Report Overview

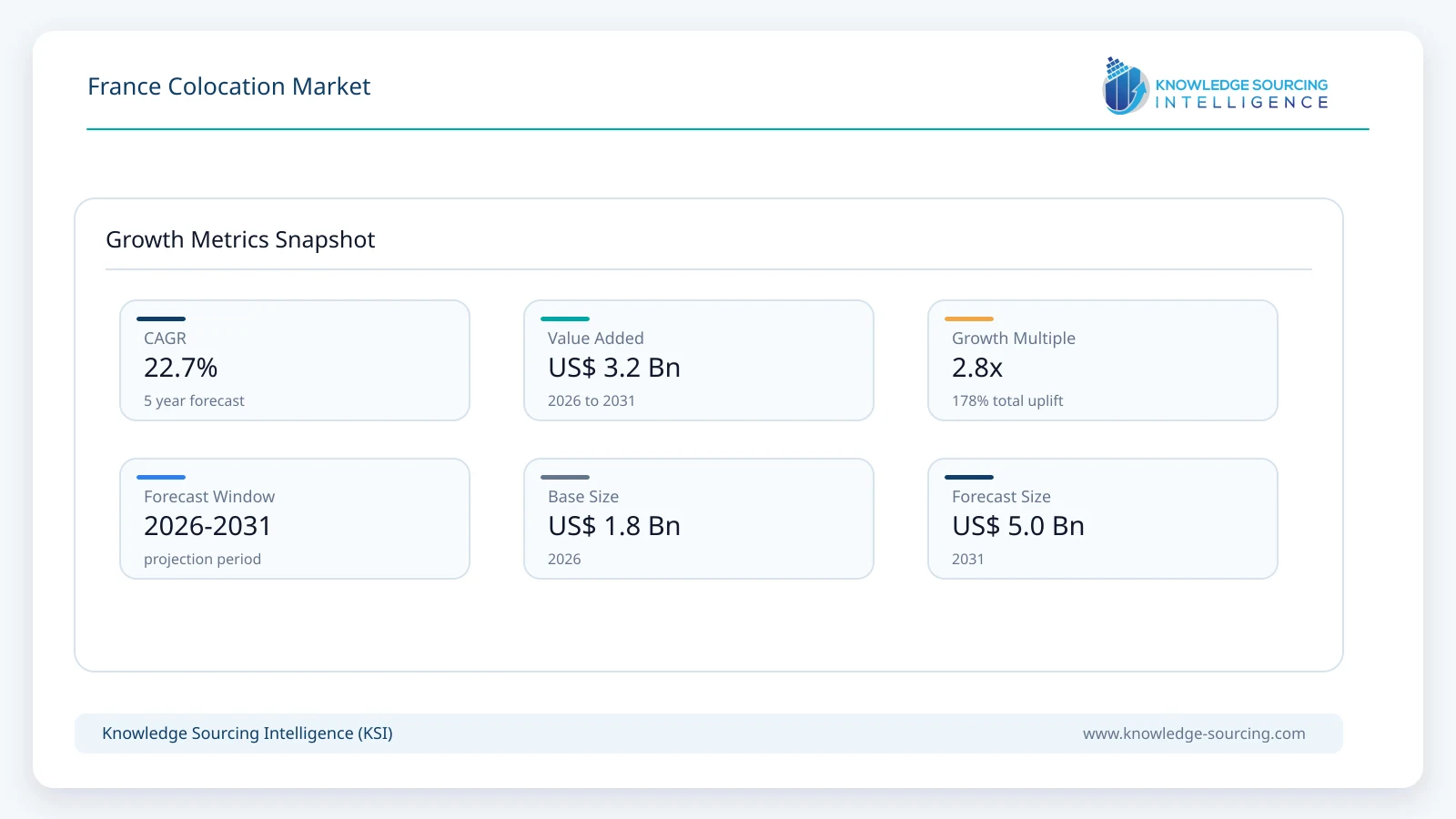

The French colocation market will grow at a CAGR of 22.7% from USD 1.8 billion in 2026 to USD 5.0 billion in 2031.

Highlights:

- 1Largest End-User (Cloud Service Providers)Hyperscale cloud providers represent the most significant source of wholesale demand, as they lease massive capacities to support the rapid expansion of localized cloud zones in the Île-de-France region.

- 2Regulatory Impact (Energy Efficiency Directive)The implementation of mandatory reporting for facilities above 500kW IT load under the EED is forcing older data centers to undergo expensive retrofitting or risk obsolescence.

- 3Regional Leader (Paris/Île-de-France)While regional hubs are growing, the Paris region remains the dominant market due to its concentration of subsea cable landings and proximity to the national financial and administrative core.

- 4Technology Transition (Liquid Cooling)The rise of AI workloads is driving a mandatory shift toward direct-to-chip and immersion cooling technologies, as traditional air-based systems cannot manage the thermal output of high-density racks.

The French colocation market is undergoing a profound structural evolution characterized by the transition from general-purpose data storage to high-density compute environments. Structural demand is no longer merely a byproduct of general internet traffic growth; instead, it is being fundamentally reshaped by the rapid adoption of generative AI and the French government’s “Digital Sovereignty Strategy.” This policy framework incentivizes the localization of data within national borders, creating a sustained requirement for secure, high-tier colocation facilities. As enterprises migrate away from legacy on-premises server rooms to reduce operational complexity, colocation providers have become the primary facilitators of this industrial-scale digital migration.

Industry dependency on colocation is deepening as the complexity of power and thermal management exceeds the capabilities of standard enterprise real estate. The evolution of processing technologies, specifically the deployment of GPU-intensive clusters for machine learning, has forced a shift in facility design toward modular, scalable architectures. Simultaneously, the market is navigating a mandatory sustainability transition. Compliance with the REEN Act and the EED is no longer optional, making energy efficiency a core competitive differentiator. Strategically, colocation has moved from being a utility-grade service to a central pillar of France’s national infrastructure, essential for supporting everything from financial high-frequency trading to the burgeoning quantum computing sector.

Market Dynamics

Market Drivers

AI-Driven Power Density Requirements: The deployment of large language models (LLMs) requires power densities often exceeding 30kW per rack. This drives demand for specialized colocation facilities capable of providing advanced electrical distribution and liquid cooling that standard enterprise offices cannot support.

National Digital Sovereignty Mandates: Government initiatives aimed at protecting sensitive data and reducing dependence on non-European infrastructure directly increase the demand for local colocation, as French organizations are increasingly required to host critical workloads within domestic, Tier 3 or Tier 4 certified facilities.

5G and Edge Computing Densification: The rollout of 5G across major French metropolitan areas necessitates low-latency processing closer to the end-user. This drives demand for smaller, distributed colocation "edge" sites in cities like Lyon, Lille, and Toulouse to handle real-time IoT and mobile data.

Sustainability-Linked Tax Incentives: To benefit from a reduced TICFE (electricity consumption tax), operators must adhere to ISO 50001 standards. This regulatory incentive encourages enterprises to move from inefficient in-house setups to professional colocation providers who can demonstrate superior Power Usage Effectiveness (PUE).

Market Restraints and Opportunities

Grid Capacity and Urban Zoning Constraints: In high-demand areas like Paris, securing new high-voltage power connections is becoming increasingly difficult. This supply-side constraint limits the speed of new facility construction and increases the cost of remaining available capacity.

Rising Operational Costs (OPEX): Fluctuating energy prices and the specialized labor required to manage high-density AI infrastructure are tightening margins. However, this also presents an opportunity for providers who can integrate on-site renewable energy or waste heat recovery to lower long-term costs.

Opportunity in Waste Heat Recovery: New regulations require facilities over 1MW to explore heat reuse. This creates a strategic opportunity for colocation operators to partner with municipalities for district heating, turning a regulatory burden into a community-integrated revenue or cost-offset model.

Emerging Demand from Quantum Computing: As France aims to be a leader in quantum technology, the specialized environmental and security needs of quantum processors provide a high-value niche opportunity for colocation providers willing to invest in ultra-secure, specialized shielded environments.

Supply Chain Analysis

The supply chain for the France colocation market is characterized by high energy intensity and a growing reliance on specialized mechanical and electrical equipment. Production concentration is high among a few global vendors for critical components like Uninterruptible Power Supply (UPS) units and high-density cooling systems. Transportation constraints for large-scale generators and transformers can lead to project delays, especially as global demand for data center hardware continues to outpace manufacturing capacity.

Integrated manufacturing strategies are increasingly common, with operators like Equinix and Digital Realty working closely with vendors to develop modular, pre-fabricated data center components to bypass local construction bottlenecks. Regional risk exposure is primarily centered on energy availability; the French grid’s reliance on nuclear power provides a stable, low-carbon base, but localized bottlenecks in the Paris North region (Saint-Denis) have forced developers to seek "shovel-ready" sites in secondary markets.

Government Regulations

Jurisdiction | Key Regulation / Agency | Market Impact Analysis |

Europe | Energy Efficiency Directive (EED) | Mandates annual public reporting of PUE, water usage, and waste heat recovery for all facilities ?500kW, driving efficiency retrofits. |

France | REEN Act / ARCEP | Empowers the regulator to collect environmental data from operators; non-compliance with environmental reporting can lead to fines and public disclosure. |

France | ICPE (Installations Classified for Environmental Protection) | Requires strict permitting for diesel generators and cooling systems, often dictating the physical design and location of new data centers. |

Global | GDPR | Ensures a baseline requirement for high-security, localized data hosting, particularly for the healthcare and finance sectors. |

Key Developments

June 2026: Telehouse France and Cirrascale Cloud Services announced a strategic partnership to deploy AI inference capabilities directly within Telehouse France colocation data centers, enabling enterprises to run AI workloads closer to their data with lower latency and enhanced data sovereignty.

May 2026: Telehouse France launched a new high-density AI module at its TH3 Paris Magny campus, expanding colocation infrastructure designed for GPU-intensive AI workloads while strengthening sovereign, high-performance digital infrastructure in France.

August 2025: Equinix – Signed a pre-order agreement for 500 MWe with Stellaria (incubated by Schneider-Electric and the French Atomic Energy Agency) for molten salt nuclear reactors. This marks a structural shift toward securing long-term, independent, low-carbon power for European data centers.

Market Segmentation

By Type: Wholesale Colocation

Wholesale colocation is the fastest-growing segment in the French market, primarily driven by the expansion of US-based hyperscale cloud providers and large-scale AI research initiatives. These clients require massive blocks of power (often multi-megawatt) and significant floor space to house their proprietary hardware. The demand in this segment is less sensitive to per-rack pricing and more focused on the long-term availability of power and the provider’s ability to support liquid cooling at scale. Wholesale contracts in France are typically long-term (5–10 years), providing operators with the capital stability needed to fund further expansions.

By Industry Vertical: BFSI (Banking, Financial Services, and Insurance)

The BFSI sector remains a cornerstone of the French retail and hybrid colocation market. Demand is driven by the necessity for ultra-low latency connections to the Paris Stock Exchange and other European trading hubs. For these institutions, colocation provides a level of physical security and redundancy (Tier 4) that is cost-prohibitive to build and maintain in-house. Furthermore, the shift toward "Open Banking" and real-time transaction processing requires financial firms to host their infrastructure in carrier-neutral facilities that offer direct, private "on-ramps" to multiple cloud providers.

By Enterprise Size: Large Enterprises

Large enterprises are the primary adopters of hybrid colocation models. These organizations typically maintain a mix of legacy systems that cannot be moved to the public cloud and modern, cloud-native applications. Colocation provides the operational advantage of a unified environment where they can colocate their private servers alongside cloud interconnection points. This reduces the cost of data egress and improves the performance of mission-critical applications by keeping the data close to the compute resources.

List of Companies

Orange S.A.

Digital Realty

Equinix, Inc.

Data4 Group

Telehouse

OVHcloud

Colt Technology Services Group Limited

Exa Infrastructure

Orange S.A.

Orange S.A. maintains a unique position in the French market due to its dual role as a national telecommunications incumbent and a major data center operator. Its strategy, recently updated in the "Trust the Future" 2026–2030 roadmap, focuses on leveraging its extensive fiber-optic infrastructure to provide high-performance connectivity to its colocation sites. Unlike some competitors, Orange has retained control over much of its physical infrastructure, allowing it to offer highly integrated wholesale and retail solutions. Its competitive advantage lies in its deep penetration across all French regions, enabling it to support edge computing deployments that global players find difficult to reach.

Equinix, Inc.

Equinix is a global leader in the colocation space with a heavy focus on interconnection and "Private AI" infrastructure. In France, the company has strategically expanded its "xScale" portfolio to meet hyperscale demand while maintaining a dominant position in the retail market through its IBX data centers. Equinix’s strategy is increasingly defined by energy innovation, as seen in its recent agreements for Small Modular Reactors (SMRs) and its commitment to 100% renewable energy. Its technology differentiation lies in its "Equinix Fabric," which allows customers to dynamically connect to thousands of other businesses and cloud providers globally.

Digital Realty

Digital Realty operates one of the largest data center footprints in France, particularly through its Paris Digital Park. Its market position is centered on providing massive scale and flexibility, catering to both retail enterprises and the world's largest cloud service providers. The company’s strategy emphasizes sustainable "design-at-scale," utilizing advanced cooling and energy management systems to minimize environmental impact. Digital Realty’s competitive strength in France is its ability to offer high-connectivity campuses that provide customers with a clear path for growth from a single rack to a multi-megawatt private suite.

Analyst View

The French colocation market is transitioning toward a high-density, AI-ready infrastructure model. Growth is structurally underpinned by digital sovereignty mandates and cloud expansion, while sustainability regulations present both a modernization challenge and a strategic opportunity for regional decentralization.

France Colocation Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 1.8 billion |

| Total Market Size in 2031 | USD 5.0 billion |

| Forecast Unit | Billion |

| Growth Rate | 22.7% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Type, Enterprise Size, Industry Vertical |

| Companies |

|

Market Segmentation

By Type

- Retail Colocation

- Wholesale Colocation

- Hybrid Colocation

By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

By Industry Vertical

- BFSI

- IT & Telecom

- Government

- Healthcare

- Manufacturing

- Retail & E-commerce

- Media & Entertainment

- Education

- Others

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

1.8. Key Benefits to the Stakeholders

2. RESEARCH METHODOLOGY

2.1. Research Design

2.2. Research Processes

3. EXECUTIVE SUMMARY

3.1. Key Findings

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Porter’s Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of New Entrants

4.3.4. Threat of Substitutes

4.3.5. Competitive Rivalry in the Industry

4.4. Industry Value Chain Analysis

4.5. Analyst View

5. FRANCE COLOCATION MARKET BY TYPE

5.1. Introduction

5.2. Retail Colocation

5.2.1. Market Trends and Opportunities

5.2.2. Growth Prospects

5.3. Wholesale Colocation

5.3.1. Market Trends and Opportunities

5.3.2. Growth Prospects

5.4. Hybrid Colocation

5.4.1. Market Trends and Opportunities

5.4.2. Growth Prospects

6. FRANCE COLOCATION MARKET BY ENTERPRISE SIZE

6.1. Introduction

6.2. Small and Medium Enterprises (SMEs)

6.2.1. Market Trends and Opportunities

6.2.2. Growth Prospects

6.3. Large Enterprises

6.3.1. Market Trends and Opportunities

6.3.2. Growth Prospects

7. FRANCE COLOCATION MARKET BY INDUSTRY VERTICAL

7.1. Introduction

7.2. BFSI

7.2.1. Market Trends and Opportunities

7.2.2. Growth Prospects

7.3. IT & Telecom

7.3.1. Market Trends and Opportunities

7.3.2. Growth Prospects

7.4. Government

7.4.1. Market Trends and Opportunities

7.4.2. Growth Prospects

7.5. Healthcare

7.5.1. Market Trends and Opportunities

7.5.2. Growth Prospects

7.6. Manufacturing

7.6.1. Market Trends and Opportunities

7.6.2. Growth Prospects

7.7. Retail & E-commerce

7.7.1. Market Trends and Opportunities

7.7.2. Growth Prospects

7.8. Media & Entertainment

7.8.1. Market Trends and Opportunities

7.8.2. Growth Prospects

7.9. Education

7.9.1. Market Trends and Opportunities

7.9.2. Growth Prospects

7.10. Others

7.10.1. Market Trends and Opportunities

7.10.2. Growth Prospects

8. COMPETITIVE ENVIRONMENT AND ANALYSIS

8.1. Major Players and Strategy Analysis

8.2. Market Share Analysis

8.3. Mergers, Acquisitions, Agreements, and Collaborations

8.4. Competitive Dashboard

9. COMPANY PROFILES

9.1. Orange S.A.

9.2. Digital Realty

9.3. Equinix, Inc.

9.4. Data4 Group

9.5. Telehouse

9.6. OVHcloud

9.7. Colt Technology Services Group Limited

9.8. Exa Infrastructure

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations