Report Overview

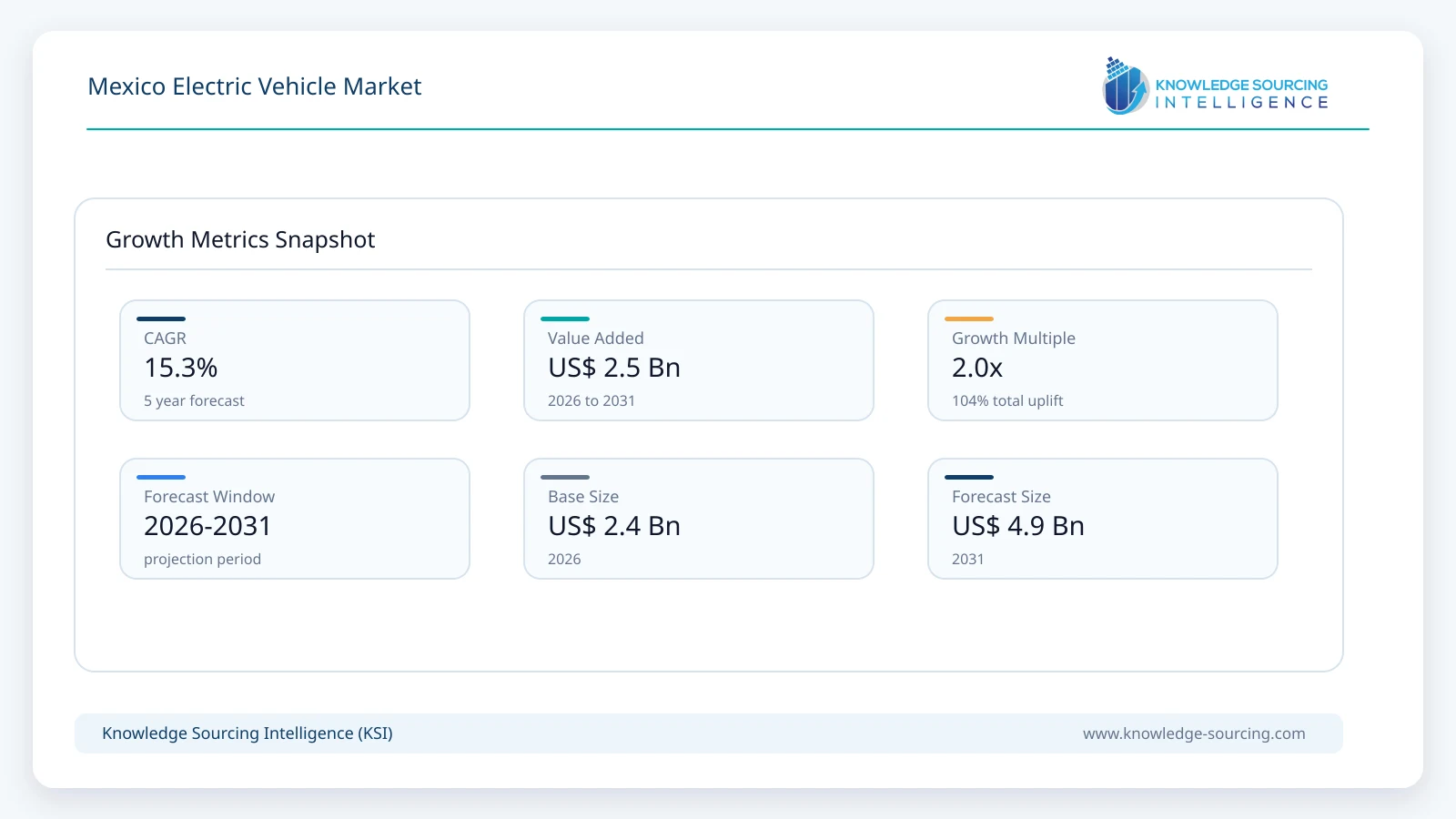

The Mexico Electric Vehicle market is forecast to grow at a CAGR of 15.3%, reaching USD 4.9 billion in 2031 from USD 2.4 billion in 2026.

Highlights:

- 1Mexico's electrified light-vehicle market continued to expand in 2026. AMDA reported that 44,183 hybrid and electric light vehicles were sold during the first quarter of 2026, while leasing companies increased their purchases of these vehicles by 65.2% year over year, highlighting growing fleet and business demand.

- 2Mexico remains a major automotive manufacturing and export base. INEGI reported that 1,299,157 light vehicles were produced during the first four months of 2026, an increase of 0.9% from the same period of 2025. Light trucks accounted for 80.0% of production during the period.

- 3Charging infrastructure is becoming more integrated with Mexico's electricity system. The Comisión Reguladora de Energía established administrative provisions through Agreement A/108/2024 for integrating electric-vehicle and plug-in hybrid charging infrastructure into the National Electric System, providing an important regulatory foundation for charging deployment.

- 4Mexico's electric-mobility opportunity extends beyond passenger cars. The Instituto Mexicano del Transporte identifies a national freight fleet of approximately 1.3 million units and notes that freight transportation represents 6.1% of GDP, making commercial-vehicle electrification an important long-term opportunity as charging capacity and vehicle economics improve.

- 5Government-backed affordable electric mobility is gaining visibility. In May 2026, Mexico's Presidency presented the Olinia electric minivehicle prototype and stated that production is planned to begin in 2027. The vehicle is designed as a low-cost, fully electric urban-mobility solution that can be charged using a conventional electrical outlet.

The Mexico electric vehicle market is moving from an early-adoption phase toward a broader electrification cycle supported by a large automotive manufacturing base, expanding model availability, fleet adoption, charging investment, and stronger integration between mobility and energy policy. The country's automotive ecosystem provides a structural advantage because vehicle assembly, components, logistics, engineering and export capabilities are already established at significant scale. INEGI recorded 1,299,157 light vehicles produced in Mexico during January-April 2026, demonstrating the scale of the industrial platform that can support further electrification.

Demand is also becoming more diversified. Electric mobility in Mexico is no longer limited to premium battery electric passenger cars. Battery electric vehicles, hybrids, plug-in hybrids, electric commercial vehicles, fleet applications and emerging low-cost urban vehicles are creating different pathways toward electrification. AMDA reported 44,183 hybrid and electric light vehicles sold during the first quarter of 2026. The same report showed that leasing companies purchased 3.2% of these vehicles as assets for customers, with their purchases increasing 65.2% from the first quarter of 2025. This indicates that leasing and corporate mobility can become important mechanisms for lowering the initial financial barrier to electrified vehicles.

The competitive environment is also changing. AMDA's Q1 2026 automotive analysis found that Asian brands accounted for 62% of Mexico's new-vehicle market, while Asian hybrid and electric vehicles recorded 105% year-over-year growth in that period. BYD was specifically identified among the brands generating strong digital demand for hybrid and electric models. These developments demonstrate why Mexico's EV competitive landscape should not be assessed only through traditional North American, European and Japanese manufacturers.

Chinese manufacturers are expanding the range of price points and powertrain options available to Mexican consumers. BYD Mexico's current portfolio includes fully electric models such as the Dolphin Mini EV, Seal EV, Yuan Pro EV and Sealion 7 EV alongside plug-in hybrid products such as the King DM-i, Song Plus DM-i and Shark. The availability of both BEV and plug-in hybrid models allows the company to address consumers with different charging access and driving requirements.

At the same time, established manufacturers are strengthening their electrification strategies. BMW reported in February 2026 that BMW and MINI achieved records for battery-electric vehicle deliveries in Mexico in 2025, while one in two fully electric BMW and MINI vehicles sold in Mexico was financed through BMW Financial Services. In April 2026, BMW also announced that the new BMW iX3 would arrive in Mexico during 2026, initially through imports from BMW Group's Debrecen plant.

General Motors is simultaneously reinforcing its Mexican manufacturing footprint. In May 2026, GM announced a new vehicle-assembly project at its Ramos Arizpe complex in Coahuila as part of the USD 1 billion investment announced in January 2026 to strengthen its Mexican operations. The first model under the new project is Chevrolet Groove, with Chevrolet Aveo planned for a subsequent phase. Although the announced project is not itself an EV-production program, it demonstrates GM's continued commitment to local manufacturing capacity and the broader Mexican automotive ecosystem in which electrification will develop.

Mexico's electrification trajectory is also being influenced by public-sector mobility programs. Hyundai Motor Company announced in 2026 that its FIFA World Cup 2026 mobility deployment would include 994 passenger vehicles and 506 buses across the 16 host cities in the United States, Canada and Mexico. The fleet includes several models with hybrid variants, providing a large-scale demonstration of electrified mobility within Mexico's World Cup transportation ecosystem.

The market nevertheless faces significant barriers. Vehicle affordability remains a central constraint, particularly because BEVs typically require higher upfront expenditure than comparable internal-combustion vehicles. Charging availability is another challenge, especially outside major metropolitan areas and along secondary intercity routes. Grid capacity, connection procedures, charging economics and the availability of suitable sites can influence the speed at which public and fleet charging infrastructure is deployed. The Instituto Mexicano del Transporte has specifically highlighted the challenges of electrifying heavy road transport, including limited energy infrastructure and the need for stronger regulation.

Consequently, Mexico's EV market should be viewed as a combination of vehicle adoption, manufacturing, charging infrastructure, fleet electrification and energy-system development. The strongest opportunities are likely to emerge where these components converge: urban passenger mobility, corporate fleets, logistics, public transportation, affordable electric vehicles, charging networks and locally integrated automotive supply chains.

Mexico Electric Vehicle Market Analysis:

Growth Drivers

Mexico's established automotive manufacturing base is one of the most important structural drivers of electric-vehicle development. The country has extensive vehicle assembly capacity, a large supplier ecosystem and established North American trade relationships. INEGI reported 1,299,157 light vehicles produced in Mexico during the first four months of 2026, while exports reached 1,140,948 units during the same period. The scale of this production and export platform gives automakers an existing industrial base from which to introduce electrified models, powertrain technologies and new manufacturing processes.

Demand growth is another important driver. The 44,183 hybrid and electric light vehicles sold during Q1 2026 demonstrate that electrified vehicles are gaining a measurable share of new-vehicle demand. The increasing participation of leasing companies is particularly relevant because fleet acquisition can reduce the importance of upfront purchase costs and allow companies to evaluate electrified vehicles on total cost of ownership, utilization and operating savings.

Asian automakers are further accelerating market development by broadening product availability. AMDA's Q1 2026 analysis identified 105% year-over-year growth for Asian hybrid and electric vehicles and reported that Asian brands represented 62% of Mexico's new-vehicle market. This competitive pressure can increase model availability, expand financing options and encourage established manufacturers to introduce more competitively priced electrified products.

Expansion of Charging Infrastructure

Charging infrastructure is becoming a central component of Mexico's EV market. The regulatory environment is evolving through the CRE's Agreement A/108/2024, which establishes administrative provisions for connecting EV and plug-in hybrid charging infrastructure to the National Electric System. The framework is important because charging stations are not simply automotive assets; they are electrical loads that require appropriate connection, safety and grid-management procedures.

The federal government's energy-planning agenda is also relevant. CENACE published its Institutional Program 2026-2030 in the Diario Oficial de la Federación in April 2026. The program establishes a strategic framework for strengthening operation of the National Electric System and the Wholesale Electricity Market, with an emphasis on security, reliability, continuity and quality of electricity supply. These priorities are directly relevant to the long-term scaling of EV charging infrastructure.

Charging deployment is increasingly likely to follow several models rather than one national infrastructure approach. Home charging can serve private owners with predictable daily travel, workplace charging can support employees and corporate fleets, destination charging can serve retail and hospitality locations, and high-power public charging can support intercity travel. Fleet depots are another important category because commercial operators can centralize charging and optimize vehicle schedules around available electrical capacity.

The challenge is not only the number of chargers but also their location, power rating, reliability and accessibility. Mexico's urban concentration means that infrastructure can initially develop rapidly in major cities while remaining less available in smaller communities and rural corridors. This creates an opportunity for charging operators, utilities, real-estate developers and fleet companies to develop geographically targeted infrastructure models.

Challenges and Opportunities

Affordability remains the largest consumer-side challenge. A BEV can provide lower energy and maintenance expenditure over its operating life, but consumers must generally absorb a larger upfront purchase price. Financing therefore becomes an important market-enabling mechanism. The increase in leasing-company purchases of hybrid and electric light vehicles during Q1 2026 illustrates the potential of alternative ownership structures. Leasing, fleet-as-a-service and other financing models can allow commercial users to adopt EVs without carrying the full capital burden of vehicle ownership.

Charging access creates a second major constraint. Consumers without dedicated parking or home charging may depend on public infrastructure, making charging availability a more important purchase consideration. This is especially relevant in dense urban areas where many households do not have private garages. For fleet operators, the challenge shifts toward depot electrical capacity, charging scheduling, route planning and vehicle utilization.

