Report Overview

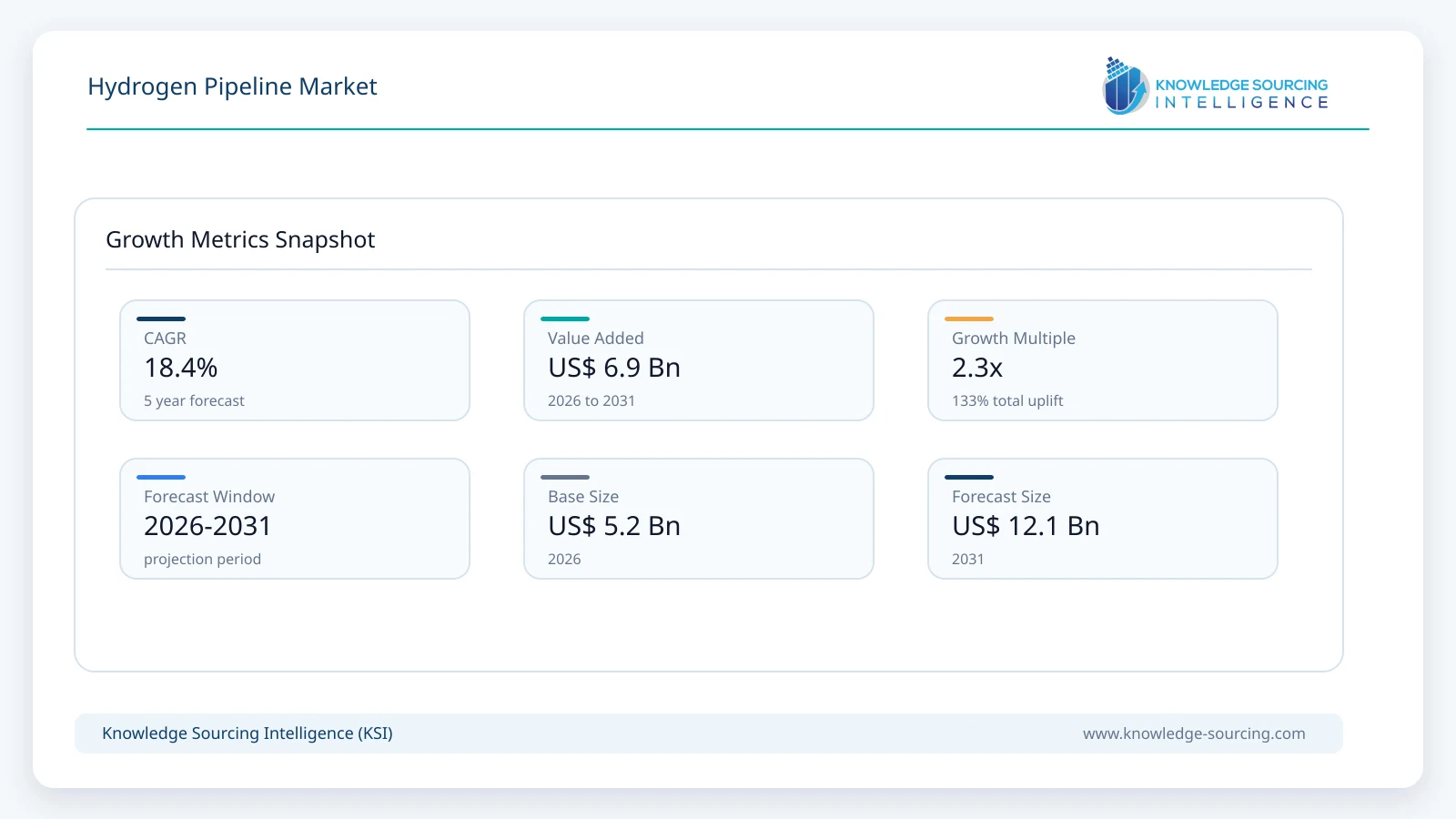

The Hydrogen Pipeline Market is forecast to grow at a CAGR of 18.4%, reaching USD 12.10 billion in 2031 from USD 5.20 billion in 2026.

Highlights:

- 1Hydrogen pipeline investment increasingly aligns with industrial decarbonization, cross-border energy trade, and hydrogen hub development.

- 2Repurposing existing natural gas pipelines is improving project economics and reducing deployment timelines.

- 3Europe remains the most active region for cross-border hydrogen transmission planning and regulatory coordination.

- 4Steel pipelines continue to serve high-pressure industrial applications, while polymer pipelines gain traction in distribution networks.

- 5Project execution increasingly depends on long-term hydrogen offtake agreements, permitting certainty, and infrastructure financing.

Unlike conventional industrial gas networks that primarily serve localized demand, hydrogen transmission infrastructure is increasingly being designed to support large-scale movement of low-emission hydrogen across industrial clusters and national borders. Demand for dedicated hydrogen transport is expanding alongside investments in renewable hydrogen production, carbon capture-enabled hydrogen projects, and industrial decarbonization programmes targeting steel, refining, chemicals, fertilizer, and heavy manufacturing. The commercial value of pipeline infrastructure therefore extends beyond transportation, influencing project bankability, supply reliability, and regional market integration.

Current buyer activity reflects a gradual transition from isolated industrial pipeline systems toward integrated regional transmission networks. Infrastructure developers, transmission system operators, industrial gas companies, and governments increasingly favour pipeline solutions where hydrogen volumes justify continuous transport and long operating lives. The International Energy Agency notes that approximately 5,000 km of hydrogen pipelines are already operating globally, largely serving established industrial users. Announced projects, including both new construction and repurposed natural gas assets, exceed 40,000 km through 2035, although only a limited proportion has progressed to committed investment or construction, highlighting the industry's execution gap between announced capacity and commercial deployment.

Purchasing decisions increasingly prioritise lifecycle transport cost, compatibility with hydrogen purity requirements, operating pressure, material integrity, future expansion capability, and regulatory compliance. Industrial buyers generally favour long-term transport agreements that reduce supply uncertainty, while pipeline developers seek anchor customers capable of supporting high utilisation rates before committing capital expenditure. Consequently, commercial success increasingly depends on coordinated development between hydrogen production, storage, transmission, and end-use facilities rather than investment in individual assets alone.

Key Market Indicators

Indicator | Latest Evidence | Commercial Meaning |

Operational hydrogen pipelines worldwide | Approximately 5,000 km | Demonstrates an established industrial operating base for hydrogen transmission. |

Announced hydrogen pipeline projects to 2035 | More than 40,000 km | Indicates an expanding long-term infrastructure pipeline supporting future hydrogen trade. |

Operational or committed share of announced pipeline projects | About 9% | Shows that financing, permitting, and customer commitments remain major execution barriers. |

Global hydrogen demand (2025) | Over 100 Mt | Industrial demand continues to provide the primary foundation for pipeline utilisation. |

Low-emissions hydrogen production growth (2025) | Around 20% year-on-year | Supports gradual expansion of dedicated hydrogen transport infrastructure. |

Sources: International Energy Agency, Global Hydrogen Review 2026.

Market Drivers

Expansion of industrial decarbonisation programmes requiring continuous hydrogen supply.

Steel manufacturing, petroleum refining, fertiliser production, chemicals, and other energy-intensive industries are increasing investment in low-emission hydrogen as governments tighten emissions standards and companies pursue net-zero commitments. These applications require dependable, high-volume hydrogen delivery that trucking cannot economically provide over sustained periods. Pipeline operators are therefore planning dedicated transmission corridors connecting production facilities with industrial clusters. Equipment suppliers are responding by developing pipeline systems designed for higher hydrogen purity, material durability, and long-term operational reliability, particularly for heavy industrial users.

Repurposing natural gas infrastructure improves project economics.

Existing gas transmission networks provide a commercially attractive starting point for hydrogen transport because many corridors, compressor stations, and rights-of-way already exist. The International Energy Agency reports growing investment in repurposed pipelines, particularly across Europe, where Germany completed one of the world's largest natural gas pipeline conversions for hydrogen service while additional cross-border projects continue to advance. Repurposing generally lowers construction costs, shortens permitting schedules, and reduces environmental impacts compared with entirely new pipeline development, improving project viability where technical conditions allow.

Government-backed hydrogen corridors and regional infrastructure planning accelerate investment decisions.

National hydrogen strategies increasingly extend beyond production incentives to include transmission infrastructure. European transmission operators continue developing interconnected hydrogen backbone networks linking industrial demand centres with import terminals and renewable hydrogen production regions. Similar planning initiatives are emerging across China and selected Middle Eastern markets to support domestic hydrogen production and export ambitions. These coordinated infrastructure programmes reduce investment uncertainty by aligning pipeline construction with production projects, storage facilities, and anticipated industrial demand, encouraging equipment manufacturers and pipeline developers to expand engineering capabilities and manufacturing capacity.

Market Restraints and Challenges

Hydrogen material compatibility increases engineering complexity and project costs.

Hydrogen molecules can penetrate certain metallic materials, causing hydrogen embrittlement that reduces ductility and increases the risk of cracking under high-pressure operation. This issue does not affect all pipeline materials equally, but it requires rigorous material selection, testing, welding procedures, and inspection before new construction or pipeline conversion proceeds. Companies such as Tenaris, Nippon Steel Corporation, and Cenergy Holdings continue to invest in pipeline grades, coatings, and manufacturing processes suitable for hydrogen service, reflecting the industry's emphasis on long-term asset integrity rather than simple adaptation of conventional gas infrastructure. These requirements increase project costs and extend engineering schedules, particularly for high-pressure transmission systems. According to the International Organization for Standardization (ISO) and industry standards under development, material qualification remains one of the most important technical considerations for hydrogen infrastructure expansion.

Project economics remain closely tied to coordinated infrastructure development.

Pipeline investment depends on sustained hydrogen throughput over several decades, making commercial viability difficult when production facilities, storage sites, and industrial demand centres develop at different speeds. The International Energy Agency notes that although announced hydrogen pipeline projects exceed 40,000 km globally, only a limited proportion has reached final investment commitment or entered operation. Developers increasingly require long-term transport agreements before construction begins, while hydrogen producers often delay capacity expansion until transmission infrastructure is available. This sequencing challenge slows project execution and raises financing risk, particularly for greenfield hydrogen corridors where customer demand has yet to mature. Public funding programmes and regulated infrastructure models are helping reduce uncertainty in some regions, although commercial alignment remains a structural industry challenge.

Permitting, regulatory alignment, and technical standards continue to evolve across jurisdictions.

Unlike conventional natural gas infrastructure, hydrogen pipeline projects frequently require new safety assessments, updated design standards, environmental reviews, and regulatory approval processes tailored to hydrogen transport. Requirements differ across jurisdictions, particularly for pipeline conversion, operating pressure, hydrogen blending limits, and material certification. Europe has made notable progress through coordinated hydrogen market legislation and cross-border infrastructure planning, yet regulatory consistency remains under development in many other markets. Manufacturers and engineering contractors therefore face varying compliance obligations across countries, increasing project preparation time and engineering costs while limiting opportunities for standardised infrastructure deployment.

Major Segment Analysis

New Pipelines

New hydrogen pipelines represent the most commercially important installation segment because they enable transmission networks specifically designed for pure hydrogen transport rather than adapting infrastructure originally intended for natural gas. Dedicated systems allow operators to optimise pipe diameter, wall thickness, compressor configuration, operating pressure, and material selection according to hydrogen service requirements, reducing operational constraints associated with legacy assets. Demand is strongest where governments are establishing hydrogen production hubs, export corridors, and industrial decarbonisation clusters that require large-volume, long-distance transport.

Buyers in this segment typically include transmission system operators, industrial gas companies, integrated energy companies, and public infrastructure developers. Procurement decisions extend beyond pipeline cost to include lifecycle reliability, inspection capability, future network expansion, and compliance with evolving hydrogen safety standards. Suppliers compete by offering specialised steel grades, corrosion-resistant coatings, welding technologies, and engineering expertise that address hydrogen compatibility requirements. Although repurposed natural gas pipelines remain attractive where technically feasible, dedicated hydrogen pipelines continue to receive investment in projects requiring higher operating pressures, greater purity assurance, or infrastructure designed for long-term network expansion. Performance within this segment will strongly influence the commercial scalability of regional hydrogen economies over the forecast period.

Regional Analysis

Region | Main Demand Signal | Principal Constraint |

North America | Industrial decarbonisation and regional hydrogen hub investments | High capital requirements and permitting timelines |

Europe | Cross-border hydrogen backbone development and decarbonisation policy | Complex regulatory coordination across multiple jurisdictions |

Asia Pacific | Manufacturing expansion, hydrogen production capacity, and government strategies | Uneven infrastructure maturity across countries |

Middle East and Africa | Export-oriented hydrogen projects and industrial diversification | Domestic demand remains comparatively limited in several markets |

North America continues to expand hydrogen pipeline opportunities through industrial decarbonisation programmes and government-backed hydrogen hubs. The United States has accelerated investment following federal incentives supporting clean hydrogen production and regional hydrogen hub development. Existing hydrogen pipeline infrastructure along the U.S. Gulf Coast provides an operational foundation for future network expansion serving refining, petrochemical, and chemical industries. Canada is advancing hydrogen infrastructure through provincial initiatives and export-oriented projects, while Mexico's market remains closely linked to industrial demand and cross-border energy integration.

European demand is shaped by policy coordination as much as industrial consumption. The European Hydrogen Backbone initiative, together with projects supported under the European Union's Trans-European Networks for Energy framework, is encouraging development of interconnected transmission systems across multiple countries. Germany, the Netherlands, France, Spain, and the United Kingdom are investing in hydrogen transport to connect renewable production, industrial clusters, storage facilities, and import terminals. Repurposing existing natural gas pipelines remains an important commercial strategy because it reduces construction costs and accelerates deployment where technical conditions permit.

Asia Pacific presents diverse market conditions driven by industrial production, government policy, and domestic energy strategies. China continues investing in renewable hydrogen production and associated transmission infrastructure to support industrial decarbonisation. Japan and South Korea prioritise hydrogen within long-term energy transition plans, while India is progressing infrastructure development under the National Green Hydrogen Mission. Although infrastructure maturity differs considerably across the region, expanding manufacturing capacity, steel production, refining activity, and fertiliser demand continue to create long-term requirements for dedicated hydrogen transportation networks.

The Middle East and Africa are increasingly positioning hydrogen pipeline infrastructure around export-oriented production and industrial diversification. Saudi Arabia and the United Arab Emirates continue developing large-scale hydrogen and ammonia projects intended to serve international markets alongside domestic industrial demand. Pipeline development increasingly supports integrated energy complexes that combine renewable generation, hydrogen production, storage, and export facilities. However, domestic hydrogen consumption remains at an earlier stage across many countries, making infrastructure investment highly dependent on export contracts and long-term international offtake agreements.

Competitive Landscape

Competition in the hydrogen pipeline market is technology-led and project-driven rather than volume-driven, as suppliers compete on engineering capability, material performance, compliance with hydrogen service standards, and execution experience. Pipeline manufacturers, steel producers, polymer pipe suppliers, and engineering companies increasingly align their portfolios with dedicated hydrogen transport and natural gas pipeline conversion projects. Long qualification cycles, strict safety requirements, and customer preference for proven infrastructure create meaningful barriers to entry, particularly for high-pressure transmission applications.

Cenergy Holdings (Corinth Pipeworks), Tenaris, EUROPIPE GmbH, Mannesmann Line Pipe GmbH, Welspun Corp., and Nippon Steel Corporation compete through specialised steel pipe manufacturing, hydrogen-compatible materials, and large-diameter transmission capabilities. GF Piping Systems, Pipelife International GmbH, and SoluForce B.V. strengthen competition in distribution networks by supplying polyethylene and composite pipeline systems suited to lower-pressure applications. Siemens Energy complements pipeline infrastructure through compression, monitoring, and system integration technologies that support hydrogen transmission projects. Across the market, suppliers are expanding engineering services, investing in material testing, and forming partnerships with utilities, transmission operators, and hydrogen project developers to address evolving customer specifications and reduce project execution risk.

Recent Developments

July 2026 – Friedrich Vorwerk secured a contract to build a hydrogen pipeline in Germany. The project expands Germany's hydrogen core network, supporting industrial decarbonisation by constructing dedicated hydrogen transport infrastructure connecting production, storage and major demand centres across the country.

May 2025 – PetroChina won the contract to construct a 190-kilometre dedicated hydrogen pipeline in China. The project strengthens China's hydrogen transportation infrastructure, enabling reliable hydrogen delivery to industrial clusters while accelerating development of the country's large-scale hydrogen economy.

March 2025 – Fluxys began construction of Belgium's first hydrogen pipeline network. Initial development connects the Port of Antwerp with the Port of Ghent, establishing the foundation for Belgium's national hydrogen backbone supporting industrial users and imports.

Regulatory and Policy Environment

Government policy has become a central factor in hydrogen pipeline development because transmission infrastructure requires long investment horizons, coordinated planning, and regulatory certainty before private capital can be deployed. Unlike conventional natural gas networks, hydrogen pipelines often operate within evolving regulatory frameworks covering safety standards, tariff structures, network access, hydrogen quality, and environmental assessment. As a result, infrastructure expansion increasingly depends on policy consistency rather than engineering capability alone.

The European Union remains the most advanced regulatory market for hydrogen transmission. Legislative measures under the Hydrogen and Decarbonised Gas Market Package establish rules for network planning, third-party access, tariff principles, and cross-border market integration. These measures reduce regulatory uncertainty while supporting the gradual development of an interconnected European hydrogen market. National hydrogen strategies in Germany, the Netherlands, France, and Spain complement these rules by identifying priority transmission corridors and providing financial support for strategic infrastructure.

Outside Europe, policy approaches remain more diverse. The United States continues supporting hydrogen infrastructure through clean hydrogen programmes established under recent federal legislation, while Japan and South Korea integrate hydrogen transmission within broader energy security and decarbonisation strategies. China continues incorporating hydrogen infrastructure into industrial and regional development plans, although implementation varies across provinces. In the Middle East, government-backed hydrogen projects increasingly combine renewable energy development, export infrastructure, and industrial diversification, creating opportunities for dedicated transmission systems linked to large-scale production facilities.

Outlook and Strategic Implications

Commercial activity during the 2026-2031 forecast period will increasingly depend on whether hydrogen production capacity, industrial demand, storage facilities, and transmission infrastructure develop at comparable rates. Pipeline investment alone will not create sustainable utilisation. Instead, commercially viable projects will require coordinated development across the entire hydrogen value chain, supported by long-term purchase agreements and predictable regulatory frameworks.

Material selection, engineering expertise, and project execution capability will remain important competitive differentiators as hydrogen transmission networks expand into higher-pressure and longer-distance applications. Suppliers capable of demonstrating hydrogen-compatible products, proven operational performance, and compliance with evolving international standards are likely to secure larger participation in strategic infrastructure projects. Continued investment in material science, inspection technologies, and digital asset monitoring will also strengthen long-term competitiveness.

Several strategic considerations are expected to shape market performance over the forecast period:

Infrastructure developers will prioritise projects supported by anchor industrial customers and long-term transport agreements to improve asset utilisation and financing prospects.

Pipeline manufacturers are expected to increase investment in hydrogen-compatible steel grades, composite materials, and quality assurance capabilities to meet evolving technical specifications.

Governments and regulators will continue aligning hydrogen production incentives with transmission planning to reduce project delays and improve network connectivity.

Industrial hydrogen users will increasingly evaluate transport reliability, lifecycle operating costs, and network availability when selecting hydrogen supply arrangements.

Technology providers and engineering companies are likely to benefit from growing demand for pipeline monitoring, compression systems, integrity management, and conversion services as hydrogen networks expand.

Although announced project pipelines indicate substantial long-term investment potential, market performance through 2031 will depend less on the volume of announced infrastructure than on the industry's ability to convert planned projects into operational assets supported by sustained hydrogen demand, regulatory clarity, and commercially viable utilisation levels.

Hydrogen Pipeline Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 5.20 billion |

| Total Market Size in 2031 | USD 12.10 billion |

| Forecast Unit | Billion |

| Growth Rate | 18.4% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Installation, Pressure, Pipeline Structure |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

BY INSTALLATION

- New Pipelines

- Repurposed/Retrofitted Natural Gas Pipelines

BY PRESSURE

- Low Pressure

- Medium Pressure

- High Pressure

BY PIPELINE STRUCTURE

- Steel

- Plastic (PE/HDPE)

- Composite

BY GEOGRAPHY

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Chile

- Argentina

- Others

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Others

- Middle East and Africa

- Saudi Arabia

- UAE

- Oman

- Algeria

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Others

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

2. RESEARCH METHODOLOGY

2.1. Research Process

2.2. Research Data

3. EXECUTIVE SUMMARY

3.1. Key Findings

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Porter’s Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of New Entrants

4.3.4. Threat of Substitutes

4.3.5. Competitive Rivalry in the Industry

4.4. Industry Value Chain Analysis

5. HYDROGEN PIPELINE MARKET, BY INSTALLATION

5.1. Introduction

5.2. New Pipelines

5.3. Repurposed/Retrofitted Natural Gas Pipelines

6. HYDROGEN PIPELINE MARKET, BY PRESSURE

6.1. Introduction

6.2. Low Pressure

6.3. Medium Pressure

6.4. High Pressure

7. HYDROGEN PIPELINE MARKET, BY PIPELINE STRUCTURE

7.1. Introduction

7.2. Steel

7.3. Plastic (PE/HDPE)

7.4. Composite

8. HYDROGEN PIPELINE MARKET, BY GEOGRAPHY

8.1. Introduction

8.2. North America

8.2.1. United States

8.2.2. Canada

8.2.3. Mexico

8.3. South America

8.3.1. Brazil

8.3.2. Chile

8.3.3. Argentina

8.3.4. Others

8.4. Europe

8.4.1. United Kingdom

8.4.2. Germany

8.4.3. France

8.4.4. Italy

8.4.5. Spain

8.4.6. Netherlands

8.4.7. Others

8.5. Middle East and Africa

8.5.1. Saudi Arabia

8.5.2. UAE

8.5.3. Oman

8.5.4. Algeria

8.5.5. Others

8.6. Asia Pacific

8.6.1. China

8.6.2. Japan

8.6.3. India

8.6.4. South Korea

8.6.5. Australia

8.6.6. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

10. COMPANY PROFILES

10.1. Cenergy Holdings (Corinth Pipeworks)

10.2. Tenaris

10.3. GF Piping Systems

10.4. Pipelife International GmbH

10.5. SoluForce B.V.

10.6. Siemens Energy

10.7. EUROPIPE GmbH

10.8. Mannesmann Line Pipe GmbH

10.9. Welspun Corp.

10.10. Nippon Steel Corporation

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations