Report Overview

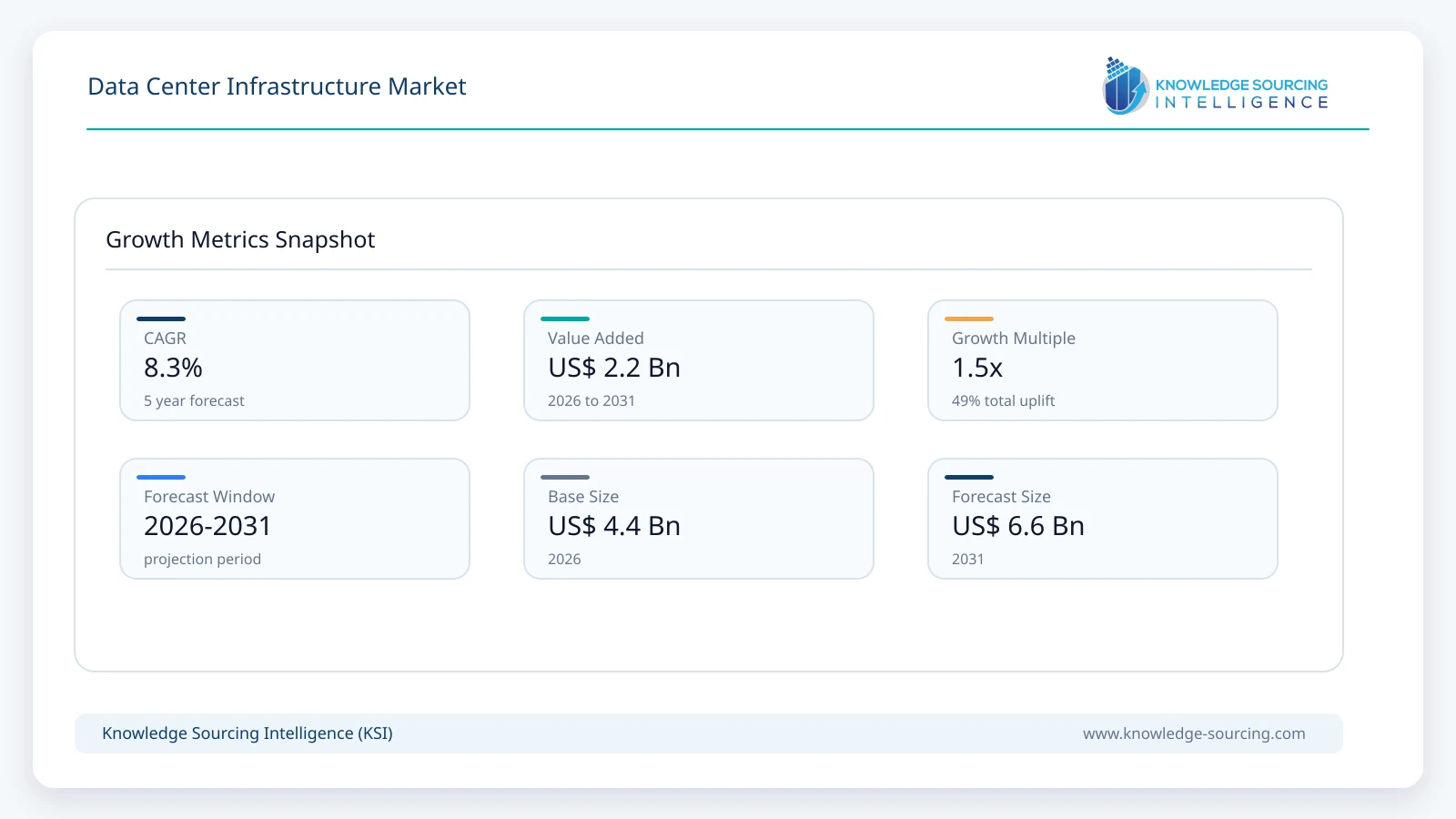

The data centre infrastructure market is forecast to grow at a CAGR of 8.25%, reaching USD 6.60 billion in 2031 from USD 4.44 billion in 2026.

Highlights:

- 1AI infrastructure deployment is increasing demand for high-density power distribution, advanced cooling systems, and intelligent rack infrastructure.

- 2Cloud service providers represent one of the most influential end-user groups due to continuous expansion of hyperscale facilities.

- 3Asia Pacific remains a major investment destination supported by digital economy initiatives and rising cloud adoption.

- 4Liquid cooling, intelligent power management, and DCIM software are becoming standard considerations for new high-density facilities.

- 5Energy efficiency regulations and sustainability reporting requirements are influencing infrastructure procurement decisions.

- 6Competition increasingly centers on integrated infrastructure platforms combining hardware, software, engineering services, and lifecycle support.

The data center infrastructure market comprises the physical and software components required to build, operate, manage, and maintain modern data centers. The market includes power infrastructure, cooling infrastructure, IT infrastructure, network infrastructure, Data Center Infrastructure Management (DCIM) software, and associated services that collectively ensure reliable computing, storage, networking, and facility operations. Demand extends across hyperscale cloud operators, colocation providers, government organizations, financial institutions, telecommunications companies, healthcare organizations, manufacturers, and large enterprises that depend on uninterrupted digital operations.

Enterprise computing requirements have shifted from supporting conventional on-premises workloads to accommodating cloud-native applications, artificial intelligence (AI), high-performance computing (HPC), edge computing, and real-time analytics. These workloads require higher rack densities, improved power efficiency, advanced thermal management, resilient networking architectures, and centralized infrastructure visibility. Buyers increasingly evaluate infrastructure investments based on lifecycle operating costs, scalability, resilience, energy efficiency, cybersecurity readiness, and compatibility with future technology upgrades rather than focusing solely on initial capital expenditure.

Investment activity continues to be supported by expanding cloud capacity, enterprise modernization programs, and government initiatives aimed at strengthening domestic digital infrastructure. The increasing deployment of AI clusters has altered procurement priorities, with operators seeking higher-capacity power distribution systems, liquid cooling technologies, intelligent rack management, and high-bandwidth networking solutions capable of supporting graphics processing units (GPUs) and specialized AI accelerators. Infrastructure vendors are therefore expanding integrated offerings that combine hardware, software, monitoring, and lifecycle services to simplify deployment and improve operational performance.

The procurement environment has also become more strategic. Cloud service providers typically negotiate long-term supply agreements to secure critical electrical equipment and cooling systems, while enterprise customers increasingly prefer modular infrastructure that can be expanded without major facility redesigns. Colocation operators remain focused on delivering flexible capacity for diverse customer workloads while maintaining strict service-level agreements related to uptime and energy efficiency. These varying buyer priorities create opportunities for suppliers capable of delivering customized infrastructure configurations supported by installation, maintenance, and remote monitoring services.

Sustainability considerations have become an important purchasing factor. Rising electricity prices and environmental reporting requirements encourage operators to invest in energy-efficient cooling technologies, intelligent power management systems, renewable energy integration, and software platforms that improve infrastructure utilization. Infrastructure efficiency is now evaluated not only through uptime metrics but also through power usage effectiveness (PUE), water consumption, carbon emissions, and operational automation.

The competitive structure reflects the convergence of electrical engineering, IT hardware, industrial automation, and software capabilities. Infrastructure suppliers compete by offering integrated ecosystems that reduce deployment complexity, shorten installation timelines, improve reliability, and provide predictive maintenance through analytics. Companies with global manufacturing capacity, extensive service networks, and long-standing relationships with hyperscale customers maintain competitive advantages as projects continue to increase in size and technical complexity.

Market Drivers

Expansion of AI and High-Performance Computing Infrastructure

Artificial intelligence training and inference workloads require considerably higher computing density than conventional enterprise applications. GPU-based servers consume substantially greater electrical power and generate higher heat loads, increasing demand for advanced power distribution units, intelligent switchgear, precision cooling, liquid cooling technologies, and high-capacity networking equipment.

Cloud providers, research institutions, and enterprise AI adopters increasingly specify infrastructure designed for future workload expansion rather than current utilization. Infrastructure suppliers respond by developing modular power architectures, liquid cooling systems, and integrated management software capable of supporting continuous performance optimization. This trend increases average infrastructure spending per facility and creates opportunities for premium engineering services.

Growth of Hyperscale and Colocation Data Centers

Organizations continue migrating workloads to public cloud and colocation facilities to improve operational flexibility and reduce internal infrastructure management requirements. Hyperscale operators regularly expand regional capacity to reduce application latency and satisfy regulatory data residency requirements.

These projects involve large procurement volumes for electrical systems, network equipment, cooling technologies, and facility management software. Vendors capable of delivering standardized yet scalable infrastructure solutions benefit from repeat purchasing cycles and long-term service agreements.

Greater Focus on Energy Efficiency

Electricity represents one of the largest operating expenses for data center operators. Rising energy prices encourage investments that reduce cooling requirements, improve electrical efficiency, and optimize equipment utilization.

Operators increasingly evaluate infrastructure based on long-term operational savings rather than equipment acquisition costs alone. Intelligent monitoring platforms, variable-speed cooling technologies, advanced UPS systems, and automated environmental controls contribute to measurable reductions in operating expenditure while supporting sustainability objectives.

Expansion of Edge Computing Infrastructure

Industrial automation, connected vehicles, telecommunications networks, healthcare applications, and smart manufacturing require low-latency computing resources located closer to end users. Edge facilities generally operate within limited physical footprints while maintaining enterprise-grade reliability.

This creates demand for compact, modular infrastructure solutions incorporating integrated power, cooling, networking, physical security, and remote management capabilities. Vendors offering standardized modular designs can accelerate deployment and reduce engineering complexity for distributed infrastructure projects.

Market Restraints and Challenges

Utility Power Availability

In several major metropolitan markets, electrical grid capacity has become a limiting factor for new data center development. Delays in securing utility connections can postpone infrastructure deployment despite strong customer demand.

Developers increasingly coordinate with utility providers during project planning while exploring renewable energy agreements, on-site generation, and battery energy storage systems to reduce dependence on constrained transmission networks.

Supply Chain Complexity for Critical Equipment

Power distribution equipment, transformers, switchgear, generators, and cooling systems often involve extended manufacturing lead times due to specialized components and strong global demand.

These delays affect project scheduling and increase procurement costs for developers. Buyers increasingly diversify supplier relationships and place equipment orders earlier in the construction process to reduce scheduling risks.

Rising Capital Requirements

Modern AI-ready facilities require substantial investments in electrical infrastructure, cooling technologies, networking hardware, and software platforms before commercial operations begin.

Smaller operators may delay expansion because financing costs and uncertain utilization rates increase investment risk. Modular deployment strategies and phased infrastructure implementation help reduce initial capital commitments.

Increasing Technical Complexity

Higher rack densities, liquid cooling integration, software-defined infrastructure, and advanced automation require specialized engineering expertise throughout design, deployment, and operations.

Organizations experiencing workforce shortages often depend on external engineering consultants and managed service providers, increasing project costs while highlighting the importance of vendor support capabilities.

Major Segment Analysis

Power Infrastructure Remains the Commercial Foundation of Data Center Investments

Power infrastructure represents one of the most commercially important solution categories because every expansion project depends on reliable electrical capacity before computing equipment can be deployed. The segment includes uninterruptible power supplies (UPS), power distribution units, switchgear, transformers, backup generators, busways, monitoring systems, and associated electrical infrastructure.

Buyer priorities extend beyond reliability alone. Operators increasingly seek systems that improve electrical efficiency, support predictive maintenance, simplify expansion, and accommodate higher rack power densities associated with AI computing. Procurement decisions frequently emphasize modular scalability, redundancy architecture, lifecycle maintenance costs, and compatibility with renewable energy integration.

Competition centers on engineering capability, installation expertise, service responsiveness, and software integration rather than equipment pricing alone. Suppliers offering intelligent monitoring, predictive diagnostics, and integrated power management platforms strengthen customer retention through long-term service relationships. As computing density continues increasing, spending on electrical infrastructure is expected to remain a substantial component of overall facility investment.

Regional Analysis

North America

North America represents one of the largest infrastructure investment markets due to the concentration of hyperscale cloud providers, enterprise technology companies, financial institutions, and colocation operators. AI infrastructure expansion, renewable energy procurement, and modernization of legacy facilities continue supporting equipment demand. Utility power constraints in selected metropolitan areas remain an important development consideration.

Europe

European demand is influenced by sustainability objectives, energy efficiency standards, and data sovereignty requirements. Investments emphasize efficient cooling technologies, intelligent power management, and environmentally responsible facility design. Enterprises increasingly adopt colocation services to improve operational flexibility while addressing regional compliance obligations.

Asia Pacific

Asia Pacific continues attracting infrastructure investment because of expanding digital economies, increasing cloud adoption, growing enterprise digitization, and government support for domestic data infrastructure. China, India, Japan, South Korea, and Southeast Asian countries continue expanding hyperscale capacity while telecommunications operators invest in edge computing infrastructure. Energy availability and land acquisition remain important planning considerations in selected markets.

Middle East & Africa

Digital government initiatives, cloud adoption, financial sector modernization, and telecommunications expansion contribute to infrastructure demand. Gulf countries continue investing in regional cloud ecosystems supported by national diversification strategies. Infrastructure deployment remains concentrated in major commercial centers with established telecommunications connectivity.

South America

Brazil represents the primary regional market, supported by cloud investment, financial services digitization, and enterprise modernization initiatives. Argentina and other countries continue expanding digital infrastructure despite economic volatility that may influence project financing and procurement timing.

Competitive Landscape

The competitive environment consists of diversified industrial technology companies, enterprise IT vendors, networking specialists, and infrastructure engineering providers. Competition increasingly focuses on delivering integrated infrastructure solutions rather than individual products. Buyers favor suppliers capable of combining electrical systems, cooling technologies, networking equipment, software platforms, engineering services, and lifecycle maintenance under unified project management.

Technology differentiation is achieved through intelligent monitoring, automation capabilities, energy-efficient system designs, modular deployment options, cybersecurity integration, and predictive maintenance functionality. Strategic partnerships with cloud providers, system integrators, construction firms, and semiconductor ecosystem participants strengthen market positioning while expanding geographic reach. Global manufacturing capacity, service availability, supply chain resilience, and technical support remain important competitive differentiators for Hewlett Packard Enterprise Development LP, Cisco Systems, Inc., Schneider Electric SE, Dell Technologies Inc., Vertiv Holdings Co., Eaton Corporation plc, Siemens AG, and Rittal GmbH & Co. KG.

Recent Developments

June 2026: Schneider Electric announced expanded AI-ready data center infrastructure solutions incorporating advanced power distribution and liquid cooling technologies. The development strengthens support for high-density computing deployments.

March 2026: Eaton announced a collaboration with NVIDIA and introduced the Eaton Beam Rubin DSX platform, alongside completing the Boyd Thermal acquisition, strengthening its grid-to-chip power and liquid-cooling infrastructure portfolio for AI data centers.

February 2026: Vertiv introduced its digitally orchestrated Vertiv™ OneCore infrastructure platform and announced collaboration with Hut 8, enabling factory-integrated, Digital Twin-validated power and cooling infrastructure for faster AI data center deployment.

Regulatory and Policy Environment

Government policies increasingly influence infrastructure investment through energy efficiency regulations, environmental reporting requirements, electrical safety standards, cybersecurity frameworks, and national digital infrastructure programs. Operators must comply with electrical installation standards, fire protection requirements, occupational safety regulations, and environmental permitting processes throughout facility development.

Many jurisdictions promote renewable energy adoption and efficient building operation through incentives, emissions reduction programs, and energy performance requirements. Data protection regulations also affect facility location decisions by requiring certain categories of information to remain within national or regional boundaries. Compliance therefore influences both infrastructure design and geographic investment strategies.

Industry standards governing power systems, networking equipment, cooling technologies, and operational resilience continue encouraging adoption of standardized engineering practices. Infrastructure vendors increasingly integrate compliance capabilities into hardware and software offerings to simplify regulatory reporting and operational audits.

Outlook and Strategic Implications

Over the next five years, infrastructure investment is expected to prioritize AI-ready facilities, modular expansion capability, higher electrical capacity, intelligent automation, and improved energy efficiency. Procurement strategies will increasingly emphasize lifecycle value, supply chain reliability, and long-term service partnerships rather than equipment acquisition costs alone.

Infrastructure software will become more closely integrated with electrical, cooling, networking, and facility management systems, enabling predictive maintenance and improved operational visibility. Liquid cooling adoption is expected to accelerate where computing density exceeds the capabilities of conventional air-based systems.

Competition will increasingly favor suppliers capable of delivering complete infrastructure ecosystems supported by engineering expertise, global manufacturing capacity, digital management platforms, and comprehensive service networks. Organizations investing in resilient supply chains, sustainable product development, AI-ready infrastructure, and regional manufacturing capabilities will be better positioned to address evolving customer requirements while managing geopolitical and operational risks.

Data Center Infrastructure Market Scope:

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 4.44 billion |

| Total Market Size in 2031 | USD 6.60 billion |

| Forecast Unit | Billion |

| Growth Rate | 8.25% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Solution, End-User, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Solution

- Power Infrastructure

- Cooling Infrastructure

- IT Infrastructure

- Network Infrastructure

- DCIM Software

- Services

By End User

- Cloud Service Providers

- Colocation Providers

- Enterprises

By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- Germany

- France

- United Kingdom

- Spain

- Others

- Middle East and Africa

- Saudi Arabia

- Israel

- United Arab Emirates

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Taiwan

- Thailand

- Indonesia

- Others

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

1.8. Key Benefits to the Stakeholder

2. RESEARCH METHODOLOGY

2.1. Research Design

2.2. Research Processes

3. EXECUTIVE SUMMARY

3.1. Key Findings

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Porter’s Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of New Entrants

4.3.4. Threat of Substitutes

4.3.5. Competitive Rivalry in the Industry

4.4. Industry Value Chain Analysis

4.5. Analyst View

5. GLOBAL DATA CENTRE INFRASTRUCTURE MARKET BY SOLUTION

5.1. Introduction

5.2. Power Infrastructure

5.3. Cooling Infrastructure

5.4. IT Infrastructure

5.5. Network Infrastructure

5.6. DCIM Software

5.7. Services

6. GLOBAL DATA CENTRE INFRASTRUCTURE MARKET BY END USER

6.1. Introduction

6.2. Cloud Service Providers

6.3. Colocation Providers

6.4. Enterprises

7. GLOBAL DATA CENTRE INFRASTRUCTURE MARKET BY GEOGRAPHY

7.1. Introduction

7.2. North America

7.2.1. By Solution

7.2.2. By End User

7.2.3. By Country

7.2.3.1. United States

7.2.3.2. Canada

7.2.3.3. Mexico

7.3. South America

7.3.1. By Solution

7.3.2. By End User

7.3.3. By Country

7.3.3.1. Brazil

7.3.3.2. Argentina

7.3.3.3. Others

7.4. Europe

7.4.1. By Solution

7.4.2. By End User

7.4.3. By Country

7.4.3.1. Germany

7.4.3.2. France

7.4.3.3. United Kingdom

7.4.3.4. Spain

7.4.3.5. Others

7.5. Middle East and Africa

7.5.1. By Solution

7.5.2. By End User

7.5.3. By Country

7.5.3.1. Saudi Arabia

7.5.3.2. Israel

7.5.3.3. United Arab Emirates

7.5.3.4. Others

7.6. Asia Pacific

7.6.1. By Solution

7.6.2. By End User

7.6.3. By Country

7.6.3.1. China

7.6.3.2. Japan

7.6.3.3. India

7.6.3.4. South Korea

7.6.3.5. Taiwan

7.6.3.6. Thailand

7.6.3.7. Indonesia

7.6.3.8. Others

8. COMPETITIVE ENVIRONMENT AND ANALYSIS

8.1. Major Players and Strategy Analysis

8.2. Market Share Analysis

8.3. Mergers, Acquisitions, Agreements, and Collaborations

8.4. Competitive Dashboard

9. COMPANY PROFILES

9.1. Hewlett Packard Enterprise Development LP

9.2. Cisco Systems, Inc.

9.3. Schneider Electric SE

9.4. Dell Technologies Inc.

9.5. Vertiv Holdings Co.

9.6. Eaton Corporation plc

9.7. Siemens AG

9.8. Rittal GmbH & Co. KG

Navigate

Trusted by the world's leading organizations