Report Overview

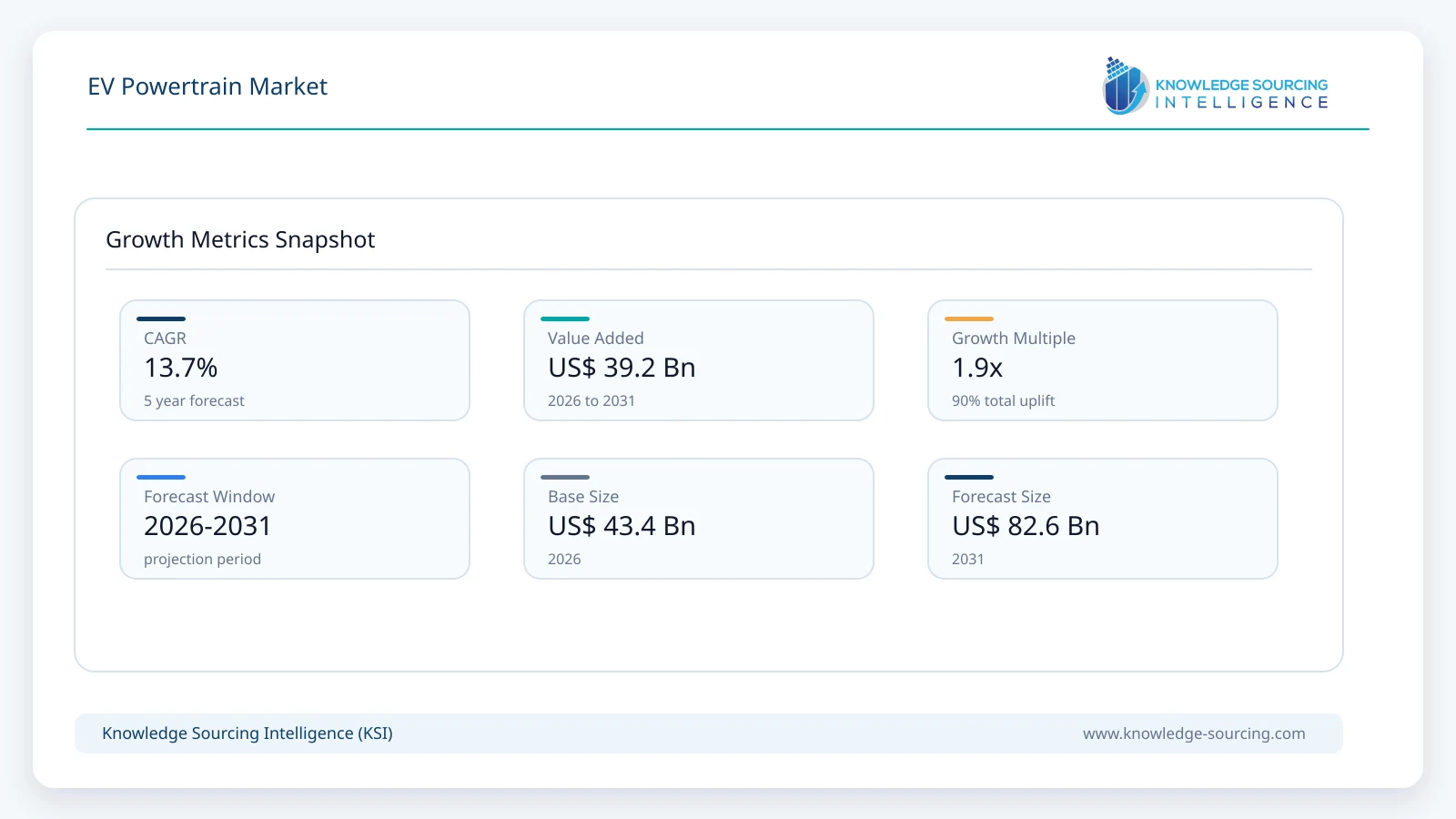

The Global Electric Vehicle (EV) Powertrain market is forecast to grow at a CAGR of 13.7%, reaching USD 82.6 billion in 2031 from USD 43.4 billion in 2026.

Highlights:

- 1Rising global electric vehicle production remains the primary demand catalyst, encouraging automakers to expand investments in integrated electric drive systems and localized component manufacturing.

- 2Battery systemscontinue to represent the most commercially influential component category because they determine vehicle range, charging performance, lifecycle costs, and overall powertrain economics.

- 3Asia Pacific maintains the strongest manufacturing ecosystem through extensive battery production capacity, integrated automotive supply chains, supportive industrial policies, and large-scale EV deployment.

- 4Silicon carbide-based power electronics are gaining wider commercial adoption as manufacturers seek higher drivetrain efficiency, faster charging capability, and improved thermal performance.

- 5Vehicle emission regulations, fuel economy standards, zero-emission vehicle policies, and battery localization initiatives continue influencing supplier selection and investment priorities across major automotive regions.

- 6Competition increasingly centers on complete electric drive unit integration, software capabilities, manufacturing scalability, long-term supply agreements, and lifecycle cost optimization rather than individual component pricing alone.

The EV powertrain market comprises the integrated propulsion systems that convert electrical energy into vehicle motion. These systems include battery packs, electric motors, transmissions or reduction gear units, power electronics such as inverters and converters, onboard charging interfaces, thermal management components, and the associated control software that coordinates energy flow. Unlike conventional internal combustion drivetrains, EV powertrains rely on electrical architecture, semiconductor technologies, and battery management systems to achieve propulsion, efficiency, regenerative braking, and vehicle performance. As vehicle manufacturers expand electrified product portfolios across passenger and commercial vehicle categories, powertrain development has become one of the most strategically important areas of investment within the automotive industry.

Demand for EV powertrains is directly linked to global electric vehicle production rather than vehicle registrations alone. Original equipment manufacturers (OEMs) increasingly seek scalable powertrain platforms that can be deployed across multiple vehicle segments, allowing them to reduce engineering costs while improving manufacturing efficiency. Modular architectures enable manufacturers to standardize electric motors, battery systems, software, and power electronics across several vehicle models without compromising vehicle-specific performance characteristics. This approach shortens development cycles, simplifies procurement, and enhances production flexibility.

Procurement priorities have shifted considerably over the past five years. Automotive manufacturers now evaluate suppliers not only on component pricing but also on energy efficiency, software integration capability, supply security, manufacturing capacity, product reliability, and compliance with regional regulatory requirements. Battery performance remains a primary purchasing consideration because it directly influences vehicle range, charging time, and lifecycle costs. At the same time, electric motors and power electronics have become important differentiators as automakers pursue higher drivetrain efficiency and reduced energy consumption.

Electrification targets established by governments across North America, Europe, and Asia Pacific continue to reshape investment decisions throughout the automotive value chain. Vehicle manufacturers are allocating substantial capital toward dedicated EV platforms, battery manufacturing facilities, semiconductor partnerships, and vertically integrated powertrain production. Several automakers have also expanded in-house development capabilities for electric drive units to improve intellectual property ownership, software control, and cost management. Nevertheless, supplier partnerships remain essential because advanced motor technologies, silicon carbide-based power electronics, and battery system engineering require specialized expertise and significant research investment.

Technology adoption within the EV powertrain market extends beyond hardware innovation. Software increasingly determines overall system efficiency by managing battery charging, regenerative braking, thermal control, torque distribution, and predictive diagnostics. Vehicle manufacturers are integrating advanced electronic control units capable of optimizing power delivery according to driving conditions while supporting over-the-air software updates. This transition strengthens long-term customer value because software improvements can enhance vehicle performance after delivery without replacing physical components.

Commercial vehicle electrification is creating additional demand for specialized powertrain configurations. Delivery fleets, buses, municipal vehicles, and regional logistics operators require propulsion systems optimized for predictable duty cycles, higher payload capacities, and extended operational reliability. Fleet operators typically prioritize total cost of ownership rather than purchase price alone. Consequently, powertrain suppliers increasingly emphasize durability, energy efficiency, maintenance intervals, and battery lifecycle management to address commercial procurement requirements.

The supply chain supporting EV powertrain production has become considerably more diversified than traditional automotive manufacturing. Critical raw materials including lithium, nickel, cobalt, graphite, and rare earth elements influence production economics, while semiconductor availability affects inverter and motor controller manufacturing. Automotive suppliers are therefore expanding regional manufacturing capacity and strengthening long-term sourcing agreements to reduce exposure to geopolitical risks and logistics disruptions. Battery cell localization has become particularly important because transportation costs, regulatory incentives, and domestic content requirements influence procurement strategies in multiple countries.

Automotive manufacturers also face growing pressure to improve manufacturing sustainability. Powertrain production facilities increasingly incorporate renewable electricity, recycled battery materials, water conservation measures, and lower-emission manufacturing processes. Sustainability reporting has evolved into a procurement criterion for several global OEMs, encouraging suppliers to demonstrate measurable reductions in carbon emissions throughout production and logistics operations. This shift extends beyond regulatory compliance and increasingly influences supplier selection during long-term sourcing agreements.

Power electronics represent another area of substantial commercial importance. The transition from conventional silicon semiconductors toward silicon carbide (SiC) devices improves switching efficiency, reduces heat generation, and supports faster charging capabilities. These characteristics enable automakers to reduce system weight while improving driving range and overall vehicle efficiency. As production volumes increase, economies of scale are expected to reduce adoption costs, encouraging broader integration across mid-range and premium electric vehicle platforms.

Buyer behavior continues to evolve alongside technological progress. Premium vehicle manufacturers typically prioritize performance, acceleration, and advanced software integration, whereas mass-market automakers emphasize manufacturing cost optimization and scalable production. Commercial fleet operators concentrate on operational efficiency, serviceability, charging compatibility, and predictable maintenance costs. These varying procurement priorities encourage suppliers to offer differentiated powertrain solutions tailored to specific customer requirements rather than standardized component packages.

Competitive differentiation increasingly depends on system integration capabilities rather than individual component performance alone. Suppliers capable of delivering complete electric drive units that combine electric motors, reduction gears, power electronics, cooling systems, and control software gain commercial advantages by simplifying vehicle assembly and reducing engineering complexity for OEM customers. Integrated solutions also shorten product development timelines, improve packaging efficiency, and reduce vehicle weight, contributing to higher overall drivetrain performance.

Investment activity across the automotive sector further supports market expansion. Vehicle manufacturers continue establishing battery production facilities, motor assembly plants, semiconductor partnerships, and advanced testing centers in proximity to major automotive manufacturing hubs. Governments frequently complement these investments through financial incentives, infrastructure funding, research grants, and industrial development programs designed to strengthen domestic EV supply chains. These initiatives encourage localization while reducing dependence on imported components.

Despite positive long-term demand fundamentals, purchasing decisions remain influenced by battery raw material pricing, charging infrastructure availability, vehicle affordability, and consumer confidence in electric mobility. Automakers therefore balance innovation investments with cost optimization to ensure broader market accessibility. Suppliers capable of simultaneously improving efficiency, reducing manufacturing costs, and maintaining product reliability are expected to strengthen their competitive positions throughout the forecast period.

Overall, the EV powertrain market represents one of the automotive industry's most strategically important technology domains because propulsion systems determine vehicle performance, energy efficiency, operating costs, and regulatory compliance. Continuous advances in battery engineering, electric motors, semiconductor technologies, software integration, and manufacturing localization will continue shaping procurement decisions and competitive positioning across global automotive markets.

Market Drivers

Expansion of Global Electric Vehicle Manufacturing Strengthens Demand for Integrated Powertrain Systems

Electric vehicle production capacity continues expanding across established and emerging automotive manufacturing regions as automakers diversify product portfolios and prepare for stricter emission requirements. New assembly plants require dedicated supply networks capable of delivering batteries, electric motors, power electronics, transmissions, and integrated propulsion modules at high production volumes. This creates sustained demand for powertrain suppliers with scalable manufacturing capabilities and established quality management systems.

Vehicle manufacturers increasingly favor suppliers capable of supporting global production programs across multiple manufacturing locations. Standardized electric drive platforms reduce engineering complexity while enabling faster vehicle launches. Suppliers respond by investing in regional production facilities, digital manufacturing systems, and flexible assembly lines that accommodate multiple vehicle platforms. Commercially, this strengthens long-term supplier relationships because OEMs prioritize manufacturing continuity, consistent quality, and reliable delivery performance over short-term component pricing.

Battery Technology Improvements Influence Vehicle Purchasing Decisions

Battery performance remains one of the most influential factors affecting electric vehicle demand because consumers evaluate vehicles according to driving range, charging convenience, durability, and ownership costs. Improvements in cell chemistry, battery management systems, thermal control, and structural battery design enable automakers to enhance vehicle efficiency without proportionally increasing battery size.

Automotive manufacturers therefore allocate substantial research budgets toward battery integration within the overall powertrain architecture. Suppliers capable of improving energy density while maintaining safety and manufacturing efficiency gain stronger commercial positioning. Better battery performance also reduces lifecycle operating costs, making electric vehicles more attractive to private consumers and commercial fleet operators. Consequently, battery innovation stimulates demand across the broader EV powertrain value chain.

Government Policies Supporting Vehicle Electrification Encourage Industry Investment

National and regional governments continue implementing vehicle emission regulations, zero-emission vehicle targets, manufacturing incentives, and industrial development programs that accelerate electrification investments. Financial support for battery manufacturing, domestic component production, charging infrastructure, and research activities encourages both automotive manufacturers and suppliers to expand powertrain production capacity.

Automakers respond by introducing dedicated EV platforms capable of meeting future regulatory requirements across multiple geographic markets. Suppliers similarly invest in localized engineering centers, production facilities, and testing infrastructure to comply with regional content requirements and reduce logistics costs. These policy measures improve investment confidence while strengthening domestic automotive supply chains and supporting sustained procurement activity.

Commercial Fleet Electrification Expands Demand Beyond Passenger Vehicles

Commercial transportation operators increasingly evaluate electric vehicles based on total ownership costs, predictable maintenance schedules, fuel savings, and regulatory compliance. Urban delivery services, municipal transit agencies, logistics providers, and corporate fleet operators represent important buyers of electric commercial vehicles equipped with specialized powertrain systems.

Fleet procurement differs substantially from retail vehicle purchasing because operators prioritize reliability, operational uptime, battery durability, and service support. Powertrain suppliers therefore develop products optimized for higher utilization rates, heavier payloads, and continuous daily operation. This commercial demand encourages investments in durable electric motors, advanced thermal management systems, and predictive maintenance technologies capable of reducing vehicle downtime throughout operational lifecycles.

Advancements in Power Electronics and Software Improve System Efficiency

Power electronics have become central to overall EV powertrain performance because they regulate electrical energy transfer between batteries, electric motors, charging systems, and auxiliary vehicle components. The adoption of silicon carbide semiconductors enables higher switching frequencies, lower energy losses, reduced cooling requirements, and improved charging efficiency compared with conventional silicon devices.

Software integration further enhances system performance through intelligent energy management, regenerative braking optimization, thermal regulation, and real-time diagnostics. Automotive manufacturers increasingly seek suppliers capable of combining hardware engineering with advanced control software, enabling continuous performance improvements through software updates. This integrated approach creates commercial differentiation while supporting higher vehicle efficiency, improved customer satisfaction, and stronger long-term supplier relationships.

Market Restraints and Challenges

High Battery Material Costs and Supply Chain Uncertainty Affect Powertrain Economics

Battery systems represent the largest cost component within an electric vehicle powertrain, making raw material availability and pricing a critical factor for manufacturers and suppliers. Materials such as lithium, nickel, cobalt, graphite, and manganese influence battery production costs, while fluctuations in commodity markets directly affect powertrain pricing strategies. Supply concentration in specific geographic regions also creates procurement risks for manufacturers seeking stable long-term production.

Automotive OEMs, battery manufacturers, and powertrain suppliers are affected by these cost pressures because battery pricing determines vehicle affordability and profit margins. Higher material costs can delay price reductions required for wider EV adoption, particularly in cost-sensitive passenger vehicle segments and emerging markets. Commercial fleet operators may also postpone electrification investments if upfront vehicle costs remain higher than comparable internal combustion alternatives.

Industry participants are addressing these challenges through several approaches, including investment in alternative battery chemistries, long-term mineral supply agreements, recycling initiatives, and regionalized production networks. The adoption of lithium iron phosphate (LFP) batteries in selected vehicle segments has reduced dependence on some expensive materials, while battery recycling programs aim to recover valuable materials and improve supply security. However, achieving large-scale recycling capacity remains a gradual process because the current volume of end-of-life EV batteries is still limited compared with future expected demand.

Semiconductor Availability and Electronic Component Constraints Impact Production Planning

Modern EV powertrains depend heavily on semiconductors used in inverters, battery management systems, motor controllers, charging systems, and vehicle control units. Unlike conventional vehicles, electric vehicles require significantly greater electronic integration, increasing exposure to semiconductor supply constraints. The availability of advanced chips, including silicon carbide and gallium nitride-based components, directly affects manufacturing schedules and product development timelines.

Automotive OEMs and powertrain suppliers face challenges in securing reliable semiconductor supplies because chip manufacturing requires specialized facilities, extended production cycles, and substantial capital investment. Supply disruptions can create production bottlenecks even when demand for electric vehicles remains strong. Smaller suppliers often experience greater pressure because they have less purchasing influence compared with global automotive manufacturers.

To mitigate these risks, companies are developing direct partnerships with semiconductor manufacturers, increasing component inventories, and redesigning systems to support alternative chip configurations. Governments in major automotive regions are also encouraging domestic semiconductor manufacturing through industrial policies aimed at improving supply chain resilience. Despite these efforts, semiconductor dependency remains a structural challenge for the EV powertrain ecosystem.

Charging Infrastructure Limitations Influence Electric Vehicle Adoption and Powertrain Demand

The expansion of EV powertrain demand depends partly on the availability of charging infrastructure. While vehicle manufacturers continue introducing new electric models, charging network development remains uneven across countries and regions. Limited public charging availability, insufficient fast-charging locations, and grid capacity constraints can influence consumer confidence and fleet electrification decisions.

Passenger vehicle buyers often consider charging convenience when selecting electric vehicles, especially in markets where residential charging options are limited. Commercial fleet operators face additional challenges because large-scale electrification requires dedicated charging facilities, grid upgrades, and operational planning. These infrastructure requirements increase the total investment needed for fleet conversion.

Powertrain suppliers are indirectly affected because slower EV adoption can delay vehicle production expansion and reduce component demand. Companies are responding by improving battery efficiency, supporting faster charging technologies, and developing powertrain systems optimized for different charging environments. However, infrastructure investment remains dependent on cooperation between governments, utilities, charging operators, and automotive manufacturers.

Complex Manufacturing Requirements Increase Capital Investment Needs

EV powertrain production requires specialized manufacturing capabilities, including precision motor assembly, battery integration, thermal management systems, semiconductor processing, and advanced testing facilities. Establishing these capabilities requires significant capital expenditure and technical expertise, creating entry barriers for new suppliers and increasing financial pressure on existing automotive component manufacturers.

Traditional automotive suppliers transitioning from internal combustion components must invest in new engineering capabilities, workforce training, production equipment, and quality validation processes. Companies with established mechanical manufacturing expertise may need additional capabilities in electrical engineering, software development, and battery technologies to remain competitive.

The transition also creates operational complexity because manufacturers must manage parallel production systems during the shift from conventional drivetrains to electric architectures. Maintaining profitability during this transition period requires careful capacity planning, efficient resource allocation, and strategic partnerships. Suppliers that fail to adapt quickly may face declining relevance as OEM procurement strategies shift toward electrified platforms.

Recycling, Environmental Compliance, and Lifecycle Management Create Additional Operational Challenges

Environmental considerations increasingly influence EV powertrain development, particularly regarding battery production, material sourcing, and end-of-life management. Governments and automotive manufacturers are introducing stricter requirements related to battery traceability, recycling rates, responsible sourcing, and lifecycle emissions. These regulations create additional compliance responsibilities for powertrain suppliers.

Battery recycling infrastructure remains an important challenge because efficient recovery systems require collection networks, specialized processing facilities, and standardized battery designs. The increasing diversity of battery chemistries and pack structures complicates recycling operations and affects recovery economics.

Automotive companies are investing in closed-loop supply chains, battery monitoring systems, and partnerships with recycling firms to address these challenges. However, commercial-scale recycling models require higher volumes of retired batteries and continued technology improvements. Suppliers must therefore balance environmental compliance requirements with cost competitiveness while maintaining reliable production operations.

Major Segment Analysis

Battery Segment: The Most Commercially Influential Component Category in the EV Powertrain Market

Among all EV powertrain components, the battery segment represents the most commercially significant category because it directly determines vehicle range, charging capability, operating cost, and overall electric vehicle performance. Battery systems account for a substantial portion of EV production costs and influence purchasing decisions across passenger vehicles, commercial fleets, and specialty transportation applications.

The demand environment for EV batteries is primarily shaped by increasing electric vehicle production volumes and the expansion of vehicle platforms designed specifically around battery-electric architectures. Automotive manufacturers are moving away from modified internal combustion platforms toward dedicated EV platforms that allow improved battery placement, enhanced vehicle packaging, and greater energy efficiency. This shift increases demand for advanced battery systems optimized for specific vehicle applications.

Passenger vehicle manufacturers typically prioritize battery characteristics such as energy density, charging speed, safety performance, lifecycle durability, and cost reduction. Premium vehicle producers often select higher-energy-density battery technologies to deliver extended driving range and performance advantages. Mass-market manufacturers generally focus on affordability, reliability, and manufacturing scalability to support broader consumer adoption.

Commercial vehicle operators evaluate batteries differently because operating economics have a greater influence on purchasing decisions. Delivery fleets, electric buses, and logistics operators require battery systems capable of supporting intensive daily usage, predictable charging cycles, and long service life. Battery degradation rates and replacement costs become important factors because fleet operators calculate total ownership expenses over extended operating periods.

Competition within the battery segment extends beyond cell manufacturing. Suppliers differentiate through battery management systems, thermal control technologies, pack design, structural integration, safety features, and recycling capabilities. Automotive manufacturers increasingly seek suppliers that can provide complete battery solutions rather than individual cells because integrated systems simplify vehicle engineering and improve production efficiency.

The geographic distribution of battery manufacturing capacity also influences competitive positioning within the EV powertrain ecosystem. Asia Pacific remains the dominant production center due to established battery supply chains, large-scale cell manufacturing facilities, and extensive experience in energy storage technologies. However, North America and Europe are expanding domestic battery production through government-supported industrial programs and partnerships between automakers and battery manufacturers.

Battery localization has become an important procurement priority because regional production reduces logistics costs, supports regulatory compliance, and improves supply chain resilience. Automotive manufacturers operating in markets with domestic content requirements increasingly evaluate suppliers based on manufacturing location, material sourcing transparency, and sustainability performance.

Technological development within the battery segment is focused on improving energy density, reducing production costs, increasing charging speed, and enhancing safety. Lithium-ion technology remains dominant, but manufacturers continue exploring alternative chemistries and cell designs to address cost, material availability, and performance requirements. Improvements in battery management software also contribute to better lifecycle performance by optimizing charging behavior and thermal conditions.

The commercial relevance of the battery segment extends beyond initial vehicle sales because battery lifecycle management creates additional business opportunities. Second-life battery applications, recycling networks, battery diagnostics, and replacement services are becoming important areas within the broader EV ecosystem. These activities can improve material recovery, reduce environmental impact, and create additional revenue streams for manufacturers and suppliers.

Over the forecast period, battery technology development, manufacturing localization, and cost reduction strategies will remain central factors influencing the EV powertrain market. Companies that combine competitive battery economics with reliable supply chains, advanced engineering capabilities, and sustainability practices are likely to strengthen their position within the expanding electric mobility value chain.

Regional Analysis

North America

North America represents an important market for EV powertrain suppliers due to expanding electric vehicle manufacturing capacity, government support for domestic supply chains, and increasing investment from global automotive manufacturers. The region’s demand environment is primarily shaped by the United States automotive sector, where passenger vehicle electrification, commercial fleet conversion, and battery manufacturing investments are influencing powertrain procurement decisions.

The United States remains the largest contributor to regional demand because major automakers are developing dedicated electric vehicle platforms and expanding production facilities for batteries and electric vehicles. Federal and state-level initiatives supporting domestic manufacturing, charging infrastructure development, and supply chain localization have encouraged companies to establish regional production capabilities. These investments create opportunities for suppliers of electric motors, power electronics, battery systems, and integrated drive units.

Buyer priorities in the United States vary between passenger vehicle manufacturers and commercial operators. Passenger vehicle OEMs emphasize cost reduction, driving range, software integration, and manufacturing scalability. Fleet operators, including logistics companies and public transportation providers, prioritize reliability, charging compatibility, and lifecycle operating costs. This difference in procurement requirements creates demand for multiple powertrain configurations rather than a single standardized solution.

Canada is strengthening its position within the EV supply chain through investments in battery materials, manufacturing facilities, and clean energy infrastructure. The country’s access to mineral resources, including lithium, nickel, and other battery-related materials, supports the development of localized battery ecosystems. However, market expansion depends on continued investment in manufacturing capacity and charging infrastructure.

Mexico has become increasingly relevant due to its established automotive manufacturing base and proximity to the United States market. Automotive suppliers are evaluating Mexico as a production location for EV components because of its manufacturing workforce, existing supplier network, and integration with North American vehicle production. Nevertheless, the transition from conventional automotive component manufacturing toward EV-specific technologies requires additional investment in technical capabilities and production equipment.

Regional constraints include infrastructure gaps outside major urban areas, higher EV production costs compared with conventional vehicles, and dependence on imported battery materials and semiconductor components. Suppliers operating in North America are therefore focusing on localized manufacturing, strategic partnerships, and flexible production models to address these challenges.

Europe

Europe remains one of the most influential regions for EV powertrain adoption due to strict vehicle emission regulations, established automotive manufacturing capabilities, and strong demand for electric passenger vehicles. The region’s regulatory environment has accelerated investment in electric vehicle platforms and encouraged manufacturers to redesign their supply chains around electrified mobility.

Germany represents the core of Europe’s automotive powertrain ecosystem due to its concentration of global vehicle manufacturers, engineering expertise, and automotive suppliers. German OEMs are investing heavily in electric platforms, battery production, software development, and manufacturing automation. This creates demand for advanced electric motors, power electronics, and integrated drivetrain systems.

The United Kingdom is developing its EV ecosystem through investments in battery manufacturing, electric vehicle production, and charging infrastructure. The country’s automotive sector is focusing on improving domestic supply capabilities while maintaining integration with European and global automotive supply networks. Battery availability and manufacturing scale remain important factors influencing long-term competitiveness.

France and Italy are also expanding electrification activities through government-supported industrial programs and OEM investments. French manufacturers are focusing on electric passenger vehicles and battery-related capabilities, while Italy’s automotive ecosystem is adapting its traditional manufacturing strengths toward electric components and specialized vehicle applications.

Spain has emerged as an important automotive production location within Europe, supported by established vehicle manufacturing facilities and investments in electrified vehicle production. Other European markets are developing EV adoption through incentives, charging infrastructure expansion, and fleet electrification programs.

The European EV powertrain market faces challenges related to energy costs, regulatory complexity, battery supply dependency, and competition from Asian manufacturing ecosystems. Suppliers must balance compliance with sustainability requirements while maintaining competitive production costs. Companies with regional manufacturing facilities, strong engineering capabilities, and established OEM relationships are better positioned to serve European demand.

Asia Pacific

Asia Pacific represents the largest manufacturing ecosystem for EV powertrain components due to extensive battery production capacity, large-scale electric vehicle deployment, and strong automotive supply chains. The region benefits from established electronics manufacturing capabilities, battery technology expertise, and significant government support for electric mobility development.

China remains the dominant contributor to regional demand and supply due to its large electric vehicle market, extensive battery manufacturing infrastructure, and integrated automotive component ecosystem. Chinese vehicle manufacturers and suppliers have developed strong capabilities across batteries, electric motors, power electronics, and vehicle control systems. Domestic EV adoption, export expansion, and manufacturing scale continue influencing regional competitive conditions.

India is becoming an important emerging market for EV powertrain suppliers due to increasing electric mobility adoption, government incentives, and growing interest from domestic and international automotive companies. Two-wheelers and commercial vehicles currently represent major electrification opportunities, while passenger vehicle adoption continues developing. Battery localization, charging infrastructure expansion, and cost optimization remain important factors influencing market development.

Japan maintains a strong position through established automotive engineering capabilities and long-term expertise in hybrid and electric vehicle technologies. Japanese manufacturers emphasize reliability, efficiency, and advanced power management systems. The country’s suppliers continue developing electric motors, power electronics, and vehicle control technologies for domestic and international markets.

South Korea plays a significant role due to its battery manufacturing capabilities and advanced automotive technology sector. Korean companies continue investing in battery technologies, electric vehicle platforms, and component manufacturing capacity to support global automotive demand.

Taiwan contributes through semiconductor manufacturing expertise, which is increasingly important for EV power electronics and control systems. Thailand and Indonesia are expanding their automotive roles through investments in electric vehicle production, battery supply chains, and regional manufacturing hubs.

The region’s competitive advantage comes from manufacturing scale, supply chain depth, and technology expertise. However, challenges include raw material dependency, price competition, and differences in regulatory frameworks across countries. Suppliers must balance cost efficiency with technological differentiation to remain competitive in this diverse market.

Middle East and Africa

The Middle East and Africa region represents an emerging opportunity for EV powertrain suppliers as governments invest in economic diversification, clean transportation initiatives, and sustainable infrastructure development. Adoption remains at an earlier stage compared with North America, Europe, and Asia Pacific, but several markets are establishing policies and investments to support electric mobility.

Saudi Arabia is developing EV-related industrial capabilities as part of broader economic diversification programs. Government investments in automotive manufacturing, renewable energy, and infrastructure development are creating opportunities for electric vehicle production and associated component supply chains. Demand is primarily influenced by government fleets, premium passenger vehicles, and future manufacturing initiatives.

The United Arab Emirates is among the leading EV adoption markets in the region due to higher consumer purchasing power, urban charging infrastructure development, and government sustainability programs. Fleet electrification, public transportation initiatives, and smart mobility projects contribute to demand for electric vehicle components.

Other Middle Eastern and African markets are gradually adopting electric vehicles, although limited charging infrastructure, higher import dependence, and affordability challenges restrict large-scale deployment. Commercial vehicles and urban transportation applications may represent early adoption opportunities because operational cost savings can justify electrification investments.

Suppliers entering these markets must consider infrastructure availability, regional service capabilities, and partnerships with local automotive stakeholders. Long-term growth depends on charging network expansion, policy support, and investment in local automotive ecosystems.

South America

South America represents a developing EV powertrain market influenced by urban mobility needs, fuel price considerations, renewable energy availability, and government sustainability initiatives. Adoption levels remain lower compared with major automotive regions due to infrastructure limitations, economic conditions, and limited local EV manufacturing capacity.

Brazil represents the largest opportunity in the region due to its automotive industry, renewable electricity generation capabilities, and growing interest in alternative powertrains. Hybrid vehicles currently have stronger market acceptance, but investments in electric vehicle infrastructure and manufacturing could support future demand for EV powertrain components.

Argentina and other South American markets are gradually exploring electric mobility through government programs, fleet initiatives, and urban transportation projects. However, high import costs, currency fluctuations, and limited charging infrastructure remain challenges affecting adoption.

Regional suppliers and international companies are evaluating South America based on long-term electrification potential rather than immediate large-scale demand. Successful market participation requires partnerships with local manufacturers, flexible supply models, and solutions adapted to regional cost conditions.

Competitive Landscape

The EV powertrain market includes established automotive suppliers, technology-focused component manufacturers, and integrated mobility solution providers competing through engineering capability, production scale, customer relationships, and technological specialization. Competition is shifting from individual component supply toward complete system integration, where suppliers combine motors, inverters, transmissions, thermal systems, and software controls into optimized electric drive solutions.

The companies included in this market analysis, including GKN Automotive, Magna International Inc., Hitachi Astemo, Ltd., Robert Bosch GmbH, BorgWarner Inc., Cummins Inc., AVL List GmbH, Mitsubishi Electric Corporation, and ZF Friedrichshafen AG compete through different technology strengths and geographic advantages.

Large automotive suppliers are expanding their EV portfolios through internal research, acquisitions, strategic collaborations, and manufacturing investments. Their competitive advantage comes from established OEM relationships, global production networks, engineering expertise, and the ability to meet automotive quality standards at scale.

Electric motor and power electronics suppliers are differentiating through efficiency improvements, compact designs, thermal management capabilities, and semiconductor integration. As automakers seek lighter and more efficient vehicles, suppliers with advanced engineering capabilities are gaining importance during vehicle development programs.

Integrated powertrain solutions are becoming a major competitive factor. OEMs increasingly prefer suppliers that can deliver complete electric drive modules because these systems reduce engineering complexity, accelerate vehicle launches, and simplify procurement management. Companies with capabilities across mechanical systems, electronics, and software have stronger opportunities to participate in future vehicle platforms.

Partnership strategies are also shaping competition. Automotive suppliers are collaborating with semiconductor companies, battery manufacturers, vehicle producers, and technology firms to strengthen EV capabilities. These partnerships allow companies to combine expertise across hardware, software, materials, and manufacturing.

Geographic expansion remains an important strategy because automotive manufacturers increasingly seek regional supply chains. Suppliers are investing in production facilities closer to vehicle assembly plants to reduce logistics costs, comply with local sourcing requirements, and improve supply reliability.

Future competitive positioning will depend on cost efficiency, technological differentiation, manufacturing flexibility, and the ability to support multiple vehicle categories. Companies that successfully integrate electric motors, power electronics, battery systems, and software capabilities will be better positioned as automotive manufacturers continue transitioning toward electrified platforms.

Recent Developments

June 2026: Hitachi Astemo announced that its electric motors and inverters were adopted for the new Nissan LEAF's 3-in-1 electric powertrain supplied through JATCO. The integrated system improves energy efficiency and driving range, reinforcing demand for compact, integrated EV powertrain architectures.

March 2026: Valeo inaugurated a new electric powertrain manufacturing line in Pune, India, dedicated to producing localized 3-in-1 e-Axle systems integrating the motor, inverter, and reducer for Mahindra's Born Electric vehicle platform.

March 2026: Valeo confirmed its Pune facility features automated manufacturing for hairpin stator assembly, inverter production, reducer assembly, and final e-Axle integration, strengthening localized EV powertrain production with full digital traceability and precision manufacturing.

February 2026: BorgWarner secured its first global 48V Electric Cross Differential (eXD) program with a Chinese OEM, expanding its electrified propulsion portfolio with advanced torque-vectoring technology for next-generation hybrid and electric vehicles.

Regulatory and Policy Environment

Government policies remain one of the most influential factors shaping investment decisions across the EV powertrain value chain. Regulations are no longer limited to vehicle emissions; they increasingly encompass battery production, supply chain localization, recycling, cybersecurity, software updates, and lifecycle sustainability. As a result, powertrain suppliers must address a broader compliance framework while maintaining competitive manufacturing costs and technological performance.

Vehicle emission standards continue to encourage automotive manufacturers to accelerate electrification. Regulatory authorities in North America, Europe, China, Japan, South Korea, and several emerging economies have introduced progressively stricter fleet-average emission requirements that encourage greater adoption of battery electric and hybrid vehicles. Compliance with these regulations requires automakers to expand their electric vehicle portfolios, creating sustained demand for batteries, electric motors, power electronics, and integrated drive units.

Battery regulations have become increasingly comprehensive. Policymakers are introducing requirements covering battery traceability, responsible sourcing of critical minerals, carbon footprint reporting, recycled material content, and end-of-life recycling. These measures encourage greater transparency throughout the battery supply chain while supporting circular economy objectives. Suppliers capable of documenting material origins and demonstrating responsible production practices are likely to gain stronger positions during OEM procurement processes.

Governments are also supporting domestic manufacturing through industrial incentive programs. Financial assistance for battery plants, semiconductor manufacturing, EV component production, and research facilities is encouraging greater localization of powertrain supply chains. These programs reduce dependence on imported components, improve supply security, and strengthen regional automotive competitiveness.

Charging infrastructure policies complement vehicle electrification strategies. Public investment in fast-charging networks, commercial fleet charging facilities, and electricity grid modernization supports wider EV adoption. Greater charging availability improves consumer confidence while encouraging fleet operators to accelerate vehicle replacement decisions, indirectly increasing demand for advanced EV powertrain systems.

Safety regulations remain central to powertrain development. Battery packs, high-voltage electrical systems, functional safety software, thermal management systems, and charging interfaces must comply with internationally recognized automotive safety standards before commercial deployment. Manufacturers therefore invest extensively in testing, validation, and certification activities throughout product development.

Cybersecurity requirements are becoming increasingly relevant as software-defined vehicles gain broader adoption. Electric powertrains rely on electronic control units, battery management systems, and connected software platforms that require secure communication and protection against unauthorized access. Compliance with automotive cybersecurity and software update regulations has therefore become an essential element of product development.

International standardization efforts also influence supplier competitiveness. Harmonized charging protocols, communication standards, battery safety specifications, and electrical interface requirements simplify vehicle interoperability across different markets while reducing engineering complexity for global manufacturers.

Overall, the regulatory environment increasingly favors suppliers that combine technological innovation with compliance expertise, localized manufacturing capabilities, sustainable production practices, and transparent supply chain management.

Outlook and Strategic Implications

The EV powertrain market is expected to remain one of the automotive industry's highest-priority investment areas through the forecast period as manufacturers continue transitioning from internal combustion platforms toward dedicated electric vehicle architectures. Future growth will be determined less by the pace of initial electrification announcements and more by manufacturers' ability to deliver affordable, efficient, and scalable electric propulsion systems.

Investment priorities are shifting toward vertically integrated production models that combine battery manufacturing, electric motor assembly, power electronics, software development, and final vehicle production. Automotive manufacturers increasingly seek greater control over critical technologies to improve cost management, reduce supply risks, and accelerate product development. At the same time, strategic partnerships will remain important for semiconductor technologies, advanced battery materials, and specialized engineering capabilities.

Procurement strategies are becoming more sophisticated. OEMs are expected to evaluate suppliers based on long-term manufacturing capacity, engineering support, software integration capability, sustainability performance, and financial stability in addition to traditional cost considerations. Suppliers capable of delivering complete electric drive systems rather than individual components are likely to strengthen their commercial position because integrated solutions simplify vehicle development and manufacturing.

Technology development will increasingly emphasize efficiency improvements rather than simply increasing battery capacity. Higher-efficiency electric motors, silicon carbide power electronics, intelligent battery management systems, advanced thermal management, and software-controlled energy optimization will become important competitive differentiators. These technologies can improve driving range and charging performance without proportionally increasing battery size or vehicle weight.

Commercial vehicle electrification is expected to generate additional opportunities for specialized powertrain suppliers. Fleet operators continue focusing on operational efficiency, predictable maintenance costs, and lifecycle economics. Suppliers capable of supporting heavy-duty applications with durable, high-performance electric propulsion systems and integrated service capabilities will benefit from expanding fleet electrification programs.

Manufacturing localization will remain a strategic priority across major automotive regions. Governments are encouraging domestic production through industrial incentives and local content requirements, while OEMs seek greater supply chain resilience following recent disruptions. Suppliers with geographically diversified manufacturing networks will be better positioned to support regional production programs and reduce logistics risks.

Several risks continue to influence market development. Volatility in battery raw material prices, semiconductor supply constraints, charging infrastructure deployment rates, evolving trade policies, and differences in regional regulatory frameworks may affect investment decisions and production planning. Economic conditions and consumer purchasing power will also influence the pace of EV adoption, particularly in emerging markets.

Competitive dynamics are expected to evolve toward platform-based collaboration rather than isolated component competition. Suppliers with expertise spanning mechanical engineering, electrical systems, software development, and advanced manufacturing are likely to achieve stronger long-term relationships with automotive manufacturers. Success will increasingly depend on delivering integrated propulsion solutions that improve vehicle efficiency, reduce production complexity, and support global manufacturing strategies.

The EV powertrain market is expected to transition from a phase centered on capacity expansion toward one focused on manufacturing efficiency, software-defined functionality, localized production, and lifecycle sustainability. Companies that balance technological innovation with cost competitiveness, supply chain resilience, and regulatory compliance will be best positioned to capture future procurement opportunities across passenger and commercial electric vehicle markets.

EV Powertrain Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 43.4 billion |

| Total Market Size in 2031 | USD 82.6 billion |

| Forecast Unit | Billion |

| Growth Rate | 13.7% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Component, Propulsion Type, Vehicle Type, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Component

- Battery

- Electric Motor

- Transmission

- Power Electronics

By Propulsion Type

- Battery Electric Vehicle (BEV)

- Plug-in Hybrid Electric Vehicle (PHEV)

- Hybrid Electric Vehicle (HEV)

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Others

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Others

- Asia Pacific

- China

- India

- Japan

- South Korea

- Taiwan

- Thailand

- Indonesia

- Others

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

1.8. Key Benefits for Stakeholders

2. RESEARCH METHODOLOGY

2.1. Research Design

2.2. Research Process

3. EXECUTIVE SUMMARY

3.1. Key Findings

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Porter’s Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of New Entrants

4.3.4. Threat of Substitutes

4.3.5. Competitive Rivalry in the Industry

4.4. Industry Value Chain Analysis

4.5. Analyst View

5. EV POWERTRAIN MARKET BY COMPONENT

5.1. Introduction

5.2. Battery

5.3. Electric Motor

5.4. Transmission

5.5. Power Electronics

6. EV POWERTRAIN MARKET BY PROPULSION TYPE

6.1. Introduction

6.2. Battery Electric Vehicle (BEV)

6.3. Plug-in Hybrid Electric Vehicle (PHEV)

6.4. Hybrid Electric Vehicle (HEV)

7. EV POWERTRAIN MARKET BY VEHICLE TYPE

7.1. Introduction

7.2. Passenger Cars

7.3. Commercial Vehicles

8. EV POWERTRAIN MARKET BY GEOGRAPHY

8.1. Introduction

8.2. North America

8.2.1. By Component

8.2.2. By Propulsion Type

8.2.3. By Vehicle Type

8.2.4. By Country

8.2.4.1. United States

8.2.4.2. Canada

8.2.4.3. Mexico

8.3. South America

8.3.1. By Component

8.3.2. By Propulsion Type

8.3.3. By Vehicle Type

8.3.4. By Country

8.3.4.1. Brazil

8.3.4.2. Argentina

8.3.4.3. Others

8.4. Europe

8.4.1. By Component

8.4.2. By Propulsion Type

8.4.3. By Vehicle Type

8.4.4. By Country

8.4.4.1. United Kingdom

8.4.4.2. Germany

8.4.4.3. France

8.4.4.4. Italy

8.4.4.5. Spain

8.4.4.6. Others

8.5. Middle East and Africa

8.5.1. By Component

8.5.2. By Propulsion Type

8.5.3. By Vehicle Type

8.5.4. By Country

8.5.4.1. Saudi Arabia

8.5.4.2. United Arab Emirates

8.5.4.3. Others

8.6. Asia Pacific

8.6.1. By Component

8.6.2. By Propulsion Type

8.6.3. By Vehicle Type

8.6.4. By Country

8.6.4.1. China

8.6.4.2. India

8.6.4.3. Japan

8.6.4.4. South Korea

8.6.4.5. Taiwan

8.6.4.6. Thailand

8.6.4.7. Indonesia

8.6.4.8. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Competitive Dashboard

10. COMPANY PROFILES

10.1. GKN Automotive (Dowlais Group plc)

10.2. Magna International Inc.

10.3. Hitachi Astemo, Ltd.

10.4. Robert Bosch GmbH

10.5. BorgWarner Inc.

10.6. Cummins Inc.

10.7. AVL List GmbH

10.8. Mitsubishi Electric Corporation

10.9. ZF Friedrichshafen AG

Navigate

Trusted by the world's leading organizations