Report Overview

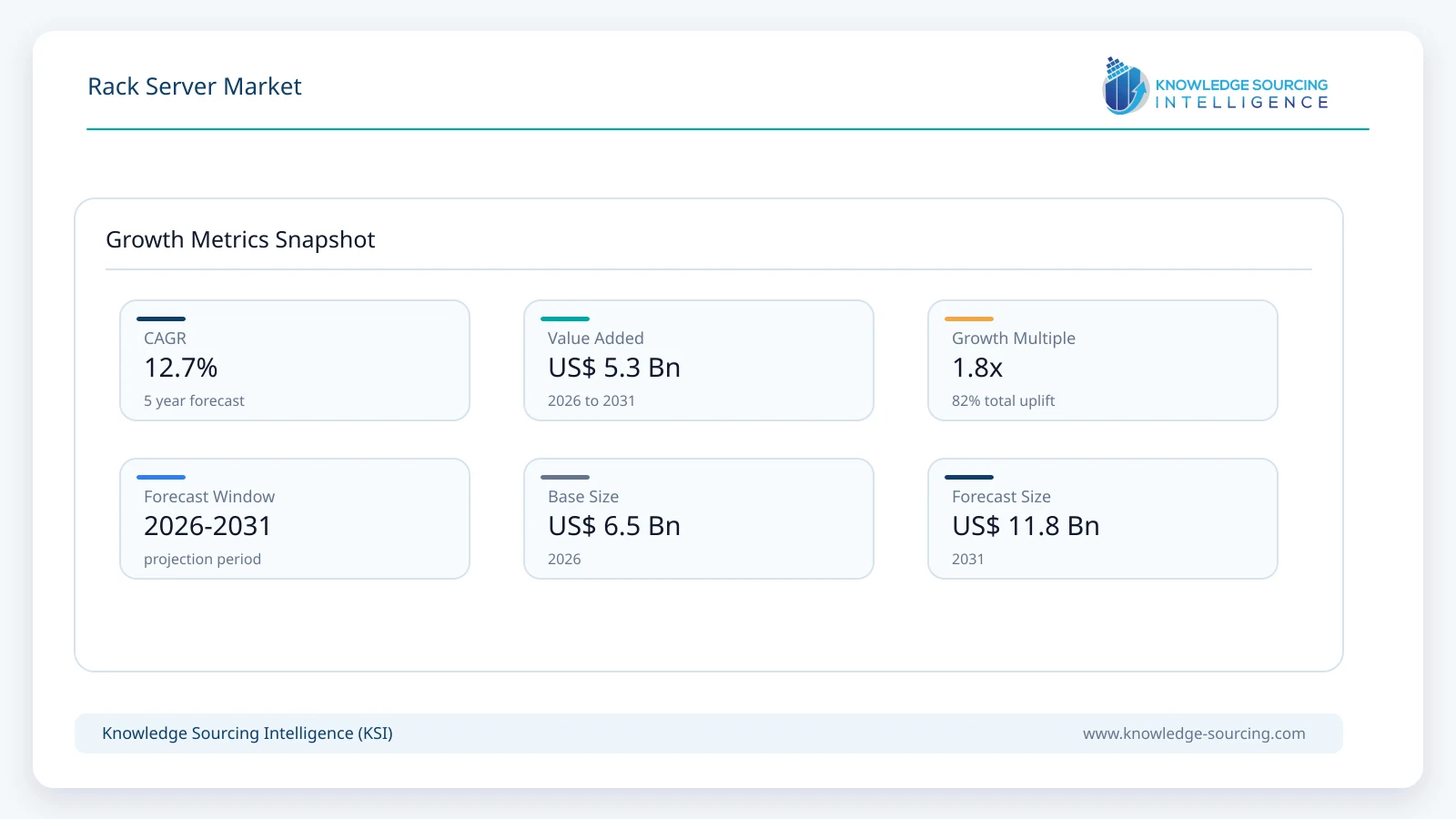

The Rack Server Market is forecast to grow at a CAGR of 12.69%, reaching USD 11.83 billion in 2031 from USD 6.51 billion in 2026.

Highlights:

- 1Rising enterprise AI adoption and hybrid cloud deployment remain the primary demand catalyst for rack server investments.

- 2Large enterprises represent the most commercially important customer segment due to continuous infrastructure modernization programs.

- 3Asia Pacific continues to attract substantial investment through hyperscale data center expansion and digital infrastructure development.

- 4GPU-enabled rack servers and liquid-cooled platforms are becoming increasingly important for high-density computing workloads.

- 5Government cybersecurity regulations and data sovereignty requirements are encouraging localized server deployments across multiple industries.

- 6Competition is increasingly based on platform efficiency, lifecycle management software, sustainability performance, and infrastructure services.

The rack server market forms a core segment of enterprise computing infrastructure, supplying standardized server platforms that are installed within equipment racks across data centers, enterprise IT facilities, telecommunications networks, and edge computing locations. Rack servers provide scalable compute capacity for virtualization, cloud services, artificial intelligence (AI) workloads, enterprise databases, software-defined storage, and mission-critical business applications. Their modular architecture allows organizations to optimize space utilization, simplify maintenance, and expand computing resources without redesigning underlying infrastructure.

Demand for rack servers is increasingly linked to enterprise modernization strategies rather than routine hardware replacement. Organizations are consolidating legacy server estates, deploying hybrid cloud architectures, and expanding AI-ready infrastructure that requires higher processor density, memory capacity, accelerated networking, and GPU compatibility. Procurement decisions increasingly emphasize workload optimization, energy efficiency, lifecycle operating costs, remote infrastructure management, and interoperability with existing virtualization platforms instead of focusing solely on hardware specifications.

Enterprise purchasing behavior continues to shift toward infrastructure investments supporting digital business continuity, cybersecurity resilience, and data-intensive applications. Financial institutions require low-latency processing environments, telecommunications operators are upgrading infrastructure to accommodate 5G network traffic, healthcare providers are expanding digital imaging and electronic health record systems, while manufacturers are implementing industrial automation platforms requiring localized computing capabilities. These developments continue to broaden commercial demand across multiple industries.

The supplier ecosystem combines established enterprise infrastructure vendors with specialized server manufacturers capable of supporting hyperscale cloud operators and custom-built computing environments. Vendors increasingly differentiate through integrated infrastructure management software, liquid cooling compatibility, AI workload optimization, flexible processor architectures, sustainability initiatives, and long-term service contracts. Customers frequently evaluate suppliers based on infrastructure reliability, global support capabilities, firmware security, supply continuity, and total cost of ownership over multi-year deployment cycles.

Hardware innovation has become an important revenue driver within the market. Higher core-count processors, PCIe Gen5 connectivity, DDR5 memory adoption, NVMe storage expansion, GPU acceleration, and advanced networking technologies have increased the commercial value of modern rack server platforms. Enterprises are replacing aging infrastructure not only because of hardware depreciation but also because newer server generations deliver measurable improvements in energy efficiency and application performance, reducing operational expenditure throughout deployment lifecycles.

Procurement models are also evolving. Organizations increasingly prefer infrastructure delivered through consumption-based pricing, managed services, and integrated solutions combining servers, storage, networking, and software management. This purchasing model reduces capital expenditure while providing operational flexibility, particularly among organizations managing variable workloads or expanding cloud-connected environments.

Market Drivers

Expansion of AI and High-Performance Computing Infrastructure

Artificial intelligence training, inference applications, and scientific computing require computing environments capable of supporting high processor utilization, accelerator integration, and large memory configurations. Enterprises investing in AI infrastructure increasingly procure rack servers designed to accommodate GPU clusters and high-speed networking fabrics.

Buyers prioritize compute density, thermal efficiency, and future scalability when selecting server platforms. Suppliers have responded by introducing AI-optimized server architectures supporting advanced cooling technologies, modular accelerator configurations, and high-bandwidth memory compatibility. These capabilities strengthen revenue opportunities within premium enterprise infrastructure deployments.

Growth in Hyperscale and Colocation Data Centers

Cloud service providers and colocation operators continue expanding global data center capacity to satisfy enterprise migration toward cloud-native applications and digital services. Rack servers remain the primary compute platform supporting virtualization, containerized workloads, storage infrastructure, and customer-hosted applications.

Large procurement contracts favor suppliers capable of delivering standardized hardware configurations, predictable supply chains, and rapid deployment schedules. Volume purchasing agreements improve manufacturing efficiency while intensifying competition among vendors seeking long-term infrastructure partnerships.

Enterprise Infrastructure Refresh Cycles

Many organizations continue operating server fleets approaching the end of their recommended operational lifecycle. Aging infrastructure increases maintenance costs, limits application performance, and consumes considerably more electricity than modern server platforms.

Replacement investments are driven by operational efficiency rather than hardware age alone. Procurement teams increasingly evaluate lifecycle energy savings, automation capabilities, remote management features, and compatibility with software-defined infrastructure before approving capital expenditure.

Telecommunications Network Modernization

Deployment of 5G infrastructure, edge computing facilities, and network function virtualization has increased demand for compact yet powerful rack servers supporting distributed computing environments.

Telecommunications operators require reliable hardware capable of operating continuously while supporting virtualized network workloads with minimal latency. Vendors have expanded ruggedized server portfolios and integrated remote monitoring capabilities to address these operational requirements.

Market Restraints and Challenges

High Capital Investment Requirements

Enterprise-grade rack servers require considerable investment, particularly when deployed alongside networking equipment, storage systems, cooling infrastructure, and backup power solutions. Budget limitations remain particularly challenging for smaller organizations planning infrastructure modernization.

Many buyers address this constraint through phased deployment strategies, infrastructure leasing, or consumption-based procurement models that distribute investment over longer periods.

Supply Chain Volatility for Critical Components

Advanced processors, memory modules, GPUs, and networking components remain subject to periodic supply constraints caused by semiconductor manufacturing concentration and geopolitical uncertainties.

Component shortages extend delivery timelines and complicate procurement planning for hyperscale operators and enterprise customers. Manufacturers increasingly diversify sourcing strategies while maintaining higher inventory levels for strategic components.

Rising Data Center Energy Consumption

Power availability has become a critical consideration in enterprise infrastructure planning. Higher-density rack servers supporting AI applications require greater electrical capacity and advanced cooling technologies, increasing operating costs for facility owners.

Organizations increasingly evaluate server efficiency ratings, processor power optimization, airflow design, and liquid cooling compatibility before purchasing new infrastructure.

Cybersecurity and Firmware Risk Management

Hardware-level cyber threats have elevated the importance of secure server architecture. Organizations require secure boot processes, firmware validation, hardware root-of-trust technologies, and continuous vulnerability management.

Meeting these requirements increases development costs but also creates opportunities for vendors capable of demonstrating strong security credentials throughout the hardware lifecycle.

Major Segment Analysis

Large Enterprises

Large enterprises represent the most commercially influential customer segment because they maintain extensive computing infrastructure supporting thousands of business applications across geographically distributed operations. Banking institutions, multinational manufacturers, cloud providers, retailers, and telecommunications companies continuously expand server capacity to accommodate business growth, cybersecurity requirements, regulatory compliance, and digital service delivery.

Procurement decisions within this segment involve comprehensive technical evaluations extending beyond processor performance. Buyers assess lifecycle operating costs, management software integration, hardware reliability, sustainability metrics, warranty coverage, and global technical support capabilities. Multi-year framework agreements are common, creating predictable revenue streams for infrastructure suppliers while strengthening long-term customer relationships.

Competitive differentiation increasingly depends on delivering integrated infrastructure ecosystems rather than standalone servers. Vendors offering automation software, predictive maintenance capabilities, AI workload optimization, and hybrid cloud compatibility strengthen their position within enterprise procurement programs. As infrastructure refresh cycles accelerate, this segment is expected to remain the principal revenue contributor across the rack server market.

Regional Analysis

North America remains the largest demand center due to extensive hyperscale cloud infrastructure, AI investment, enterprise software development, and mature colocation markets. Technology companies continue expanding data center capacity while financial institutions and healthcare providers modernize computing infrastructure. Government cybersecurity initiatives and domestic semiconductor investment further support enterprise infrastructure spending.

Europe demonstrates stable demand supported by industrial digitalization, financial services modernization, and strict data governance regulations. Organizations increasingly deploy localized computing infrastructure to satisfy data residency requirements while improving operational resilience. Energy efficiency regulations also encourage replacement of legacy server equipment with more efficient platforms.

Asia Pacific represents the strongest investment destination because of expanding cloud adoption, government-backed digital infrastructure initiatives, manufacturing automation, and rapidly growing internet economies. China, India, Japan, South Korea, and Australia continue investing in hyperscale facilities, enterprise cloud infrastructure, and AI computing resources. Regional manufacturing capability also strengthens supply chain competitiveness.

Middle East and Africa continues expanding through national digital economy programs, smart city investments, financial sector modernization, and telecommunications infrastructure development. Although infrastructure maturity varies considerably across countries, public-sector technology investment supports gradual market expansion.

South America experiences moderate demand driven by financial services modernization, cloud migration, and telecommunications infrastructure upgrades. Economic volatility occasionally delays enterprise capital expenditure, but continued investment in digital services supports long-term infrastructure demand.

Competitive Landscape

Competition within the rack server market is characterized by established enterprise infrastructure vendors competing alongside specialized manufacturers serving hyperscale cloud providers and customized computing deployments. Dell Technologies Inc., Hewlett Packard Enterprise (HPE), Lenovo Group Limited, Super Micro Computer, Inc., Fujitsu Limited, Cisco Systems, Inc., GIGABYTE Technology Co., Ltd., ASUSTeK Computer Inc., Quanta Cloud Technology (QCT), and Intel Corporation compete through platform performance, workload optimization, infrastructure management capabilities, energy efficiency, and global service networks.

Product differentiation increasingly focuses on AI-ready server architectures, advanced cooling technologies, GPU integration, remote lifecycle management, firmware security, and compatibility with hybrid cloud environments. Strategic partnerships involving processor vendors, accelerator manufacturers, cloud service providers, and software companies enable suppliers to deliver integrated infrastructure solutions addressing evolving enterprise computing requirements. Geographic expansion, localized manufacturing capabilities, and long-term enterprise support services remain important competitive factors as procurement becomes increasingly relationship-driven.

Recent Developments

June 2026: Dell Technologies introduced the PowerEdge XE8812 server, powered by NVIDIA Vera Rubin NVL4 architecture, delivering up to 144 GPUs per rack to support high-performance computing and large-scale AI infrastructure within the Dell AI Factory portfolio.

June 2026: Supermicro launched 12 new server platforms optimized for Intel Xeon 6+ processors across its Hyper, SuperBlade, FlexTwin, and GrandTwin families, enabling higher rack density, lower power consumption, and improved total cost of ownership for cloud and enterprise data centers.

June 2025: Hewlett Packard Enterprise expanded its AI infrastructure portfolio by introducing additional enterprise server solutions optimized for large-scale AI deployments. Commercial relevance: The launch strengthened enterprise adoption of AI-ready rack server infrastructure.

Regulatory and Policy Environment

The rack server market is influenced by cybersecurity regulations, environmental policies, data protection legislation, and energy efficiency standards. Data residency requirements in several jurisdictions encourage enterprises to maintain localized computing infrastructure, supporting investments in domestic data centers and enterprise server deployments.

Cybersecurity frameworks increasingly require secure hardware architectures incorporating firmware integrity verification, encryption capabilities, hardware root-of-trust technologies, and continuous security updates. Compliance with standards published by organizations such as ISO, IEC, and national cybersecurity agencies has become an important purchasing criterion for government agencies, financial institutions, and healthcare providers.

Environmental policies are also shaping procurement decisions. Data center operators face increasing pressure to improve power usage effectiveness, reduce greenhouse gas emissions, and deploy more energy-efficient computing equipment. These requirements encourage adoption of higher-efficiency processors, advanced cooling technologies, and recyclable hardware components while influencing long-term infrastructure planning.

Government incentives supporting semiconductor manufacturing, domestic digital infrastructure, AI research, and cloud computing investments further strengthen demand for enterprise server deployments across several major economies.

Outlook and Strategic Implications

Investment priorities over the 2026–2031 period will increasingly favor infrastructure capable of supporting AI applications, hybrid cloud operations, edge computing, and high-density enterprise workloads. Organizations are expected to prioritize server platforms that combine computational performance with measurable improvements in operational efficiency and infrastructure automation.

Procurement strategies will continue shifting toward consumption-based infrastructure models, integrated hardware-software ecosystems, and lifecycle service agreements that simplify deployment and maintenance. Buyers will evaluate suppliers based on scalability, cybersecurity resilience, energy efficiency, and long-term operating costs rather than initial acquisition price alone.

Competitive positioning will increasingly depend on AI optimization, advanced cooling compatibility, secure hardware design, supply chain resilience, and software-driven infrastructure management. Vendors capable of integrating compute, networking, storage, and automation within unified enterprise platforms are likely to strengthen their commercial position.

Risks remain associated with semiconductor supply disruptions, energy availability for large-scale data centers, geopolitical trade restrictions, and evolving cybersecurity requirements. Nevertheless, sustained investment in cloud infrastructure, enterprise modernization, telecommunications expansion, and AI computing provides a favorable long-term foundation for continued demand across the global rack server market.

Rack Server Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 6.51 billion |

| Total Market Size in 2031 | USD 11.83 billion |

| Forecast Unit | Billion |

| Growth Rate | 12.69% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Type, Enterprise Size, End-User, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Type

By Enterprise Size

By End-user

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. RACK SERVER MARKET BY TYPE

5.1. Introduction

5.2. 1U Rack Servers

5.3. 2U Rack Servers

5.4. 4U and Above Rack Servers

5.5. Others

6. RACK SERVER MARKET BY ENTERPRISE SIZE

6.1. Introduction

6.2. Small and Medium Enterprises (SMEs)

6.3. Large Enterprises

7. RACK SERVER MARKET BY END-USER

7.1. Introduction

7.2. IT & Telecommunications

7.3. BFSI

7.4. Government & Defense

7.5. Healthcare

7.6. Manufacturing

7.7. Retail & E-commerce

7.8. Others

8. RACK SERVER MARKET BY GEOGRAPHY

8.1. Introduction

8.2. North America

8.2.1. United States

8.2.2. Canada

8.2.3. Mexico

8.3. South America

8.3.1. Brazil

8.3.2. Argentina

8.3.3. Others

8.4. Europe

8.4.1. United Kingdom

8.4.2. Germany

8.4.3. France

8.4.4. Spain

8.4.5. Others

8.5. Middle East and Africa

8.5.1. Saudi Arabia

8.5.2. UAE

8.5.3. Others

8.6. Asia Pacific

8.6.1. China

8.6.2. Japan

8.6.3. India

8.6.4. South Korea

8.6.5. Australia

8.6.6. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Competitive Dashboard

10. COMPANY PROFILES

10.1. Dell Technologies Inc.

10.2. Hewlett Packard Enterprise (HPE)

10.3. Lenovo Group Limited

10.4. Super Micro Computer, Inc.

10.5. Fujitsu Limited

10.6. Cisco Systems, Inc.

10.7. GIGABYTE Technology Co., Ltd.

10.8. ASUSTeK Computer Inc.

10.9. Quanta Cloud Technology (QCT)

10.10. Intel Corporation

11. APPENDIX

11.1. Currency

11.2. Assumptions

11.3. Base and Forecast Years Timeline

11.4. Key Benefits for Stakeholders

11.5. Research Methodology

11.6. Abbreviations

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations