Report Overview

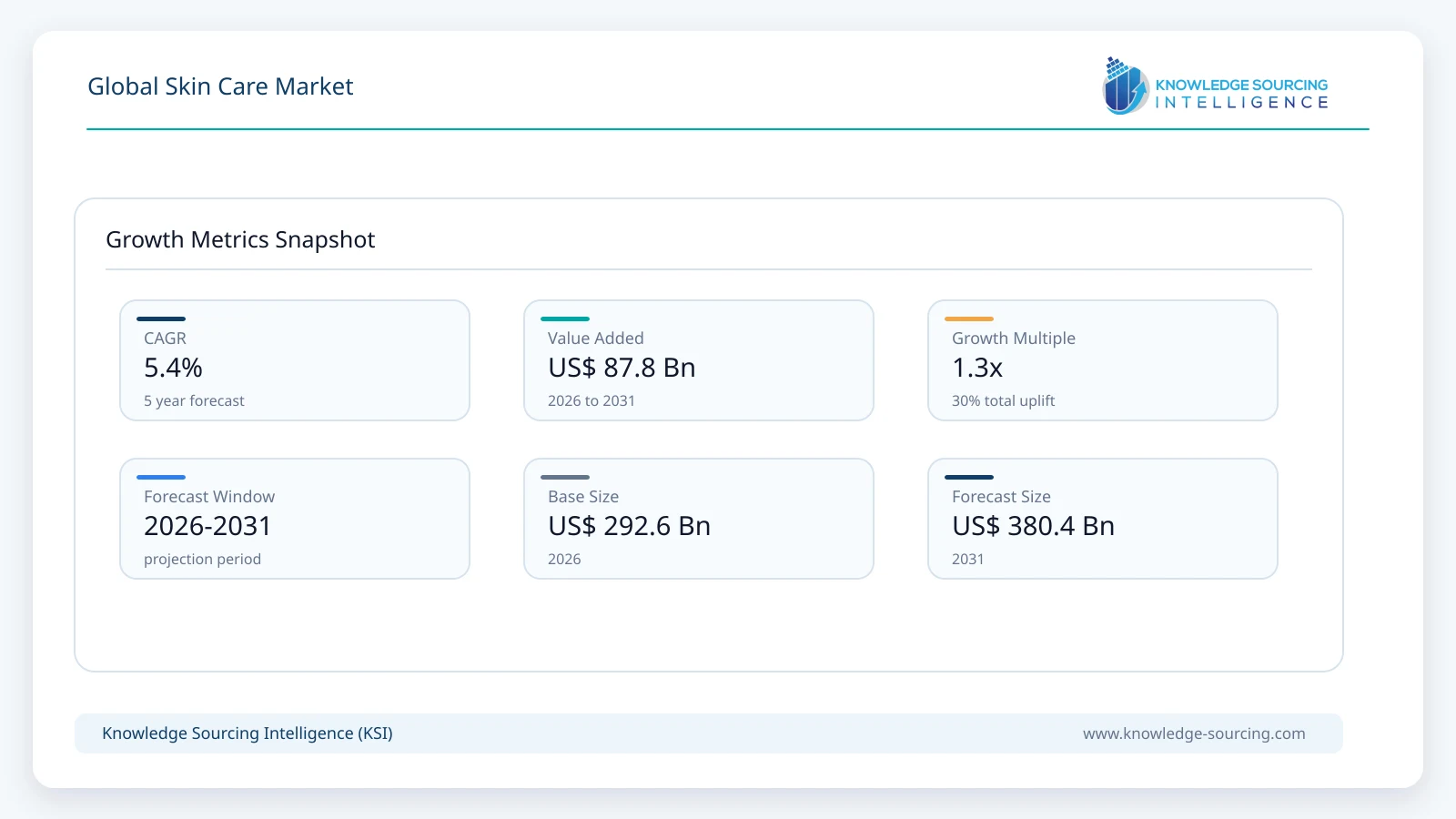

The Global Skincare Market is forecast to grow at a CAGR of 5.39%, reaching USD 380.36 billion in 2031 from USD 292.57 billion in 2026.

Highlights:

- 1Rising consumer focus on preventive skin health and barrier protection continues to support demand across facial and daily care products.

- 2Face care products represent the leading commercial segment due to frequent purchase cycles and product innovation.

- 3Asia Pacific offers substantial long-term opportunities supported by expanding middle-income populations and sophisticated beauty routines.

- 4Artificial intelligence-assisted skin diagnostics and personalized formulation recommendations are improving consumer engagement across online channels.

- 5Product safety regulations, ingredient disclosure requirements, and sustainability policies increasingly shape product development and packaging decisions.

- 6Competition is centered on formulation innovation, dermatological credibility, omnichannel distribution, and premium product differentiation rather than price alone.

The skincare market comprises products developed to maintain, protect, and improve skin health and appearance across facial, body, lip, and sun care applications. It serves consumers of all age groups through preventive, therapeutic, cosmetic, and wellness-oriented products distributed via physical retail networks and digital commerce platforms. Demand originates from daily personal care routines, dermatology-inspired regimens, anti-aging concerns, environmental protection needs, and rising consumer awareness regarding skin health. The market also benefits from growing interest in ingredient transparency, science-backed formulations, and products tailored to different skin types and climatic conditions.

Consumer purchasing decisions increasingly reflect a balance between efficacy, safety, sustainability, and product experience. Buyers seek formulations containing clinically recognized ingredients such as niacinamide, ceramides, retinol, peptides, hyaluronic acid, and vitamin C while paying closer attention to dermatological testing, fragrance content, allergen disclosure, and environmental certifications. Younger consumers are highly influenced by digital education, dermatologist recommendations, and social media product reviews, whereas mature consumers prioritize anti-aging performance, skin barrier restoration, and long-term product reliability.

The industry consists of multinational consumer goods manufacturers, prestige beauty companies, regional brands, contract manufacturers, ingredient suppliers, packaging providers, and specialized dermatological skin care firms. Competition extends beyond pricing, with companies investing in formulation science, clinical validation, sustainable packaging, digital consumer engagement, and omnichannel retail capabilities. Premiumization remains an important revenue contributor despite economic uncertainty, while mass-market brands continue expanding value-oriented offerings through innovation and improved ingredient quality.

Retail channels continue to diversify. Specialty beauty stores, pharmacies, supermarkets, department stores, and direct-to-consumer online platforms each address distinct consumer segments. Digital commerce has strengthened consumer access to personalized product recommendations, subscription models, and educational content, allowing brands to build stronger customer relationships while collecting first-party consumer insights that support product development and targeted marketing.

Market Drivers

Rising consumer emphasis on preventive skin health

Consumers increasingly view skin care as an essential component of overall health rather than purely cosmetic maintenance. Greater awareness of ultraviolet exposure, pollution, stress, and skin barrier function has encouraged consistent use of moisturizers, cleansers, sunscreens, and repair-oriented products. Dermatologists and healthcare professionals continue to educate consumers regarding preventive care, expanding demand beyond traditional beauty-focused buyers.

Manufacturers respond by introducing clinically supported formulations, strengthening dermatologist partnerships, and investing in ingredient research. This approach improves brand credibility while encouraging repeat purchases and higher customer retention, supporting stable revenue generation.

Expansion of science-backed and ingredient-focused purchasing

Modern buyers evaluate ingredient lists with greater scrutiny than previous generations. Clinical evidence, transparent labeling, and dermatologist endorsement increasingly influence purchasing decisions. Consumers actively compare concentrations of active ingredients while seeking products addressing pigmentation, acne, sensitivity, hydration, and signs of aging.

Companies invest in formulation research, clinical studies, and educational marketing to differentiate products. This increases development costs but also supports premium pricing and enhances brand trust among informed consumers.

Digital commerce and personalized consumer engagement

Online retail has changed how consumers discover, evaluate, and purchase skin care products. Artificial intelligence-based skin analysis tools, virtual consultations, educational videos, and personalized recommendations improve conversion rates while expanding access to niche brands.

Direct consumer interaction provides manufacturers with purchasing behavior data that informs inventory planning, product development, and targeted promotions. Digital channels also reduce dependence on traditional retail shelf space, allowing newer brands to compete more effectively.

Premiumization across mature and emerging markets

Consumers increasingly allocate discretionary spending toward products promising measurable performance and superior ingredient quality. Premium facial care, dermatologist-developed formulations, and multifunctional products attract consumers seeking convenience and long-term value.

Manufacturers continue investing in research, sustainable packaging, and premium brand positioning, creating opportunities for higher margins despite inflationary pressure on production costs.

Market Restraints and Challenges

Regulatory complexity across international markets

Ingredient restrictions, labeling standards, product claims, and safety assessments differ substantially across jurisdictions. Manufacturers operating internationally must maintain separate compliance strategies for different regulatory frameworks.

These requirements increase development timelines, testing expenses, and documentation burdens. Larger multinational companies possess greater compliance resources, whereas smaller brands often face higher relative regulatory costs.

Volatility in raw material and packaging costs

Skin care production depends upon specialty chemicals, botanical extracts, fragrances, emulsifiers, preservatives, and packaging materials sourced through global supply networks. Weather events, geopolitical uncertainty, transportation disruptions, and commodity price fluctuations periodically increase procurement costs.

Manufacturers mitigate these risks through supplier diversification, strategic inventory planning, long-term purchasing agreements, and reformulation where commercially feasible.

Consumer skepticism toward marketing claims

Consumers increasingly question unsupported efficacy claims following greater regulatory scrutiny and improved public access to scientific information. Social media also accelerates criticism of products that fail to deliver expected results.

Companies therefore invest in independent clinical testing, transparent communication, dermatologist partnerships, and evidence-based marketing to strengthen consumer confidence and reduce reputational risk.

Market saturation within developed economies

Established markets contain numerous competing brands across every price category. Product differentiation becomes increasingly difficult as comparable active ingredients become widely available.

Companies therefore compete through superior formulation quality, personalized experiences, sustainability initiatives, subscription services, and stronger customer engagement rather than relying solely on new product launches.

Major Segment Analysis

Face Care Products

Face care products represent the most commercially important segment because facial skin receives daily consumer attention and supports frequent product replacement cycles. Moisturizers, cleansers, brightening products, serums, and specialized treatment products collectively generate consistent consumer spending across multiple demographic groups.

Demand continues expanding because consumers increasingly adopt multi-step routines addressing hydration, pigmentation, acne management, environmental protection, and anti-aging objectives. Buyers seek clinically validated formulations suited to specific skin conditions rather than universal products. Personalized recommendations based on age, skin type, climate, and lifestyle further strengthen purchasing confidence.

Competition within face care remains particularly intense due to continual ingredient innovation, dermatologist endorsement, premium positioning, and extensive digital marketing activity. Successful suppliers differentiate through scientific validation, visible performance improvements, elegant product textures, sustainable packaging, and strong consumer education. Since facial care products typically command higher average selling prices than body care products, they remain an important contributor to industry profitability and research investment.

Regional Analysis

North America

North America maintains strong demand supported by high consumer spending on premium personal care products, established dermatology infrastructure, and sophisticated retail distribution. Consumers demonstrate strong interest in clinically supported formulations, clean ingredients, and personalized recommendations. Large retailers, pharmacies, specialty beauty chains, and online platforms provide extensive market access. Inflationary pressures influence discretionary purchases, although premium facial care remains comparatively resilient.

Europe

European demand is shaped by stringent cosmetic safety regulations, environmental sustainability objectives, and consumer preference for scientifically validated products. Manufacturers increasingly prioritize recyclable packaging, responsible ingredient sourcing, and regulatory compliance. Mature retail infrastructure and strong pharmacy channels support premium product sales, while economic conditions encourage balanced demand across both prestige and mass-market categories.

Asia Pacific

Asia Pacific represents the largest long-term expansion opportunity due to rising disposable incomes, urbanization, digital commerce growth, and deeply established skin care routines. Consumers demonstrate high awareness of product innovation, multifunctional formulations, and advanced cosmetic technologies. Regional manufacturers continue expanding internationally while multinational companies increase investments in localized product development tailored to climate, skin types, and consumer preferences.

Middle East & Africa and South America

Demand continues expanding as urban populations grow and organized retail networks strengthen. Rising awareness of sun protection, increasing female workforce participation, and expanding digital commerce contribute to market development. Economic volatility, currency fluctuations, and import dependency remain important commercial constraints, encouraging suppliers to strengthen regional manufacturing and distribution capabilities where feasible.

Competitive Landscape

The competitive environment includes established multinational consumer goods companies, prestige beauty manufacturers, and regionally influential cosmetic producers. Competition is driven by formulation science, dermatological credibility, ingredient innovation, brand equity, and consumer trust rather than solely by pricing.

Companies including L'Oréal S.A., The Estée Lauder Companies Inc., Unilever, The Procter & Gamble Company, Beiersdorf AG, Shiseido Co., Ltd., Johnson & Johnson, Coty Inc., Revlon, Inc., Avon Products, Inc., Amorepacific Corporation, and Kao Corporation continue expanding research capabilities, strengthening digital commerce, improving sustainability performance, and broadening geographic reach. Strategic priorities include partnerships with dermatologists, investment in biotechnology-derived ingredients, personalized consumer experiences, environmentally responsible packaging, and expansion across high-growth emerging economies.

Recent Developments

June 2026: L'Oréal Groupe and OpenAI announced a strategic collaboration at VivaTech 2026 to develop AI-powered beauty solutions, supporting more advanced skin diagnostics, formulation development, and personalized skincare experiences.

June 2026: L'Oréal Groupe announced an agreement to acquire a majority stake in Innovist, a leading Indian digital-first personal care company, strengthening its skincare and personal care portfolio in India's rapidly growing beauty market.

March 2026: Reale Actives, founded by Alix Earle with dermatologist Dr. Kiran Mian, officially launched its first acne-focused skincare range featuring four clinically inspired products designed for acne-prone skin.

Regulatory and Policy Environment

The skin care market operates within comprehensive regulatory frameworks governing cosmetic safety, manufacturing quality, labeling accuracy, ingredient approval, and advertising claims. Authorities including the European Commission, the U.S. Food and Drug Administration, Health Canada, Japan's Ministry of Health, Labour and Welfare, and comparable national regulators establish product safety requirements before commercialization.

Environmental policies increasingly influence packaging material selection, recycling targets, and waste reduction initiatives. Manufacturers also face growing expectations regarding supply chain transparency, responsible sourcing, and chemical safety documentation. Product claims related to efficacy, dermatological testing, and environmental benefits receive closer regulatory scrutiny, encouraging companies to strengthen scientific substantiation and compliance systems.

Outlook and Strategic Implications

Over the next five years, investment is expected to concentrate on formulation science, biotechnology-derived ingredients, digital skin diagnostics, sustainable packaging, and personalized consumer experiences. Procurement teams will continue diversifying ingredient sourcing to improve resilience against supply chain disruptions while maintaining consistent product quality.

Artificial intelligence-supported product recommendations, consumer data analytics, and connected digital platforms will strengthen customer engagement and improve product development efficiency. Companies capable of combining scientific credibility, regulatory compliance, environmental responsibility, and effective omnichannel distribution are likely to strengthen competitive positioning.

Commercial risks include persistent raw material cost volatility, evolving regulatory requirements, changing consumer preferences, and heightened competition across both premium and value-oriented product categories. Nevertheless, consistent demand for preventive skin health, daily facial care, clinically validated formulations, and personalized skin care solutions provides a stable foundation for long-term industry expansion. Manufacturers that continue investing in scientific research, consumer education, sustainable innovation, and geographically diversified operations are expected to capture the strongest commercial opportunities throughout the forecast period.

Skin Care Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 292.57 billion |

| Total Market Size in 2031 | USD 380.36 billion |

| Forecast Unit | Billion |

| Growth Rate | 5.39% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Product, Distribution Channel, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Product

By Distribution Channel

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. GLOBAL SKIN CARE MARKET BY PRODUCT

4.1. Introduction

4.2. Face Care Products

4.2.1. Face Moisturizers

4.2.2. Brightening Products

4.2.3. Cleansers and Toners

4.2.4. Others

4.3. Body Care Products

4.4. Sun Care Products

4.5. Lip Care Products

5. GLOBAL SKIN CARE MARKET BY DISTRIBUTION CHANNEL

5.1. Introduction

5.2. Online

5.3. Offline

6. GLOBAL SKIN CARE MARKET BY GEOGRAPHY

6.1. Introduction

6.2. North America

6.2.1. By Product

6.2.2. By Distribution Channel

6.2.3. By Country

6.2.3.1. USA

6.2.3.2. Canada

6.2.3.3. Mexico

6.3. South America

6.3.1. By Product

6.3.2. By Distribution Channel

6.3.3. By Country

6.3.3.1. Brazil

6.3.3.2. Argentina

6.3.3.3. Others

6.4. Europe

6.4.1. By Product

6.4.2. By Distribution Channel

6.4.3. By Country

6.4.3.1. United Kingdom

6.4.3.2. Germany

6.4.3.3. France

6.4.3.4. Spain

6.4.3.5. Italy

6.4.3.6. Others

6.5. Middle East and Africa

6.5.1. By Product

6.5.2. By Distribution Channel

6.5.3. By Country

6.5.3.1. Saudi Arabia

6.5.3.2. UAE

6.5.3.3. Israel

6.5.3.4. Others

6.6. Asia Pacific

6.6.1. By Product

6.6.2. By Distribution Channel

6.6.3. By Country

6.6.3.1. China

6.6.3.2. Japan

6.6.3.3. India

6.6.3.4. South Korea

6.6.3.5. Taiwan

6.6.3.6. Thailand

6.6.3.7. Indonesia

6.6.3.8. Others

7. COMPETITIVE ENVIRONMENT AND ANALYSIS

7.1. Major Players and Strategy Analysis

7.2. Market Share Analysis

7.3. Mergers, Acquisitions, Agreements, and Collaborations

7.4. Competitive Dashboard

8. COMPANY PROFILES

8.1. L'Oréal S.A.

8.2. The Estée Lauder Companies Inc.

8.3. Unilever

8.4. The Procter & Gamble Company

8.5. Beiersdorf AG

8.6. Shiseido Co., Ltd.

8.7. Johnson & Johnson

8.8. Coty Inc.

8.9. Revlon, Inc.

8.10. Avon Products, Inc.

8.11. Amorepacific Corporation

8.12. Kao Corporation

9. APPENDIX

9.1. Currency

9.2. Assumptions

9.3. Base and Forecast Years Timeline

9.4. Key Benefits for Stakeholders

9.5. Research Methodology

9.6. Abbreviations

Navigate

Trusted by the world's leading organizations