Report Overview

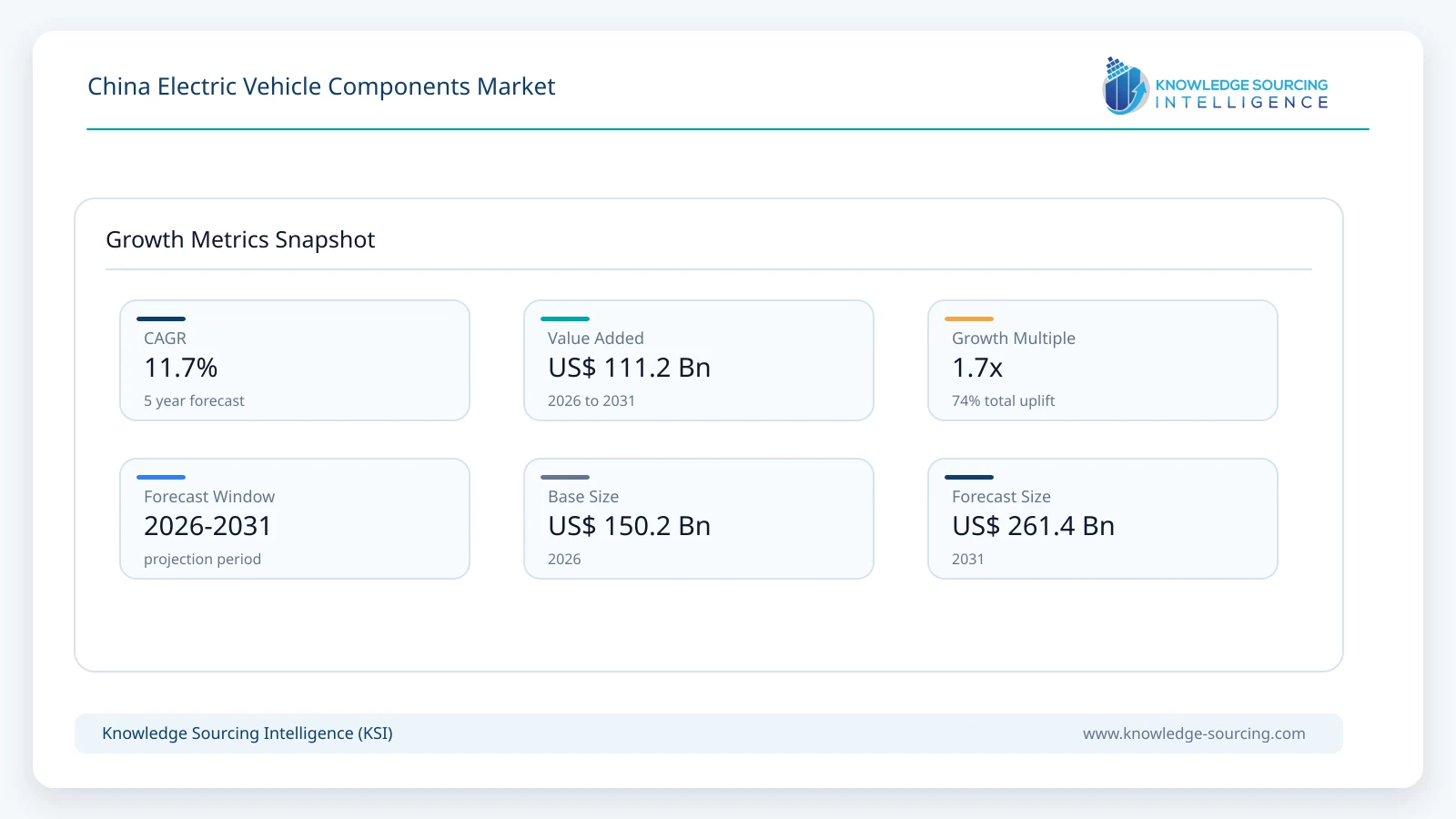

The China Electric Vehicle Components market is forecast to grow at a CAGR of 11.7%, reaching USD 261.4 billion in 2031 from USD 150.2 billion in 2026.

Highlights:

- 1Vehicle electrification is the principal demand catalystNew-energy vehicles accounted for 47.9% of China's new-vehicle sales in 2025, creating a large installed production base for batteries, drive systems, power electronics, thermal systems, and high-voltage architectures.

- 2Battery-related components remain commercially importantBattery safety, durability, charging performance, and energy efficiency are receiving greater regulatory and OEM attention, increasing the technical requirements imposed on battery-system suppliers.

- 3Passenger cars provide the largest addressable production baseHigh-volume passenger-car platforms create recurring demand for integrated electric propulsion, power electronics, thermal management, and charging components.

- 4Component integration is changing supplier economicsIntegrated drive units, battery systems, and thermal architectures can increase the value of individual supplier awards while placing greater engineering and validation responsibilities on component manufacturers.

- 5Regulation is raising technical thresholdsGB 38031-2025 introduced updated traction-battery safety requirements effective July 1, 2026, while GB 18384-2025 updated electric-vehicle safety requirements from the same date.

- 6Charging infrastructure supports utilization and component demandChina's charging network exceeded 20 million facilities by the end of 2025, strengthening the operating ecosystem for electric vehicles across urban and intercity applications.

The China Electric Vehicle Components Market covers the manufacture, supply, integration, and aftermarket replacement of major components used in battery electric vehicles, plug-in hybrid electric vehicles, hybrid electric vehicles, and fuel cell electric vehicles. The scope includes battery packs and battery management systems, electric motors and electric drive units, inverters, DC-DC converters, on-board chargers, thermal management systems, vehicle control units and power electronics, high-voltage cables and connectors, and other supporting components. Demand is assessed across passenger cars, commercial vehicles, two-wheelers, and three-wheelers, with procurement occurring through original equipment manufacturers (OEMs) and aftermarket channels.

The commercial importance of this component ecosystem is tied directly to China's vehicle production scale and the increasing electrical content of each vehicle. China produced 34.53 million vehicles and sold 34.40 million in 2025. New-energy vehicle production reached 16.63 million units and sales reached 16.49 million, representing 47.9% of total new-vehicle sales. This means the component opportunity is no longer confined to a specialist portion of the automotive supply chain; electrified propulsion has become a large-scale production requirement for Chinese vehicle manufacturers.

The demand environment is therefore shaped by vehicle volume, component content per vehicle, platform architecture, energy efficiency requirements, and the purchasing strategies of OEMs. A supplier winning a battery management system, inverter, drive unit, or thermal management contract can obtain multi-year platform revenue, but the award process is demanding. OEMs normally evaluate component suppliers against cost, efficiency, reliability, packaging, thermal performance, software capability, production consistency, delivery security, and the supplier's ability to support vehicle development from prototype through mass production.

China's component industry also benefits from a dense domestic manufacturing base. Battery materials, cells, power electronics, electric motors, semiconductor packaging, thermal systems, aluminum components, wiring systems, and precision machining are increasingly connected through domestic supply networks. This reduces logistics exposure between component stages and allows vehicle manufacturers to modify designs rapidly. At the same time, intense price competition means suppliers must demonstrate measurable cost or performance advantages rather than depend solely on scale.

Buyer behavior differs substantially by component category. Battery-related purchases are driven by energy density, safety, cycle life, charging performance, warranty exposure, and total system cost. Electric-drive procurement places greater weight on power density, efficiency, NVH performance, integration, and software control. Thermal management suppliers are evaluated on the ability to coordinate battery, motor, inverter, passenger-cabin, and charging temperatures within a compact architecture. For high-voltage cables and connectors, electrical safety, insulation performance, packaging, durability, and manufacturing consistency become central purchasing criteria.

The revenue pool is also affected by increasing component integration. OEMs are moving toward more compact electric-drive systems that combine motors, inverters, reduction gears, and associated control electronics. Similar integration is taking place around battery packs, thermal systems, charging systems, and vehicle control electronics. This can reduce the number of discrete components purchased per vehicle while increasing the technical and monetary value of the integrated module. Suppliers that can provide complete systems may therefore compete for a larger portion of vehicle-level spending.

Infrastructure deployment reinforces component demand indirectly. China's National Energy Administration reported 20.092 million electric-vehicle charging facilities by the end of December 2025, including 4.717 million public charging facilities and 15.375 million private facilities. Public charging equipment had an average charging power of approximately 46.53 kW. The same government source reported that more than 98% of highway service areas had charging facilities. Such infrastructure density reduces one of the practical barriers to vehicle electrification and supports continued utilization of electric vehicles, which in turn sustains demand for replacement components and new vehicle platforms.

The market should consequently be viewed as a vehicle-production-driven component industry rather than simply an electric-vehicle accessories market. Its economics depend on platform awards, localization, component integration, manufacturing yield, raw-material exposure, semiconductor availability, warranty requirements, and the ability to meet increasingly specific Chinese technical standards.

No market-size value or CAGR was supplied in the input data. Accordingly, this report description does not introduce an unsupported market valuation or forecast rate for 2026–2031. The forecast-period analysis instead concentrates on the structural factors expected to influence component demand through 2031.

Market Drivers

High New-Energy Vehicle Penetration Is Expanding the Addressable Component Base

The strongest demand mechanism is the rising share of electrified vehicles within China's total automotive production. In 2025, new-energy vehicles represented almost half of new-vehicle sales. For component suppliers, this changes procurement from a niche-volume business into a mainstream automotive supply requirement.

OEM buyers are consequently seeking scalable components that can support multiple vehicle platforms. Battery packs, battery management systems, electric drive units, inverters, thermal management modules, and high-voltage interconnects are being specified at the architecture stage rather than added after vehicle design is established. This favors suppliers that can participate early in engineering programs and demonstrate production readiness before the vehicle enters mass manufacturing.

For suppliers, the commercial implication is a greater opportunity for long-term platform awards but also greater exposure to OEM cost negotiations. Winning volume is not sufficient. Suppliers must preserve margins through manufacturing efficiency, design standardization, common platforms, localized sourcing, and component integration.

Demand for Higher Efficiency and Integrated Powertrains Is Increasing Component Value

Electric vehicles convert electrical energy into motion more efficiently than conventional powertrains, but their commercial performance still depends heavily on losses within motors, inverters, converters, cables, and thermal systems. Every improvement in electrical efficiency can influence vehicle range, charging behavior, battery size, and operating cost.

This creates procurement demand for higher-efficiency motors, compact inverters, improved power semiconductor architectures, low-loss electrical connections, and coordinated thermal management. OEMs also have an economic incentive to reduce the number of separate components by combining functions into integrated modules. A supplier capable of supplying an integrated drive unit may compete on system cost and packaging rather than the price of an individual motor or inverter.

The result is a shift in competitive criteria. Suppliers increasingly need mechanical, electrical, thermal, software, and manufacturing capabilities within the same development program. This raises entry barriers for small suppliers that lack validation infrastructure or production scale.

Government Consumption Policies Continue to Support Vehicle Replacement Demand

Government policy remains an important demand-support mechanism. China's 2025 automobile trade-in program provided subsidies of up to RMB 20,000 for qualifying consumers who scrapped older vehicles and purchased eligible new-energy passenger cars. The 2025 program also allowed a subsidy of up to RMB 15,000 for qualifying new-energy passenger-car replacement transactions.

The 2026 program was renewed with subsidies of up to RMB 20,000 for qualifying vehicle scrappage transactions, while the replacement mechanism provides support based on the new vehicle's purchase price. These programs matter to component suppliers because they influence vehicle replacement volumes rather than directly subsidizing individual components. Higher replacement activity increases OEM production requirements and, consequently, component purchasing.

At the same time, the policy structure is becoming more selective. From 2026 through 2027, new-energy vehicles receive a 50% vehicle purchase-tax reduction rather than the full exemption that applied during 2024–2025, subject to the applicable per-vehicle ceiling. The revised policy also links tax eligibility to updated technical requirements.

This creates a commercial incentive for component suppliers to improve efficiency and compliance. Components that contribute to vehicle energy-consumption performance can influence whether a model satisfies the technical criteria required for policy eligibility.

Charging Infrastructure Expansion Supports Higher Electric-Vehicle Utilization

Infrastructure availability affects the practical economics of vehicle ownership. China's charging network reached 20.092 million charging facilities by the end of 2025, almost doubling from 2024 levels in a comparatively short period. Public facilities totaled 4.717 million, while private facilities reached 15.375 million.

For component suppliers, charging growth supports demand in two ways. First, greater charging availability supports new-vehicle sales. Second, more frequent and diverse charging patterns place greater emphasis on battery durability, charging-system reliability, thermal control, high-voltage connectors, and power electronics.

The deployment of higher-power public charging also changes component specifications. Charging systems must manage greater electrical loads while controlling heat and maintaining safety. This creates opportunities for suppliers of thermal systems, charging electronics, high-voltage connectors, and associated power-management technologies.

Market Restraints and Challenges

OEM Price Pressure Can Compress Component Margins

China's large vehicle production base provides substantial component volumes, but purchasing departments retain strong bargaining power. OEMs frequently compare domestic suppliers against alternative sources and may redesign components to reduce cost. High-volume awards therefore do not automatically translate into attractive margins.

Battery and power-electronics suppliers face particularly strong cost pressure because their products represent material portions of electric-vehicle bill-of-materials costs. Suppliers must offset price reductions through automation, material optimization, higher production yields, platform commonality, and greater vertical integration.

Battery Safety and Reliability Requirements Increase Validation Costs

Battery systems carry a disproportionate share of vehicle safety responsibility. GB 38031-2025 replaced the previous traction-battery safety standard and became effective on July 1, 2026. The revised standard raises the importance of safety testing and system-level engineering.

The commercial impact extends beyond battery manufacturers. Thermal-management suppliers, battery-management-system developers, connectors, pack structures, and control-system providers may all face additional validation requirements. More extensive testing increases engineering expenditure and can lengthen qualification periods for new products.

Raw-Material and Semiconductor Exposure Creates Cost Volatility

Electric-vehicle components use copper, aluminum, permanent-magnet materials, lithium-based battery materials, electronic components, semiconductors, polymers, and engineered thermal materials. Price movements can therefore affect supplier margins even when vehicle volumes remain stable.

Semiconductors introduce a separate risk because inverters, vehicle control units, battery-management systems, DC-DC converters, and chargers require power and control electronics. Suppliers mitigate these risks through multi-source procurement, supplier qualification, inventory planning, localized production, and component redesign where technically feasible.

Technology Cycles Can Reduce the Economic Life of Existing Components

Electric-vehicle platforms are developing faster than conventional vehicle architectures in several areas. New battery chemistries, higher-voltage architectures, integrated drive systems, advanced charging systems, and improved thermal architectures can make older component designs less attractive.

This creates investment risk for suppliers. Production lines built for one architecture may require modification when OEMs migrate to another design. Suppliers must therefore balance dedicated platform investment against modular manufacturing systems that can serve multiple vehicle programs.

Major Segment Analysis

Battery Pack and Battery Management System

The battery pack and battery management system segment is commercially important because it combines the largest energy-storage function of an electric vehicle with a substantial share of its safety, performance, and lifecycle requirements. Battery demand is directly connected to vehicle production, while the technical requirements imposed on batteries influence cell selection, pack architecture, thermal systems, electronics, software, and vehicle controls.

China's scale is visible in battery manufacturing activity. Contemporary Amperex Technology Co., Ltd. reported that its 2025 lithium-ion battery sales reached 661 GWh, while its global production capacity reached 772 GWh at year-end, with another 321 GWh under construction. The company reported RMB 22.1 billion in 2025 R&D investment. These figures illustrate the scale of investment required to compete in advanced battery manufacturing.

OEM purchasing decisions increasingly extend beyond battery price. Buyers evaluate usable energy, fast-charging performance, thermal behavior, safety under abnormal conditions, degradation, warranty exposure, pack dimensions, manufacturing consistency, and integration with vehicle control software. Battery suppliers must therefore compete on a combination of cell chemistry, pack engineering, electronics, software, production yield, and lifecycle economics.

Regulation is strengthening this segment's commercial importance. GB 38031-2025 became effective on July 1, 2026 and sets updated safety requirements for traction batteries. China also introduced GB/T 46991.1-2025 covering durability requirements and test methods for in-vehicle traction batteries in light-duty vehicles, effective July 1, 2026.

These requirements change buyer behavior. OEMs have greater reason to select suppliers with established testing capabilities, traceable manufacturing processes, mature battery-management software, and documented reliability. A low purchase price becomes less attractive if a supplier creates warranty or compliance exposure.

Battery investment is also moving beyond conventional lithium-ion optimization. China's national standards system is developing safety specifications for solid-state batteries. A 2026 national standard project covers safety requirements and test methods for solid-state battery cells used in electric vehicles, with CATL and BYD among the listed drafting participants. This does not mean solid-state batteries will immediately displace current technologies, but it demonstrates that suppliers are preparing for potential architecture changes.

Battery recycling is another commercial consideration. CATL reported that spent-battery recycling reached 210,000 tonnes in 2025, with 24,000 tonnes of lithium salts regenerated. Recycling capability can reduce exposure to primary material supply, create secondary revenue opportunities, and strengthen compliance with future circular-economy requirements.

The principal constraint for this segment is the combination of safety, cost, and technology risk. Suppliers must continue reducing cost without compromising durability or safety. They must also maintain production flexibility as OEMs evaluate different cell chemistries and pack formats. This favors manufacturers with substantial engineering resources and integrated supply chains.

Competitive Landscape

The competitive structure comprises large domestic manufacturers, specialized Chinese component suppliers, global Tier-1 suppliers, and companies with narrower positions in thermal systems, charging equipment, aluminum components, power electronics, and electric-drive technologies. The supplied competitive universe includes BYD Co., Ltd., Contemporary Amperex Technology Co., Ltd. (CATL), Jing-Jin Electric Technologies Co., Ltd., Valeo SA, SONGZ Automobile Air Conditioning Co., Ltd., TKT HVAC Co., Ltd., StarCharge, Sinovation EV, MAHLE GmbH, and Trumony Aluminum Limited.

Competition is not uniform across the component categories. BYD and CATL possess considerable scale in battery-related technologies and benefit from close relationships with vehicle production. Specialized suppliers such as Jing-Jin Electric Technologies compete more directly around electric-drive and power-electronics capabilities. Thermal-management suppliers such as SONGZ Automobile Air Conditioning and TKT HVAC address an area where battery temperature, cabin comfort, motor cooling, and charging performance increasingly intersect.

Global suppliers such as Valeo SA and MAHLE GmbH compete through engineering capabilities, established OEM relationships, product breadth, and international customer coverage. Their competitive proposition differs from suppliers that primarily compete on domestic manufacturing scale and cost. Valeo's product activity illustrates the breadth of electrification-related aftermarket and charging offerings, including electric compressors, DC-DC converters, and EV charging solutions.

StarCharge and Sinovation EV occupy positions connected to electric mobility infrastructure and electrification systems, where integration between vehicle electronics, charging, energy management, and fleet requirements can influence purchasing decisions. Trumony Aluminum Limited has a different competitive position, with aluminum-related capabilities relevant to lightweighting and battery-system structures.

The principal competitive advantage is therefore not simply production capacity. Suppliers compete through platform access, engineering support, localization, quality consistency, cost structure, product integration, and the ability to meet OEM validation schedules. Long-term OEM relationships remain commercially valuable because switching a qualified component supplier can require significant engineering and testing work.

Expansion strategies are likely to favor modular product families, local production near vehicle-manufacturing clusters, deeper customer engineering engagement, and broader system-level offerings. Suppliers that depend on a single component may face greater pricing pressure than companies capable of supplying related functions.

BYD's scale illustrates the benefits of vertical integration. The company reported 2025 new-energy vehicle sales of approximately 4.6 million units and R&D expenditure of RMB 63.4 billion. Such investment supports proprietary technologies and gives the company substantial control over the relationship between vehicle platforms and component development.

Recent Developments

July 2026: China's updated GB 38031-2025 traction-battery safety standard and GB 18384-2025 electric-vehicle safety standard entered into force on July 1, 2026. Commercial relevance: battery and vehicle-component suppliers must meet higher formal safety requirements, increasing validation obligations and strengthening the competitive position of suppliers with established testing and quality systems.

March 2026: CATL released its 2025 annual report, reporting RMB 423.7 billion in revenue, RMB 72.2 billion in net profit, 661 GWh of lithium-ion battery sales, and 772 GWh of global production capacity at year-end 2025. Commercial relevance: the figures demonstrate continued capital deployment and manufacturing scale in China's battery supply chain, raising the competitive threshold for battery-system suppliers.

March 2026: BYD released its 2025 annual results and subsequently reported 2025 new-energy vehicle sales of approximately 4.6 million units, alongside R&D expenditure of RMB 63.4 billion. Commercial relevance: sustained vehicle volume and high R&D spending strengthen the relationship between Chinese OEM scale and internally developed electric-vehicle component technologies.

Regulatory and Policy Environment

China's electric-vehicle component industry operates within a broad regulatory framework covering vehicle safety, battery safety, energy consumption, taxation, product qualification, charging infrastructure, and technical standards. Regulation affects component demand indirectly by determining which vehicle technologies can qualify for incentives and directly by setting minimum performance and safety requirements.

Vehicle purchase-tax policy remains commercially relevant during the forecast period. New-energy vehicles purchased from January 1, 2026 through December 31, 2027 receive a 50% reduction in vehicle purchase tax, subject to the applicable maximum reduction of RMB 15,000 per new-energy passenger vehicle. Eligibility depends on meeting the technical requirements established by the Ministry of Industry and Information Technology, Ministry of Finance, and State Taxation Administration.

The 2026–2027 technical requirements place greater emphasis on vehicle energy consumption. Pure-electric passenger cars must meet the applicable energy-consumption limits under GB 36980.1-2025 to qualify under the relevant tax-reduction framework. This creates an indirect procurement incentive for efficient motors, inverters, power electronics, thermal systems, and other components that influence vehicle energy consumption.

Battery safety requirements have also been strengthened. GB 38031-2025 replaced GB 38031-2020 and became effective July 1, 2026. The new framework raises the importance of battery-system safety evaluation, testing, and compliance.

GB 18384-2025, the updated electric-vehicle safety requirement, also became effective July 1, 2026. Together, these standards make safety compliance a more visible component of supplier qualification.

China is also developing standards for emerging technologies. In 2026, a national standard project was initiated for safety specifications covering solid-state batteries for electric vehicles. The project involves organizations including CATL and BYD among its drafting participants. Such standardization activity reduces uncertainty around future technology adoption and gives component developers clearer technical targets.

Charging infrastructure policy provides another demand channel. The National Energy Administration reported that China's charging network exceeded 20 million facilities by the end of 2025. In September 2025, several government departments also issued a three-year action plan for doubling charging-infrastructure service capacity during 2025–2027.

Tax policy also changed for commercial new-energy vehicles. A July 2026 announcement stated that from January 1, 2027, exemptions from vehicle and vessel tax for pure-electric commercial vehicles, plug-in hybrid commercial vehicles, and fuel-cell commercial vehicles will be removed. This change may influence fleet economics and could affect procurement decisions for commercial vehicles and their components.

For component manufacturers, the regulatory direction creates two requirements. First, suppliers must maintain technical documentation and testing capabilities that support OEM certification. Second, suppliers must anticipate future requirements rather than design products only around current minimum specifications. This is particularly relevant to battery safety, energy efficiency, charging systems, and high-voltage electrical architectures.

Outlook and Strategic Implications

China's electric-vehicle component industry enters 2026–2031 with a large production base and a supply chain that has already achieved substantial scale. The central commercial question is therefore not whether electric vehicles will require components, but which suppliers will capture value as vehicle architectures become more integrated and technically demanding.

Investment priorities are expected to concentrate on battery safety, high-efficiency electric drives, power electronics, thermal management, charging systems, high-voltage architectures, software-enabled control systems, and manufacturing automation. Battery suppliers will need to balance capacity expansion with technology flexibility. Overbuilding capacity without sufficient platform utilization can damage returns, while insufficient capacity can result in lost OEM programs.

Procurement is likely to become more system-oriented. OEMs can reduce engineering complexity by sourcing integrated drive units, integrated thermal modules, intelligent battery systems, and consolidated electrical architectures. This favors suppliers that can demonstrate cross-domain engineering capabilities and maintain production quality at high volumes.

Battery-management systems should become more important as OEMs place greater emphasis on durability, safety, charging behavior, and lifecycle performance. The introduction of updated battery durability and safety standards reinforces this direction. Suppliers with reliable sensing, control algorithms, diagnostic functions, and data-management capabilities can obtain stronger positions within battery-system procurement.

Power electronics will also remain a strategic technology area. Inverters, DC-DC converters, on-board chargers, and vehicle control units determine how efficiently electrical energy moves through the vehicle. Higher-voltage architectures and faster charging increase the need for components capable of handling greater power while maintaining thermal and electrical safety.

Thermal management deserves particular attention because it connects several vehicle functions. Battery charging, fast charging, passenger-cabin heating and cooling, motor operation, inverter performance, and battery longevity can all be affected by temperature. This gives integrated thermal suppliers an opportunity to increase their content per vehicle when OEMs consolidate thermal circuits and controls.

The competitive environment is likely to remain price-sensitive. China's large domestic supplier base gives OEMs considerable sourcing choice. Suppliers that lack differentiated technology may therefore experience continued margin pressure. By contrast, suppliers with proprietary designs, strong testing capabilities, high production yields, and proven platform awards can protect their positions more effectively.

International suppliers face a different strategic challenge. Their engineering expertise and established relationships remain valuable, but they must maintain competitive cost structures within China's domestic supply environment. Localization of engineering and manufacturing can reduce response times and improve cost competitiveness. Domestic suppliers, meanwhile, may seek international expansion as Chinese vehicle manufacturers increase overseas production and exports.

Export activity adds another dimension to the outlook. China's new-energy vehicle exports reached 2.615 million units in 2025, up 103.7% year over year, according to the Ministry of Industry and Information Technology's automotive industry data. As Chinese manufacturers expand overseas, component suppliers with international certification, logistics capabilities, and localized service networks can follow vehicle platforms into foreign markets.

Supply-chain resilience will remain a strategic concern. Component manufacturers must manage exposure to raw-material prices, electronic components, specialized machinery, logistics, and changing technology standards. Multi-sourcing and regional manufacturing can reduce disruption risk, although they may increase fixed costs.

The largest strategic opportunity lies in moving from component supply toward system-level value creation. A supplier that combines hardware, embedded control, thermal management, diagnostics, and manufacturing expertise can participate in a broader portion of an OEM platform. Such positioning also makes the supplier harder to replace after qualification.

At the same time, technology bets require discipline. Solid-state batteries, higher-voltage systems, new power-semiconductor architectures, advanced charging, and increasingly integrated drive systems offer potential long-term opportunities, but commercial adoption will depend on cost, reliability, production yield, and OEM platform timing. Standardization activity around emerging technologies indicates that China is preparing the regulatory foundation for future component architectures, but standard development should not be interpreted as proof of immediate mass adoption.

For investors, suppliers, and OEM procurement teams, five factors warrant close monitoring through 2031: the pace of new-energy vehicle penetration, battery and power-electronics cost curves, changes in safety and energy-efficiency standards, OEM localization strategies, and the migration from individual components toward integrated vehicle systems.

Overall, China's electric-vehicle component industry is moving from volume expansion toward a more demanding phase of technical differentiation. Vehicle production will continue to provide the underlying demand base, but supplier performance will increasingly depend on efficiency, safety, integration, engineering responsiveness, and lifecycle economics. Companies that align manufacturing scale with platform-specific engineering and regulatory readiness should be better positioned to secure durable OEM business during the 2026–2031 forecast period.

China Electric Vehicle Components Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 150.2 billion |

| Total Market Size in 2031 | USD 261.4 billion |

| Forecast Unit | Billion |

| Growth Rate | 11.7% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Component Type, Vehicle Type, Propulsion Type, Sales Channel |

| Companies |

|

Market Segmentation

By Component Type

By Vehicle Type

By Propulsion Type

By Sales Channel

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. China Policies, Standards, and Regulations

3.7. Recent Industry Developments

3.8. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

4.1. Battery Technology

4.2. Electric Motor and Electric Drive Technology

4.3. Power Electronics Technology

4.4. Silicon Carbide (SiC) Power Electronics

4.5. High-Voltage Electric Vehicle Architecture

4.6. Battery Thermal Management Technology

4.7. Integrated Electric Drive Systems

4.8. Fast Charging and High-Power Charging Technology

4.9. Vehicle-to-Grid (V2G) and Bidirectional Charging Technology

5. CHINA ELECTRIC VEHICLE COMPONENTS MARKET BY COMPONENT TYPE

5.1. Introduction

5.2. Battery Pack and Battery Management System

5.3. Electric Motor and Electric Drive Unit

5.4. Inverter

5.5. DC-DC Converter

5.6. On-Board Charger

5.7. Thermal Management System

5.8. Vehicle Control Unit and Power Electronics

5.9. High-Voltage Cables and Connectors

5.10. Other Components

6. CHINA ELECTRIC VEHICLE COMPONENTS MARKET BY VEHICLE TYPE

6.1. Introduction

6.2. Passenger Cars

6.3. Commercial Vehicles

6.4. Two-Wheelers

6.5. Three-Wheelers

7. CHINA ELECTRIC VEHICLE COMPONENTS MARKET BY PROPULSION TYPE

7.1. Introduction

7.2. Battery Electric Vehicle (BEV)

7.3. Plug-in Hybrid Electric Vehicle (PHEV)

7.4. Hybrid Electric Vehicle (HEV)

7.5. Fuel Cell Electric Vehicle (FCEV)

8. CHINA ELECTRIC VEHICLE COMPONENTS MARKET BY SALES CHANNEL

8.1. Introduction

8.2. Original Equipment Manufacturers (OEMs)

8.3. Aftermarket

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Competitive Positioning and Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Competitive Dashboard

10. COMPANY PROFILES

10.1. BYD Co., Ltd.

10.2. Contemporary Amperex Technology Co., Ltd. (CATL)

10.3. Jing-Jin Electric Technologies Co., Ltd.

10.4. Valeo SA

10.5. SONGZ Automobile Air Conditioning Co., Ltd.

10.6. TKT HVAC Co., Ltd.

10.7. StarCharge

10.8. Sinovation EV

10.9. MAHLE GmbH

10.10. Trumony Aluminum Limited

11. APPENDIX

11.1. Currency

11.2. Assumptions

11.3. Base Year and Forecast Period

11.4. Key Benefits for Stakeholders

11.5. Research Methodology

11.6. Abbreviations

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations