems are influencing procurement strategies.

- 5Regulatory requirements covering operational resilience, critical infrastructure protection, and information security encourage investment in advanced physical safeguards.

- 6Competition increasingly centers on integrated solutions combining hardware, software, lifecycle services, and global implementation capabilities.

The data center physical security market comprises technologies and services designed to protect critical computing infrastructure, networking equipment, storage systems, and supporting facilities from unauthorized access, theft, sabotage, environmental hazards, and operational disruption. The market includes hardware, software, and managed services covering access control, surveillance, environmental monitoring, and integrated security management across enterprise, colocation, hyperscale, and edge data centers.

Demand for physical security solutions has expanded alongside sustained investment in digital infrastructure. Cloud service providers, colocation operators, financial institutions, telecommunications companies, healthcare organizations, and government agencies continue to expand computing capacity while placing greater emphasis on facility resilience and operational continuity. As data centers become larger and more geographically distributed, owners require multilayered physical protection capable of supporting high equipment density and uninterrupted operations.

Procurement decisions are increasingly influenced by lifecycle cost, regulatory compliance, interoperability with building management systems, and centralized monitoring capabilities rather than standalone hardware performance. Buyers seek integrated platforms that combine identity management, intelligent surveillance, environmental sensing, visitor management, alarm management, and incident reporting within a unified operational framework. This purchasing behavior has encouraged suppliers to expand software capabilities alongside traditional security hardware.

Industry structure reflects participation from building automation companies, access control specialists, surveillance technology providers, networking vendors, and integrated security service providers. Hardware remains an essential revenue contributor because every new facility requires physical barriers, readers, cameras, controllers, locks, and environmental sensors. Software and recurring services, however, generate increasing long-term revenue through maintenance contracts, cloud-based monitoring, cybersecurity updates, compliance auditing, and managed security operations.

Facility modernization also supports replacement demand. Older enterprise data centers frequently require upgrades to biometric authentication, IP-based surveillance, intelligent video analytics, and integrated environmental monitoring to comply with evolving security policies. At the same time, hyperscale and colocation developments specify advanced physical security systems during initial construction, creating opportunities for suppliers capable of supporting large-scale deployments across multiple geographic regions.

Market Drivers

Expansion of Hyperscale and Colocation Infrastructure

Global cloud adoption continues to stimulate construction of large-scale data centers that require comprehensive physical protection from the planning stage onward. Operators invest in layered security architecture that includes perimeter surveillance, biometric access, secure visitor management, and continuous environmental monitoring. Procurement increasingly favors suppliers capable of delivering integrated systems across multiple sites while maintaining standardized security policies, reducing operational complexity, and supporting rapid expansion.

Rising Regulatory and Customer Compliance Requirements

Organizations handling financial records, healthcare information, government data, and critical enterprise workloads face stricter compliance obligations related to physical access management and operational resilience. Auditable access logs, surveillance retention, incident reporting, and secure visitor authentication have become standard procurement requirements. Vendors therefore compete by providing solutions that simplify compliance documentation while reducing administrative overhead for facility operators.

Growth of Edge Computing Facilities

Edge computing deployments introduce a distributed infrastructure model consisting of numerous smaller facilities located closer to end users. Unlike centralized campuses, these locations often operate with limited onsite personnel, increasing demand for remote monitoring, automated access control, intelligent surveillance, and centralized security management. Suppliers offering scalable platforms capable of supporting geographically dispersed facilities benefit from this deployment trend.

Increasing Cost of Service Interruptions

Downtime resulting from unauthorized access, equipment damage, or environmental incidents can generate substantial financial losses for operators and enterprise customers. Consequently, investment decisions increasingly emphasize preventive protection rather than reactive incident response. Buyers prioritize redundant monitoring systems, early-warning environmental detection, and integrated incident management that reduce operational risk while supporting service-level agreements.

Market Restraints and Challenges

High Capital Investment Requirements

Deploying enterprise-grade physical security infrastructure involves significant upfront expenditure on access control equipment, surveillance networks, environmental sensors, secure doors, perimeter protection, and software integration. Smaller enterprises and regional operators may delay modernization projects because of budget limitations. Vendors increasingly address this challenge through managed services, subscription-based software, and phased implementation models.

Integration Complexity Across Legacy Infrastructure

Many enterprise data centers operate legacy access control platforms, analog surveillance systems, and independent environmental monitoring solutions developed over several years. Integrating these technologies into a unified management platform requires specialized engineering expertise, additional software development, and operational testing. Project complexity may increase deployment timelines and implementation costs.

Balancing Security with Operational Efficiency

Data centers require stringent physical controls without restricting maintenance activities or delaying authorized personnel access during operational incidents. Facility operators must balance stringent authentication requirements with efficient workforce mobility, contractor management, and emergency response. Suppliers therefore invest in intelligent identity management, adaptive authentication, and automated workflow capabilities.

Supply Chain and Equipment Availability

Electronic components, imaging devices, networking equipment, and specialized sensors remain exposed to procurement risks arising from component shortages, logistics disruptions, and geopolitical trade restrictions. Extended lead times can delay construction schedules for new facilities while increasing inventory management costs for system integrators and equipment manufacturers.

Major Segment Analysis

Access Control Systems

Access control systems represent one of the most commercially important solution categories because they determine who may enter sensitive operational areas throughout a data center. Modern facilities increasingly deploy multilayer authentication using biometric identification, smart credentials, and digital identity verification to reduce unauthorized access while maintaining comprehensive audit trails.

Demand is particularly strong among hyperscale operators, colocation providers, financial institutions, healthcare organizations, and government agencies where customer trust and regulatory compliance depend upon strict facility security. Buyers increasingly require centralized identity management capable of administering thousands of employees, contractors, and visitors across multiple locations from a unified platform.

Procurement priorities extend beyond hardware performance. Organizations evaluate software interoperability, cybersecurity protections, integration with surveillance systems, scalability, maintenance requirements, and lifecycle operating costs before selecting vendors. Integration with human resource systems and security information management platforms has become an important purchasing consideration for larger enterprises.

Competitive differentiation increasingly depends on combining biometric authentication, mobile credentials, AI-supported anomaly detection, and cloud-based administration while maintaining compatibility with existing building management infrastructure. Suppliers capable of delivering complete implementation, training, maintenance, and compliance support generate recurring revenue beyond the initial equipment sale.

Regional Analysis

North America

North America maintains a substantial share of demand due to extensive cloud infrastructure, mature colocation markets, and continuous investment by hyperscale operators. Government agencies, financial institutions, healthcare providers, and telecommunications companies maintain rigorous security standards that support replacement and modernization projects. Buyers emphasize integrated platforms capable of meeting operational resilience and regulatory requirements while reducing management complexity.

Europe

European demand is influenced by data protection regulations, critical infrastructure security requirements, and increasing investment in sustainable data center development. Operators prioritize secure access management, environmental monitoring, and centralized compliance reporting. Western European markets also exhibit strong demand for modernization of legacy facilities through integrated building management and physical security solutions.

Asia Pacific

Asia Pacific represents an important investment destination due to expanding digital economies, cloud adoption, and government support for domestic data infrastructure. China, India, Japan, South Korea, Taiwan, Indonesia, and Southeast Asian markets continue to attract new hyperscale and colocation developments. Buyers seek scalable security architectures capable of supporting both new construction and expanding regional networks.

Middle East & Africa

Digital transformation initiatives, smart city programs, government cloud strategies, and increasing enterprise digitization contribute to data center investments across the Middle East. Gulf countries continue to attract international cloud providers establishing regional infrastructure. African markets present longer-term opportunities, although investment pace varies according to telecommunications development, energy availability, and capital expenditure.

South America

Brazil remains the principal regional market due to enterprise cloud adoption, expanding telecommunications infrastructure, and growing colocation investment. Other countries continue to develop digital infrastructure, although economic volatility and financing conditions may influence project timing. Buyers generally prioritize reliable, cost-efficient security systems with long operational lifecycles.

Competitive Landscape

Competition within the data center physical security market combines established industrial technology companies, building automation specialists, surveillance providers, networking companies, and integrated security service providers. Suppliers differentiate through system integration capabilities, software functionality, service coverage, lifecycle support, and compatibility with broader facility management platforms.

Competitive positioning increasingly depends on delivering end-to-end solutions encompassing access control, surveillance, environmental monitoring, cybersecurity integration, analytics, remote management, and maintenance services. Strategic partnerships among infrastructure providers, systems integrators, and technology vendors enable comprehensive project execution across multinational deployments.

Companies including ASSA ABLOY Group, Robert Bosch GmbH, Honeywell International Inc., Johnson Controls International plc, Siemens AG, Schneider Electric SE, Hangzhou Hikvision Digital Technology Co., Ltd., Cisco Systems, Inc., Securitas Technology, and Axis Communications AB continue to compete through product innovation, geographic expansion, integrated software capabilities, and long-term customer service agreements.

Recent Developments

May 2026: Alcatraz released major enhancements to its AI-powered Rock™ biometric physical access platform, adding automated firmware management, improved enrollment workflows, flexible consent controls, and enhanced device administration for critical infrastructure, including data center security deployment

March 2026: Genetec introduced new Security Center SaaS access control capabilities, including optional biometric authentication through SAFR SCAN integration, enabling enterprises and data center operators to modernize physical security with stronger identity verification and cloud-based access management.

January 2026: Orion Entrance Control launched Orion DataGuard™, an AI-enabled automated security screening room purpose-built for hyperscale and enterprise data centers, providing automated secure entry, reduced staffing requirements, and enhanced physical protection for critical infrastructure facilities.

January 2026: Fingerprint Cards AB (FPC) announced that its AllKey biometric technology was deployed in ActChip's server rack access control solution for Dynamic-Technologies, introducing biometric authentication at the individual server rack level to strengthen physical security in Indian data centers.

Regulatory and Policy Environment

The market is influenced by regulations governing critical infrastructure protection, occupational safety, cybersecurity, and operational resilience. Data center operators serving regulated industries must implement documented physical access controls, visitor management procedures, surveillance retention policies, and environmental monitoring systems to satisfy compliance obligations.

International standards such as ISO/IEC 27001 emphasize physical security as a fundamental element of information security management. Data centers supporting financial services, healthcare, government operations, and telecommunications frequently incorporate additional sector-specific compliance requirements related to facility protection, auditability, and business continuity.

Building codes, fire protection standards, electrical safety regulations, and environmental monitoring requirements also influence purchasing decisions. Compliance with recognized industry standards encourages investment in integrated monitoring systems capable of generating comprehensive operational records and supporting regulatory inspections.

Outlook and Strategic Implications

Investment over the next five years is expected to concentrate on integrated security ecosystems rather than isolated hardware deployments. Buyers will continue prioritizing centralized management, AI-assisted monitoring, biometric authentication, predictive maintenance, and remote administration as facilities become more distributed through edge computing expansion.

Procurement strategies are expected to favor vendors capable of providing complete project execution, software integration, managed services, cybersecurity compatibility, and long-term maintenance support. Lifecycle cost, interoperability, and scalability will remain decisive purchasing criteria, particularly for multinational operators managing diverse infrastructure portfolios.

Technology development is likely to strengthen convergence between physical security, building automation, operational analytics, and information security. Organizations seeking standardized security governance across global facilities will increasingly prefer unified platforms capable of supporting compliance reporting, operational resilience, and centralized policy management.

Although capital expenditure requirements, supply chain uncertainties, and integration complexity remain commercial risks, continued investment in cloud infrastructure, colocation facilities, and edge computing supports sustained demand for advanced physical security solutions throughout the forecast period. Suppliers with broad implementation expertise, software-centric offerings, and global service capabilities are expected to maintain stronger competitive positions as customer requirements continue to expand.

Data Center Physical Security Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 17.43 billion |

| Total Market Size in 2031 | USD 35.51 billion |

| Forecast Unit | Billion |

| Growth Rate | 15.30% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Components, Solution, Data Center Type, Enterprise Size, End User, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Component

By Solution

By Data Center Type

By Enterprise Size

By End User

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. GLOBAL DATA CENTER PHYSICAL SECURITY MARKET BY COMPONENT

5.1. Introduction

5.2. Hardware

5.3. Software

5.4. Services

6. GLOBAL DATA CENTER PHYSICAL SECURITY MARKET BY SOLUTION

6.1. Introduction

6.2. Access Control Systems

6.2.1. Biometric Authentication

6.2.2. Multi-Factor Authentication

6.3. Environmental Monitoring & Control

6.3.1. Fire Detection & Suppression Systems

6.3.2. Temperature & Humidity Monitoring

6.4. Surveillance & Monitoring Systems

6.5. Others

7. GLOBAL DATA CENTER PHYSICAL SECURITY MARKET BY DATA CENTER TYPE

7.1. Introduction

7.2. Colocation Data Centers

7.3. Hyperscale Data Centers

7.4. Edge Data Centers

7.5. Others

8. GLOBAL DATA CENTER PHYSICAL SECURITY MARKET BY ENTERPRISE SIZE

8.1. Introduction

8.2. Small and Medium Enterprises (SMEs)

8.3. Large Enterprises

9. GLOBAL DATA CENTER PHYSICAL SECURITY MARKET BY END USER

9.1. Introduction

9.2. BFSI

9.3. IT & Telecom

9.4. Government

9.5. Healthcare

9.6. Energy & Utilities

9.7. Others

10. GLOBAL DATA CENTER PHYSICAL SECURITY MARKET BY GEOGRAPHY

10.1. Introduction

10.2. North America

10.2.1. By Component

10.2.2. By Solution

10.2.3. By Data Center Type

10.2.4. By Enterprise Size

10.2.5. By End User

10.2.6. By Country

10.2.6.1. United States

10.2.6.2. Canada

10.2.6.3. Mexico

10.3. South America

10.3.1. By Component

10.3.2. By Solution

10.3.3. By Data Center Type

10.3.4. By Enterprise Size

10.3.5. By End User

10.3.6. By Country

10.3.6.1. Brazil

10.3.6.2. Argentina

10.3.6.3. Others

10.4. Europe

10.4.1. By Component

10.4.2. By Solution

10.4.3. By Data Center Type

10.4.4. By Enterprise Size

10.4.5. By End User

10.4.6. By Country

10.4.6.1. Germany

10.4.6.2. France

10.4.6.3. United Kingdom

10.4.6.4. Spain

10.4.6.5. Others

10.5. Middle East and Africa

10.5.1. By Component

10.5.2. By Solution

10.5.3. By Data Center Type

10.5.4. By Enterprise Size

10.5.5. By End User

10.5.6. By Country

10.5.6.1. Saudi Arabia

10.5.6.2. United Arab Emirates

10.5.6.3. Israel

10.5.6.4. Others

10.6. Asia Pacific

10.6.1. By Component

10.6.2. By Solution

10.6.3. By Data Center Type

10.6.4. By Enterprise Size

10.6.5. By End User

10.6.6. By Country

10.6.6.1. China

10.6.6.2. India

10.6.6.3. Japan

10.6.6.4. South Korea

10.6.6.5. Indonesia

10.6.6.6. Thailand

10.6.6.7. Taiwan

10.6.6.8. Others

11. COMPETITIVE ENVIRONMENT AND ANALYSIS

11.1. Major Players and Strategy Analysis

11.2. Market Share Analysis

11.3. Mergers, Acquisitions, Agreements, and Collaborations

11.4. Competitive Dashboard

12. COMPANY PROFILES

12.1. ASSA ABLOY Group

12.2. Robert Bosch GmbH

12.3. Honeywell International Inc.

12.4. Johnson Controls International plc

12.5. Siemens AG

12.6. Schneider Electric SE

12.7. Hangzhou Hikvision Digital Technology Co., Ltd.

12.8. Cisco Systems, Inc.

12.9. Securitas Technology

12.10. Axis Communications AB

13. APPENDIX

13.1. Currency

13.2. Assumptions

13.3. Base and Forecast Years Timeline

13.4. Key Benefits for Stakeholders

13.5. Research Methodology

13.6. Abbreviations

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations