Report Overview

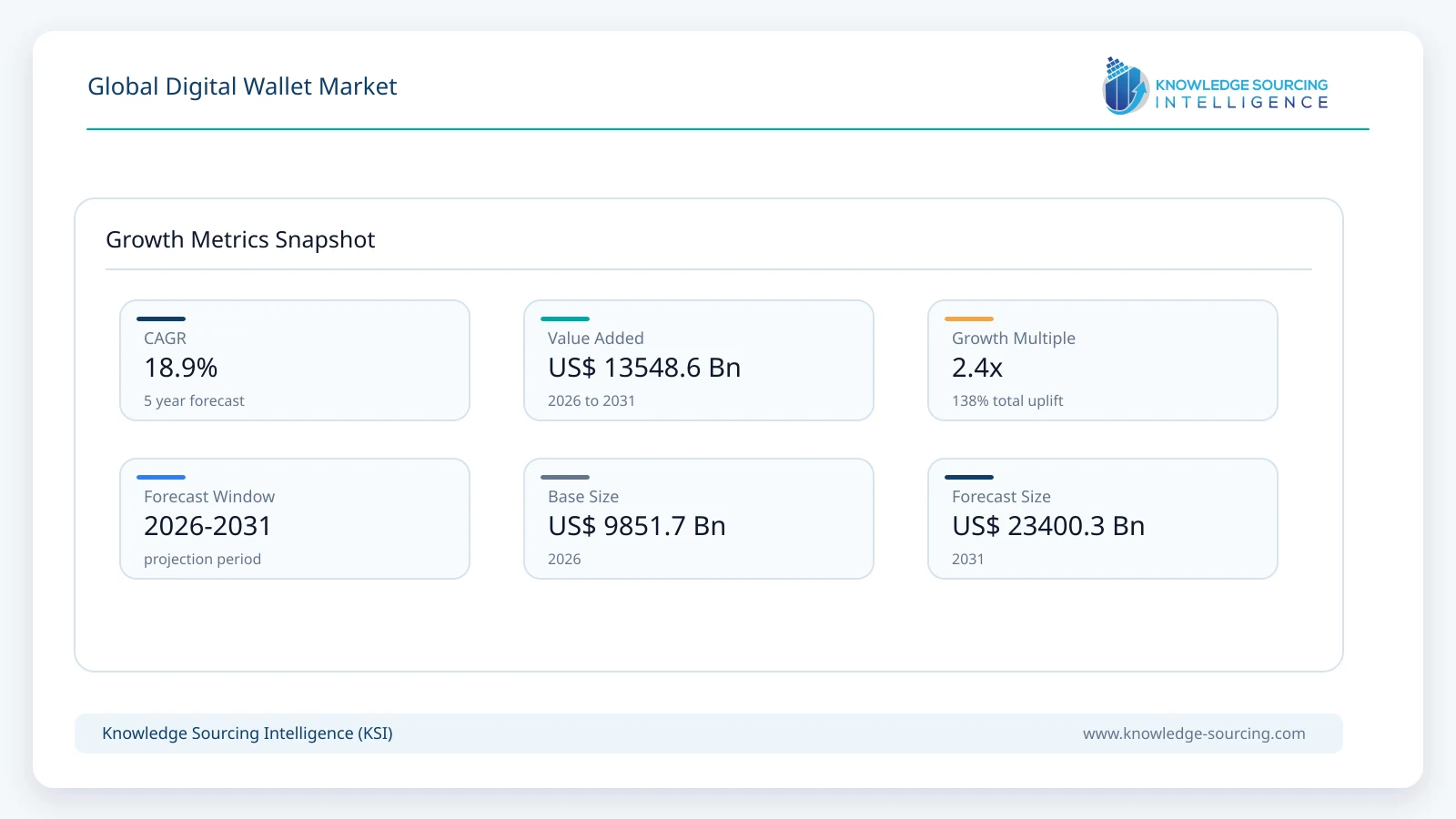

The global digital wallet transaction value is projected to grow at a CAGR of 18.9% over the forecast period, reaching USD 23,400.3 billion by 2031 from an estimated USD 9,851.7 billion in 2026.

Highlights:

- 1Enabling seamless transactionsWallets are simplifying e-commerce checkouts.

- 2Expanding financial inclusionMobile payments are reaching underserved areas.

- 3Boosting contactless adoptionNFC is powering secure touchless payments.

- 4Strengthening biometric securityAuthentication is enhancing user trust.

- 5Driving Asia-Pacific surgeUPI is accelerating wallet usage.

- 6Supporting real-time payments infrastructureSystems are enabling instant transfers.

The digital wallet industry’s expansion is driven by users' increasing interest in using electronic wallets rather than cash, as well as the rising number of merchants/shops that accept digital wallets. Digital wallets store a user's credit card and debit card information digitally and allow the user to make payments on multiple platforms, including in-store and online purchases. In addition, technological advances, such as near field communication (NFC), QR codes (quick response codes), biometric authentication, and tokenization, have improved the security and usability of digital wallets.

Digital Wallet Market Trends:

Digital wallets, storing credit card details and bank account information on mobile devices, offer seamless mobile payments for in-store purchases, bill payments, mobile recharges, movie tickets, and travel reservations. The digital wallet market is surging due to demand for convenient payment systems and technological innovations like virtual currency and contactless payments. In developing countries, mobile payment systems drive a consumer revolution, enhancing financial inclusion.

Real-time customer data analytics boosts digital wallet adoption, enabling retailers to access user information instantly, streamlining transactions, and improving customer experience. This fosters retailer adoption, driving market growth. North America and Europe lead due to advanced fintech infrastructure, while Asia-Pacific, particularly India and China, grows rapidly. Security features like biometric authentication and encryption enhance trust, though cybersecurity risks remain a challenge. Blockchain and AI-driven fraud detection further strengthen secure transactions. The digital wallet market thrives on convenience, innovation, and digital transformation, reshaping global payment ecosystems.

Digital Wallet Market Overview:

The global digital wallet industry has become an integral part of the modern payment system, driven by the rapid transition from cash-based transactions to electronic-based transactions and the government's support of Digital Payment Systems (DPS) worldwide.

Digital wallets allow users to manage their payment methods electronically, carry out payment transactions through retail, person-to-person (P2P), and bill payment methods, by utilising mobile devices or web browsers. Digital wallets are now recognized by governments and central banks as an integral part of the nation's overall financial services infrastructure. As a result, they are subject to regulation aimed at promoting consumer protection, ensuring data security, and establishing oversight of providers' operations.

Various public agencies have reported sustained growth in the number of individuals using digital payment systems in both developed and developing markets. In India, the government has established an infrastructure for digital payments, including the UPI, which enables consumers to make digital payments, thereby reducing cash usage and increasing access to formal financial services. Central bank data confirms that UPI has accounted for a large proportion of the retail digital payment volume, thus exemplifying how public entities encourage the adoption of digital wallets through the acceptance of digital payment systems.

In the U.S. and EU, regulators are expanding their supervisory reach to cover many of the larger, non-bank providers of payment services and digital wallets. These providers will now be held to the same compliance standards as traditional financial institutions for consumer data protection and fraud prevention. With these recent developments, governments are creating regulations for these services and considering digital wallets to be regulated financial products, rather than optional forms of payment. The government is also creating a framework for digital wallets to integrate into the nation's broader payment ecosystem and facilitate cross-border payments globally.

The sharp rise in UPI transaction volumes reflects how public digital payment infrastructure can scale rapidly when supported by government policy, regulatory clarity, and interoperability standards. The expansion from 92 crore transactions in FY 2017–18 to over 13,000 crore by FY 2023–24 demonstrates widespread adoption of wallet-based and account-to-account digital payments. This growth strengthens the global digital wallet market by setting a replicable model for real-time payments, cross-platform compatibility, and low-cost transactions. As UPI expands internationally through bilateral linkages, it supports global digital payment integration, accelerates cashless adoption, and influences how other countries design and regulate their own digital wallet ecosystems.

Consequently, customers are increasingly demanding the best from both worlds, and internet shopping is merging into conventional store-based business. More individuals are embracing digital wallets to complete purchases owing to rising internet penetration and expanding smartphone usage. Presently, there is a wide range of e-wallet services, including GPay, PayPal, and Apple Pay, among several others. The e-wallet payment system has been modified to make transactions more convenient for consumers. An e-wallet payment system offers other services outside of processing payments to businesses, like integrating loyalty cards and serving marketing functions.

Speed - As per PayPal, cart abandonment is a major problem for retailers. 69.8% of carts are left before the checkout process is complete. This is generally when customers become irritated because there are many details to fill out.

Security - Digital wallets, according to the Identity Theft Resource Center, rely on time-tested security methods like two-factor verification and PINs that are limited to being utilized once. As a result, it is more challenging for cybercriminals to obtain this information when consumers utilize their digital wallets to purchase goods.

Convenience - According to Marqeta, 60% of consumers indicated that they will feel at ease going out with just their smartphone and not their wallet because of the high level of consumer trust in contactless banking and digital wallets. Furthermore, more than half (56%) of the consumers claimed to have become accustomed to contactless payments and find it inconvenient to enter a PIN.

Digital Wallet Market Growth Drivers:

Smartphone and internet penetration

Smartphones and internet access indicate the proportion of people who have access to a mobile device that can connect to the internet and the necessary underlying network for reliable connections. Governments and global organisations view this as one of the pillars of a modern digital infrastructure. As people gain more access to these devices, they will be able to use digital services for education, healthcare, government, and commerce. The number of people connected to the internet continues to increase.

Policies are now being implemented to create provisions for expanding mobile broadband networks, and making broadband data affordable will be an important part of achieving digital inclusion. As one solution, the Government of India has initiated the BharatNet program, which has built extensive networks of optical fibre in rural areas, helping to bridge the digital divide between urban and rural regions.

Two additional areas of focus within these initiatives are digital literacy and the availability of devices. Regulatory agencies have determined that merely providing access to a connection is inadequate for people to enjoy the benefits of using a digital device; individuals must also be capable of using a digital device safely and effectively. Digital affordability, digital infrastructure, and digital literacy are the three core areas of focus, and together these three areas will help to expand access to the digital economy for many people.

Increased smartphone and internet penetration will help bring greater economic inclusion and participation of a larger number of people into digital services and digital markets. The economic foundation that increased smartphone and internet penetration provides will assist all industries to innovate and adopt new technologies, ultimately becoming stronger and more accessible within the global economy.

High smartphone ownership among young adults, with 95.5% in rural areas and 97.6% in urban areas, is a strong indicator of digital readiness. Widespread access to smartphones expands the potential user base for digital services, enabling faster adoption of mobile-based solutions across sectors. This accessibility supports continuous connectivity, allowing individuals to engage with online platforms, apps, and services efficiently. For the digital wallet market, such penetration lays the foundation for increased transactions, seamless money transfers, and broader financial inclusion. It also encourages innovation in app features and payment infrastructure to cater to a digitally connected population.

Increasing focus on contactless payment

The higher emphasis on using digital wallets has resulted in increased demand, implying that the market will be favorable henceforth. There also continues to be a growth in the popularity of touchless payment systems because individuals need a safer mode since they deviate from the use of paper money or cards. Moreover, digital wallets are provided with almost proximity interaction (NFC) technology, enabling quick and secure contactless transactions by customers using their smartphones on POS machines. It means that prompt payment is more convenient for those who are busy. Paying for goods or services using contactless cards has seen an increased use among people in a bid to maintain cleanliness against spreading diseases like coronavirus. Businesses are spending money on NFC-capable terminals in an attempt to meet customer preferences, which has resulted in the expansion of the market.

Rising security concerns

Digital wallet providers understand that their products need to be more secure than before. Hence, they are rolling out advanced security features such as biometric authentication and tokenization to boost public trust. Moreover, authentication techniques based on biometrics create a very secure layer, thereby ensuring that only legitimate users can access or use the phone wallets that they have created. Additionally, tokenization reduces the likelihood of a data breach by making it deeper.

Some of the best-known companies worldwide have set up cutting-edge security systems to increase their customers' confidence while making various types of payments. Companies like Google or Amazon could use cutting-edge security systems to enhance consumer confidence while making online payments.

Easy checkout process

Digital wallet apps make it possible for users to store different payment methods, like debit cards and credit cards, among other cards, in one place. Because of this, there is no need to carry plastic cards around anymore, because any transaction can be quickly made. Furthermore, digital wallets simplify both online and offline payments, thus easing checkouts. Digital wallets also make it easier to check out for both in-person and online purchases. In keeping with this, consumers can finish transactions on their smartphones with a few taps, reducing time spent in line or entering payment information. Additionally, digital wallets provide tools for budgeting and tracking transaction histories. The market is growing because consumers can easily observe their spending and get insightful information about their financial habits.

Favourable government initiatives and investments

The enhancement of internet infrastructure and technological upgradation, coupled with developments in digital payment platforms, has propelled the demand for digital wallets globally. Also, favourable government initiatives to bolster digitization are further expected to accelerate the digital wallet industry's growth. For instance, the “Digital India” initiative aims to make government services more accessible to all citizens of the nation electronically. Moreover, efforts to promote digital payment platforms in several Middle Eastern countries are also being witnessed.

Digital Wallet Market Restraint:

Increasing cases of cyber crimes

Digital wallets and mobile payment applications have become more popular, which is why they have attracted the attention of cyber-criminals. Due to mobile wallet attacks, many people have lost their sensitive information, and hundreds of millions of dollars have been lost in the process. NITI Aayog data shows that such attacks have affected more than half of the Indian enterprises; a few examples are ransomware, phishing scams, Trojans, and denial-of-service attacks; all these are cyber threats that could disrupt the steady growth of the company’s business. Providers of financial technology services are more susceptible to various types of cyberattacks owing to the constant addition of new features and technologies aimed at satisfying customer demands, which could, in turn, inhibit market development.

Digital Wallet Market Segment Analysis:

The PC/Laptops segment is anticipated to grow substantially

The global digital wallet industry for devices is bifurcated into PCs/laptops and smartphones. Contrary to mobile phones, PC/laptops are considered a safer option for transferring money as these are less susceptible to certain types of malware and phishing attacks, which can help your digital wallet and financial information. Additionally, a PC/laptop can provide a larger screen and better user interface for checking and confirming transaction information, enhancing accuracy and security while completing transactions using digital wallets, especially for larger sums or more complex transactions. Moreover, for people who cannot keep their financial transactions properly, they can easily transfer their record data into a file for keeping track or for financial analysis.

Additionally, PCs give an easy way to access and manage digital wallet services. Through the web-based interfaces or dedicated desktop apps supplied by wallet service providers, users can log in to their digital wallet accounts, check balances, review transaction history, and undertake other financial operations. Secure operating systems and huge visibility, as compared to mobile, help pay larger amounts with more confidence. Hence, the use of non-cash transactions is increasing in the US, along with various other countries, which is providing an edge for industry growth as the use of PCs or laptops is anticipated to increase for larger amounts, providing an edge for industry growth in the coming years.

By Device: Smartphones

Smartphones offer an easy way to access and manage digital wallet services through the web-based interfaces or dedicated mobile apps supplied by wallet service providers. This functionality allows users to log in to their digital wallet accounts, check balances, review transaction history, and undertake other financial operations. It offers secure operating systems and greater visibility compared to mobile, allowing users to make larger payments with more confidence.

Rapid urbanization and improvement in living standards have provided a major boost to digitization, with consumers preferring digital platforms to process their transactions, thereby eliminating the need to carry physical cards or cash. Likewise, the high convenience offered by digital wallets is driving the habitual usage, with consumers receiving weekly account notifications and security alerts. Hence, smartphones align with the given usage criteria for digital wallets, with consumers conducting transactions anywhere.

With constant economic growth and an improved frequency of smartphone users, the prevalence of usage of digital wallets is projected to show considerable growth. According to Zimperium’s “Global Mobile Threat Report”, by the end of 2024, the global number of smartphone users reached 7.2 billion. Hence, major regional economies, namely the United States, China, India, and the European Union, are witnessing considerable growth in the digital economy signifies a constant increase in smartphone adoption in such nations.

According to the July 2025 PIB (Press Information Bureau) release, the total number of Digilocker users as of June 2025 reached 53.93 crores. Additionally, according to the National eGovernance Division, as of 23rd December 2025, the number of mobile verified sign-ups in Digilocker stood at 168.64 lakhs, representing a considerable growth of 20.59% over the total number of mobile verified sign-ups recorded in the preceding year. Booming digital economic growth has further propelled the use of mobiles & smartphones for conducting transactions and accessing essential documents via digital document wallets.

Furthermore, the e-commerce sector has taken a massive leap over the years, fuelled by the growing internet penetration, especially among the younger generation and millennials who prefer online shopping through smartphones. According to the “E-Commerce Trend Report 2025” issued by DHL, it was stated that nearly 83% of millennials prefer to shop through mobile apps.

Digital Wallet Market Geographical Outlook:

Asia Pacific is projected to grow at a high rate during the forecast period

Southeast Asia is rapidly emerging as a key player in the global digital wallet market, driven by robust economic growth and a sharp rise in smartphone penetration. Historically reliant on cash-based transactions, the region is now witnessing a significant shift toward cashless payments. This transformation is being powered by a diverse ecosystem of stakeholders, including banks, ride-hailing platforms, remittance services, and fintech startups, who are expanding access to digital financial tools. While China previously led the mobile payment revolution through its advanced fintech infrastructure, Southeast Asia is quickly closing the gap by embracing digital wallets at scale.

North America: the US

The booming technological innovations have transformed the digital landscape in the United States, thereby providing new growth prospects for digital wallets, which are becoming an effective alternative for making payments and storing necessary financial information. The new approach aligns with the national objective of promoting contactless payment options among users, offering them higher convenience. Furthermore, the improved internet penetration has also played a major role in driving the adoption trend.

Similarly, the booming e-commerce activities fuelled by the improvement in urban population, youth and millennials’ strength have further escalated the prevalence of digital platforms usage for making transactions. According to data revealed by the Census Bureau of the Department of Commerce, in Q3 2025, the total US retail e-commerce sales seasonally adjusted reached USD 310.27 billion, marking a considerable growth of 5.1% over Q3 2024. The same source also specified that e-commerce sales accounted for 16.4% of total retail sales.

Additionally, the financial institutions, realizing the growing importance of digital wallets, are investing in strategic collaborations with market players. For instance, in November 2025, Citibank announced its collaboration with Coinbase to bolster its digital asset payment, thereby enabling it to build digital infrastructure that will offer next-generation financial services for its global network of clients.

Furthermore, digital wallets are rapidly expanding their reach into various applications beyond traditional payment scenarios. For U.S. internet gaming companies, payments are a key driver of client retention. Digital wallets attempt to give operators a competitive advantage in terms of client acquisition and retention by offering an unmatched payment experience.

The huge customer base and high transactional volume, coupled with the implementation of incentives and programs to bolster the digital economy, haves made the United States a major market for online financial services. Hence, various market players, namely PayPal, Google LLC, Apple Inc., and Mastercard, among others, have a well-established presence in the US. According to the quarterly report from PayPal, in Q3 2025, the company’s total payment volume (TPV) reached USD 458,088 million, of which the United States alone accounted for USD 285,966, representing a 7.6% year-on-year growth. Such improved revenue growth showcases the growing market potential for digital wallets in the United States.

Digital Wallet Market Key Developments:

April 2026: AstreaX launched AX Wallet, a secure digital identity wallet enabling citizens to store government-issued credentials, access public services, and manage digital identification through a mobile platform.

April 2026: Tether launched tether.wallet, a self-custodial digital wallet designed to provide global users with direct access to payments, transfers, and digital financial services through Tether’s infrastructure.

April 2026: Exodus Movement launched Exodus Pay, a digital wallet solution allowing users to spend, send, and manage digital assets from a single application while retaining full self-custody and control.

February 2026: Ericsson and Mastercard announced a strategic collaboration integrating the Ericsson Fintech Platform with Mastercard Move, enabling telecom operators, banks, and fintechs to expand digital wallet services and money movement capabilities.

January 2026: Ingenico launched its Digital Currency Solution in partnership with WalletConnect Pay, enabling consumers to use more than 700 digital wallets for stablecoin payments at physical merchant checkouts worldwide.

January 2026: Rumble and Tether launched Rumble Wallet, a non-custodial digital wallet integrated directly into the Rumble platform, enabling creator tipping and peer-to-peer payments using Bitcoin, USDT, and Tether Gold.

Digital Wallet Market Scope:

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 9,851.7 billion |

| Total Market Size in 2031 | USD 23,400.3 billion |

| Forecast Unit | Billion |

| Growth Rate | 18.9% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Type, Technology, Device, Application, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Type

By Technology

By Device

By Application

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. GLOBAL DIGITAL WALLET INDUSTRY BY TYPE

5.1. Introduction

5.2. Open Wallet

5.3. Closed Wallet

5.4. Semi-Closed Wallet

5.5. Others

6. GLOBAL DIGITAL WALLET INDUSTRY BY TECHNOLOGY

6.1. Introduction

6.2. Near-Field Communication (NFC)

6.3. Biometric Authentication

6.4. QR Codes

6.5. Tokenization

6.6. Others

7. GLOBAL DIGITAL WALLET INDUSTRY BY DEVICE

7.1. Introduction

7.2. PC/Laptops

7.3. Smartphones

8. GLOBAL DIGITAL WALLET INDUSTRY BY APPLICATION

8.1. Introduction

8.2. Money Transfer

8.3. Recharge

8.4. Movie Booking

8.5. Food Ordering

8.6. Others

9. GLOBAL DIGITAL WALLET INDUSTRY BY GEOGRAPHY

9.1. Introduction

9.2. North America

9.2.1. By Type

9.2.2. By Technology

9.2.3. By Device

9.2.4. By Application

9.2.5. By Country

9.2.5.1. United States

9.2.5.1.1. By Type

9.2.5.1.2. By Technology

9.2.5.1.3. By Device

9.2.5.1.4. By Application

9.2.5.2. Canada

9.2.5.2.1. By Type

9.2.5.2.2. By Technology

9.2.5.2.3. By Device

9.2.5.2.4. By Application

9.2.5.3. Mexico

9.2.5.3.1. By Type

9.2.5.3.2. By Technology

9.2.5.3.3. By Device

9.2.5.3.4. By Application

9.3. South America

9.3.1. By Type

9.3.2. By Technology

9.3.3. By Device

9.3.4. By Application

9.3.5. By Country

9.3.5.1. Brazil

9.3.5.1.1. By Type

9.3.5.1.2. By Technology

9.3.5.1.3. By Device

9.3.5.1.4. By Application

9.3.5.2. Argentina

9.3.5.2.1. By Type

9.3.5.2.2. By Technology

9.3.5.2.3. By Device

9.3.5.2.4. By Application

9.3.5.3. Others

9.3.5.3.1. By Type

9.3.5.3.2. By Technology

9.3.5.3.3. By Device

9.3.5.3.4. By Application

9.4. Europe

9.4.1. By Type

9.4.2. By Technology

9.4.3. By Device

9.4.4. By Application

9.4.5. By Country

9.4.5.1. United Kingdom

9.4.5.1.1. By Type

9.4.5.1.2. By Technology

9.4.5.1.3. By Device

9.4.5.1.4. By Application

9.4.5.2. Germany

9.4.5.2.1. By Type

9.4.5.2.2. By Technology

9.4.5.2.3. By Device

9.4.5.2.4. By Application

9.4.5.3. France

9.4.5.3.1. By Type

9.4.5.3.2. By Technology

9.4.5.3.3. By Device

9.4.5.3.4. By Application

9.4.5.4. Spain

9.4.5.4.1. By Type

9.4.5.4.2. By Technology

9.4.5.4.3. By Device

9.4.5.4.4. By Application

9.4.5.5. Others

9.4.5.5.1. By Type

9.4.5.5.2. By Technology

9.4.5.5.3. By Device

9.4.5.5.4. By Application

9.5. Middle East and Africa

9.5.1. By Type

9.5.2. By Technology

9.5.3. By Device

9.5.4. By Application

9.5.5. By Country

9.5.5.1. Saudi Arabia

9.5.5.1.1. By Type

9.5.5.1.2. By Technology

9.5.5.1.3. By Device

9.5.5.1.4. By Application

9.5.5.2. UAE

9.5.5.2.1. By Type

9.5.5.2.2. By Technology

9.5.5.2.3. By Device

9.5.5.2.4. By Application

9.5.5.3. Others

9.5.5.3.1. By Type

9.5.5.3.2. By Technology

9.5.5.3.3. By Device

9.5.5.3.4. By Application

9.6. Asia Pacific

9.6.1. By Type

9.6.2. By Technology

9.6.3. By Device

9.6.4. By Application

9.6.5. By Country

9.6.5.1. Japan

9.6.5.1.1. By Type

9.6.5.1.2. By Technology

9.6.5.1.3. By Device

9.6.5.1.4. By Application

9.6.5.2. China

9.6.5.2.1. By Type

9.6.5.2.2. By Technology

9.6.5.2.3. By Device

9.6.5.2.4. By Application

9.6.5.3. India

9.6.5.3.1. By Type

9.6.5.3.2. By Technology

9.6.5.3.3. By Device

9.6.5.3.4. By Application

9.6.5.4. South Korea

9.6.5.4.1. By Type

9.6.5.4.2. By Technology

9.6.5.4.3. By Device

9.6.5.4.4. By Application

9.6.5.5. Taiwan

9.6.5.5.1. By Type

9.6.5.5.2. By Technology

9.6.5.5.3. By Device

9.6.5.5.4. By Application

9.6.5.6. Thailand

9.6.5.6.1. By Type

9.6.5.6.2. By Technology

9.6.5.6.3. By Device

9.6.5.6.4. By Application

9.6.5.7. Indonesia

9.6.5.7.1. By Type

9.6.5.7.2. By Technology

9.6.5.7.3. By Device

9.6.5.7.4. By Application

9.6.5.8. Others

9.6.5.8.1. By Type

9.6.5.8.2. By Technology

9.6.5.8.3. By Device

9.6.5.8.4. By Application

10. COMPETITIVE ENVIRONMENT AND ANALYSIS

10.1. Major Players and Strategy Analysis

10.2. Market Share Analysis

10.3. Vendor Matrix

10.4. Mergers, Acquisitions, Agreements, and Collaborations

10.5. Competitive Dashboard

11. COMPANY PROFILES

11.1. Payment

11.1.1. Samsung

11.1.1.1. Overview

11.1.1.2. Product and Service

11.1.1.3. Financials

11.1.1.4. Key Developments

11.1.2. Apple Inc.

11.1.2.1. Overview

11.1.2.2. Product and Service

11.1.2.3. Financials

11.1.2.4. Key Developments

11.1.3. Google LLC

11.1.3.1. Overview

11.1.3.2. Product and Service

11.1.3.3. Financials

11.1.3.4. Key Developments

11.1.4. PayPal Holdings, Inc.

11.1.4.1. Overview

11.1.4.2. Product and Service

11.1.4.3. Financials

11.1.4.4. Key Developments

11.1.5. LINE Pay Corporation

11.1.5.1. Overview

11.1.5.2. Product and Service

11.1.5.3. Key Developments

11.1.6. Paytm Payment Bank Limited

11.1.6.1. Overview

11.1.6.2. Product and Service

11.1.6.3. Financials

11.1.7. Zelle

11.1.7.1. Overview

11.1.7.2. Product and Service

11.1.7.3. Key Developments

11.1.8. Walmart

11.1.8.1. Overview

11.1.8.2. Product and Service

11.1.8.3. Financials

11.1.8.4. Key Developments

11.1.9. Mastercard

11.1.9.1. Overview

11.1.9.2. Product and Service

11.1.9.3. Financials

11.1.9.4. Key Developments

11.1.10. WeChat (Tencent Holdings Limited)

11.1.10.1. Overview

11.1.10.2. Product and Service

11.1.10.3. Financials

11.1.10.4. Key Developments

11.1.11. Alipay (Alibaba Group)

11.1.11.1. Overview

11.1.11.2. Product and Service

11.1.11.3. Financials

11.1.11.4. Key Developments

11.1.12. MercadoLibre Inc.

11.1.12.1. Overview

11.1.12.2. Product and Service

11.1.12.3. Financials

11.1.12.4. Key Developments

11.1.13. Venmo

11.1.13.1. Overview

11.1.13.2. Product and Service

11.1.13.3. Key Developments

11.1.14. Cash App

11.1.14.1. Overview

11.1.14.2. Product and Service

11.1.14.3. Key Developments

11.1.15. GoPay

11.1.15.1. Overview

11.1.15.2. Product and Service

11.1.16. PhonePe

11.1.16.1. Overview

11.1.16.2. Product and Service

11.1.16.3. Key Developments

11.1.17. RapiPay Fintech Private Ltd

11.1.17.1. Overview

11.1.17.2. Product and Service

11.1.17.3. Financials

11.1.18. DANA – PT

11.1.18.1. Overview

11.1.18.2. Product and Service

11.1.18.3. Key Developments

11.1.19. Huawei Pay (Huawei Technologies Co. Ltd)

11.1.19.1. Overview

11.1.19.2. Product and Service

11.1.19.3. Financials

11.1.19.4. Key Developments

11.1.20. Kakao Corporation

11.1.20.1. Overview

11.1.20.2. Product and Service

11.1.20.3. Financials

11.1.20.4. Key Developments

11.1.21. Freecharge Payment Technologies Pvt. Ltd. (Axis Bank)

11.1.21.1. Overview

11.1.21.2. Product and Service

11.1.21.3. Financials

11.1.22. PicPay

11.1.22.1. Overview

11.1.22.2. Product and Service

11.1.22.3. Financials

11.1.22.4. Key Developments

11.1.23. Grab Holdings Inc.

11.1.23.1. Overview

11.1.23.2. Product and Service

11.1.23.3. Financials

11.1.23.4. Key Developments

11.1.24. ConsenSys (MetaMask)

11.1.24.1. Overview

11.1.24.2. Product and Service

11.1.24.3. Key Developments

11.1.25. imToken Pte. Ltd.

11.1.25.1. Overview

11.1.25.2. Product and Service

11.1.25.3. Key Developments

11.1.26. Ledger

11.1.26.1. Overview

11.1.26.2. Product and Service

11.1.26.3. Key Developments

11.1.27. HyperPay

11.1.27.1. Overview

11.1.27.2. Product and Service

11.1.27.3. Key Developments

11.1.28. Coinbase

11.1.28.1. Overview

11.1.28.2. Product and Service

11.1.28.3. Financials

11.1.28.4. Key Developments

11.1.29. SafePal Wallet

11.1.29.1. Overview

11.1.29.2. Product and Service

11.1.29.3. Key Developments

11.1.30. Coin98 Labs

11.1.30.1. Overview

11.1.30.2. Product and Service

11.1.30.3. Key Developments

11.1.31. MathWallet

11.1.31.1. Overview

11.1.31.2. Product and Service

11.1.31.3. Key Developments

11.1.32. Atomic Wallet

11.1.32.1. Overview

11.1.32.2. Product and Service

11.1.33. Phantom

11.1.33.1. Overview

11.1.33.2. Product and Service

11.1.33.3. Financials

11.1.33.4. Key Developments

11.1.34. AlphaWallet

11.1.34.1. Overview

11.1.34.2. Product and Service

11.1.35. Trust Wallet

11.1.35.1. Overview

11.1.35.2. Product and Service

11.2. Identity

11.2.1. Thales

11.2.1.1. Overview

11.2.1.2. Product and Service

11.2.1.3. Financials

11.2.1.4. Key Developments

11.2.2. Identyum

11.2.2.1. Overview

11.2.2.2. Product and Service

11.2.3. ID.me, Inc.

11.2.3.1. Overview

11.2.3.2. Product and Service

11.2.3.3. Key Developments

11.2.4. Scytales AB

11.2.4.1. Overview

11.2.4.2. Product and Service

11.2.4.3. Key Developments

11.2.5. EUDI Wallet

11.2.5.1. Overview

11.2.5.2. Product and Service

11.2.5.3. Key Developments

11.2.6. Google LLC

11.2.6.1. Overview

11.2.6.2. Product and Service

11.2.6.3. Financials

11.2.6.4. Key Developments

11.2.7. Apple Inc.

11.2.7.1. Overview

11.2.7.2. Product and Service

11.2.7.3. Financials

11.2.7.4. Key Developments

11.2.8. Samsung

11.2.8.1. Overview

11.2.8.2. Product and Service

11.2.8.3. Financials

11.2.8.4. Key Developments

11.2.9. Trinsic Technologies Inc.

11.2.9.1. Overview

11.2.9.2. Product and Service

11.2.9.3. Key Developments

11.2.10. LA Wallet

11.2.10.1. Overview

11.2.10.2. Product and Service

11.2.10.3. Key Developments

11.2.11. DigiLocker

11.2.11.1. Overview

11.2.11.2. Product and Service

11.2.11.3. Key Developments

11.3. Access

11.3.1. Apple Inc.

11.3.1.1. Overview

11.3.1.2. Product and Service

11.3.1.3. Financials

11.3.1.4. Key Developments

11.3.2. Google LLC

11.3.2.1. Overview

11.3.2.2. Product and Service

11.3.2.3. Financials

11.3.2.4. Key Developments

11.3.3. Samsung

11.3.3.1. Overview

11.3.3.2. Product and Service

11.3.3.3. Financials

11.3.3.4. Key Developments

11.3.4. LastPass

11.3.4.1. Overview

11.3.4.2. Product and Service

11.3.4.3. Key Developments

11.3.5. Selznick Scientific Software

11.3.5.1. Overview

11.3.5.2. Product and Service

11.3.5.3. Key Developments

11.3.6. The Cleveland Orchestra and Musical Arts Association

11.3.6.1. Overview

11.3.6.2. Product and Service

11.3.6.3. Financials

11.3.6.4. Key Developments

11.3.7. True Tickets

11.3.7.1. Overview

11.3.7.2. Product and Service

11.3.7.3. Key Developments

11.3.8. Wallet Passes

11.3.8.1. Overview

11.3.8.2. Product and Service

11.3.9. PayPal

11.3.9.1. Overview

11.3.9.2. Product and Service

11.3.9.3. Financials

11.3.9.4. Key Developments

11.4. White Label Platform

11.4.1. Cellum

11.4.1.1. Overview

11.4.1.2. Product and Service

11.4.1.3. Key Developments

11.4.2. Mastercard

11.4.2.1. Overview

11.4.2.2. Product and Service

11.4.2.3. Financials

11.4.2.4. Key Developments

11.4.3. Amdocs

11.4.3.1. Overview

11.4.3.2. Product and Service

11.4.3.3. Financials

11.4.3.4. Key Developments

11.4.4. Velmie

11.4.4.1. Overview

11.4.4.2. Product and Service

11.4.4.3. Key Developments

11.4.5. Mistral Mobile

11.4.5.1. Overview

11.4.5.2. Product and Service

11.4.6. Panamax Inc. (Bankai Group Inc.)

11.4.6.1. Overview

11.4.6.2. Product and Service

11.4.7. PureSoftware

11.4.7.1. Overview

11.4.7.2. Product and Service

11.4.7.3. Key Developments

11.4.8. Telefonaktiebolaget LM Ericsson

11.4.8.1. Overview

11.4.8.2. Product and Service

11.4.8.3. Financials

11.4.8.4. Key Developments

11.4.9. Youtap Limited

11.4.9.1. Overview

11.4.9.2. Product and Service

11.4.9.3. Key Developments

11.4.10. Hi Sun FinTech Global Limited

11.4.10.1. Overview

11.4.10.2. Product and Service

11.4.10.3. Financials

11.4.10.4. Key Developments

11.4.11. Comviva Technologies Limited (Tech Mahindra Company)

11.4.11.1. Overview

11.4.11.2. Product and Service

11.4.11.3. Financials

11.4.11.4. Key Developments

12. RESEARCH METHODOLOGY

List of Figures

List of Tables

Research Methodology

This report has been prepared using Knowledge Sourcing Intelligence's (KSI's) market research framework, which combines secondary research, company-level analysis, market triangulation, and analyst review. The research process defines the market boundary, identifies demand and supply indicators, maps key participants, and evaluates market trends over the study period.

For the Global Digital Wallet Market, the research process considered smartphone and internet penetration, digital payment adoption, e-commerce activity, contactless payment volume, financial inclusion initiatives in major countries like India, real-time payment infrastructure investments, and consumer and merchant preference for cashless transactions. The analysis also considers product innovation across open, semi-closed, and closed digital wallets, along with changes in QR code payments, near-field communication, tokenization, biometric authentication, and cross-border payment capabilities driving digital wallet adoption across geographies.

Supply-side assessment considers digital wallet platforms, payment processing networks, merchant payment infrastructure, mobile application ecosystems, and the availability of cloud infrastructure, payment gateways, identity verification services, fraud prevention solutions, and application programming interfaces among others. The competitive strategies of banks, fintech companies, payment network providers, technology companies, telecommunications operators, e-commerce platforms, and digital wallet providers were also reviewed.

The segmentation in this study include type, technology, device, application, and geography. Regional and country-level analysis was developed using digital payment transaction data, smartphone and internet penetration indicators, bank account statistics, and e-commerce acitivity, financial inclusion indicators, government and regulatory publications, investor presentations, and other credible secondary sources. KSI also undertakes primary inputs and expert discussions to map them to internal estimation models.

Public source categories reviewed for this study include digital payment industry publications, financial inclusion statistics, mobile connectivity indicators, payment transaction data, cybersecurity and payment security regulations, regulatory filings, and industry association data. Examples of broader sources considered include the Bank for International Settlements, World Bank, GSMA, EMVCo, PCI Security Standards Council, NFC Forum, central banks, national financial regulators, payment industry associations, national statistics agencies, investor presentations, and press releases, among others.

Market estimates were reviewed through bottom-up and top-down modelling. Bottom-up validation considered company participation, digital wallet user bases, transaction volumes, payment values, merchant networks, platform partnerships, pricing and fee structures, regional operations, and wallet adoption indicators. Top-down validation considers smartphone and internet usage, bank account penetration, digital payment activity, e-commerce growth, financial inclusion, merchant digitization, payment infrastructure development, and other relevant macroeconomic parameters.

Final outputs were reviewed for source reliability, internal consistency, segment-level reconciliation, transaction and user adoption consistency, demand reasonableness, and forecast plausibility.

For more information on the broader research process, please visit our Research Methodology page.

Navigate

Trusted by the world's leading organizations