These challenges also create commercial opportunities. Companies can develop charging-as-a-service solutions, fleet charging management software, financing products, battery services and energy-management systems. Automakers can also differentiate through bundled charging solutions, extended warranties and financing packages. The development of affordable EVs can broaden the addressable market beyond premium consumers.

Raw Material and Pricing Analysis

Battery cost remains an important determinant of EV affordability and manufacturing economics. The cost structure of an electric vehicle is influenced by battery cells, cathode and anode materials, power electronics, electric motors, thermal-management systems and other specialized components. Mexico's strategic importance is therefore linked not only to vehicle assembly but also to the gradual localization of components and related supply-chain activities.

Mexico's lithium policy should be treated carefully in market analysis. Lithium resources in the country do not automatically translate into large-scale domestic battery manufacturing. The existence of mineral resources, mining policy, extraction technology, processing capacity, environmental requirements and investment conditions are separate issues. Therefore, it would be inaccurate to state that Mexico's lithium resources will automatically reduce EV production costs or make the country self-sufficient in battery materials.

A more defensible assessment is that Mexico has a strategic opportunity to participate in the North American battery value chain while continuing to rely on international sources for many critical materials and components. The country's proximity to the United States, established automotive supplier network and manufacturing capabilities can support regional sourcing as battery and EV production expands.

Inadequate Charging Network Density

Charging-network density remains a constraint, particularly for long-distance travel and consumers without home charging. The problem is geographical as well as numerical. A relatively high concentration of chargers in major metropolitan areas does not eliminate the need for reliable charging corridors connecting industrial centers, tourism destinations and secondary cities.

The challenge is more pronounced for commercial and heavy vehicles. The Instituto Mexicano del Transporte estimates that Mexico has approximately 1.3 million freight units and notes that freight transportation accounts for 6.1% of GDP. Electrifying this fleet will require high-capacity charging, suitable depot infrastructure, grid upgrades and route-specific energy planning.

Electricity supply is another consideration. The IMT has highlighted the limited share of electricity generated from clean sources and the difficulty of expanding charging infrastructure supported by clean energy. This means that the EV market should increasingly be analyzed alongside electricity generation, transmission, distribution and energy-storage developments rather than as an isolated automotive market.

Mexico's Olinia project provides another perspective on the infrastructure challenge. The government presented the Olinia prototype in May 2026 as an affordable fully electric urban vehicle and stated that production is planned for 2027. The vehicle is designed to use a conventional electrical outlet for charging, which could reduce dependence on specialized charging infrastructure for some urban applications.

Supply Chain Analysis

Mexico's automotive supply chain provides a significant competitive advantage for EV development. The country already has extensive capabilities in vehicle assembly, stamping, powertrain components, electronics, wiring systems, seats, interiors, logistics and vehicle exports. The transition to EVs will alter the composition of this ecosystem by increasing demand for batteries, electric motors, inverters, power electronics, battery-management systems and thermal-management components.

Nearshoring can support this transition, but the effect should not be overstated. Mexico's ability to attract EV-related investment depends on labor availability, electricity reliability, infrastructure, logistics, trade rules, supplier localization and access to critical materials. The USMCA framework remains an important factor for North American automotive manufacturing, but individual investment decisions depend on broader cost and regulatory considerations.

The industrial opportunity is already visible in company activity. BMW stated in June 2026 that its San Luis Potosí plant's next stage will include production of Neue Klasse electric vehicles and high-voltage batteries beginning in 2027. This is a particularly significant development because it connects Mexican vehicle production with next-generation EV architecture and battery manufacturing.

Government Regulations

Jurisdiction | Key Regulation / Agency | Market Impact Analysis |

|---|---|---|

National | Comisión Reguladora de Energía, Agreement A/108/2024 | Establishes administrative provisions for integrating EV and plug-in hybrid charging infrastructure into the National Electric System, creating a clearer framework for charging connections and grid integration. |

National | CENACE Institutional Program 2026-2030 | Strengthens the strategic framework for secure, reliable and continuous operation of the National Electric System, which is relevant to the long-term expansion of electricity demand from EV charging. |

National | Olinia Electric Mobility Program | Supports development of an affordable Mexican electric minivehicle. The government presented the prototype in May 2026 and stated that production is planned to begin in 2027. |

Federal and Local | Vehicle taxation, emissions and mobility measures | Tax treatment, emissions-control programs and local driving restrictions can influence the relative operating and ownership economics of electrified vehicles. Their application should be assessed separately by jurisdiction rather than treated as a single nationwide incentive. |

Mexico Electric Vehicle Market Segment Analysis:

By Propulsion Type: Battery Electric Vehicle (BEV)

The BEV segment represents the clearest long-term pathway toward zero-tailpipe-emission road transport because the vehicle is propelled entirely by electricity and does not require an internal-combustion engine for propulsion. BEV demand in Mexico is supported by expanding model availability, improvements in range and charging technology, increasing consumer awareness and the growth of charging infrastructure.

Competition within the BEV segment is becoming more diverse. Tesla remains an important premium and technology-focused player, while BYD is expanding the range of more accessible electric models. BYD Mexico currently lists the Dolphin Mini EV, Seal EV, Yuan Pro EV and Sealion 7 EV among its electric products. The 2026 Dolphin Mini is positioned as a fully electric hatchback and is offered with the Blade Battery and a stated NEDC range of up to 380 km, demonstrating how smaller and more affordable EVs are becoming part of the Mexican product mix.

Tesla's continued charging ecosystem is also relevant to BEV adoption. Tesla's Mexico charging information provides home, destination and Supercharger solutions, while its Mexican website continues to market the Model 3 and Model Y. The company states that its Supercharger network supports high-speed charging, with charging speeds depending on vehicle and station configuration.

BMW is expanding the premium BEV proposition in Mexico through its Neue Klasse strategy. In April 2026, BMW announced that the new BMW iX3 would arrive in Mexico during the year, initially imported from Hungary, before the company expands its next-generation electric production strategy. BMW also stated in June 2026 that its San Luis Potosí plant will begin production of Neue Klasse electric vehicles and high-voltage batteries from 2027.

The key BEV opportunity therefore extends beyond vehicle sales. It includes home chargers, public charging, fleet charging, financing, battery services, software, energy management and maintenance. As charging access improves and lower-priced models enter the market, BEVs can expand from affluent urban consumers toward a broader range of private and commercial users.

By Propulsion Type: Hybrid Electric Vehicle (HEV)

HEVs are particularly important to Mexico's electrification pathway because they reduce fuel consumption without requiring the driver to depend on external charging infrastructure. This characteristic makes them attractive to consumers who want lower fuel use and emissions but face limited access to home or public charging.

The scale of HEV demand is visible in the broader hybrid-and-electric sales data. AMDA reported 44,183 hybrid and electric light vehicles sold during the first quarter of 2026. The continued presence of HEVs alongside BEVs and PHEVs means that Mexico's transition is likely to remain multi-powertrain rather than shifting immediately to battery-electric vehicles alone.

Asian automakers are particularly important in this segment. AMDA's Q1 2026 analysis reported 105% year-over-year growth for Asian hybrid and electric vehicles and highlighted strong demand for models such as the BYD King and Honda CR-V Hybrid. This suggests that consumers are increasingly willing to consider electrified powertrains when they provide a balance between fuel savings, range and convenience.

BYD's Mexican portfolio demonstrates the convergence between HEV and plug-in hybrid technology. Its King DM-i and Song Plus DM-i provide electric driving capability while retaining an internal-combustion component, offering consumers a transition route where charging infrastructure is not yet sufficient for a pure BEV.

Mexico Electric Vehicle Market Competitive Analysis:

The Mexico EV competitive environment is becoming increasingly fragmented and technology-diverse. Established North American, European and Japanese automakers are competing with rapidly expanding Chinese brands, while local initiatives such as Olinia add a domestic dimension. Competitive positioning is increasingly based on product price, financing, battery technology, charging support, after-sales service, manufacturing footprint and the ability to address different vehicle segments.

Tesla, Inc.

Tesla maintains a strong position in Mexico's premium BEV segment through its Model 3 and Model Y portfolio and integrated charging ecosystem. Its Mexican website currently promotes the Model Y and Model 3 and provides access to Supercharger and Destination Charger information. Tesla's Mexican support pages also describe Supercharging capabilities and the company's charging-payment ecosystem.

Tesla's competitive advantage is therefore not limited to the vehicle itself. The combination of software, charging, vehicle connectivity and direct customer interaction creates an integrated ownership proposition. The company also continues to evaluate access to its Supercharger network for non-Tesla EVs in selected markets, although availability varies by market and connector compatibility.

General Motors Company

General Motors remains a strategically important player because of its manufacturing scale and long-standing Mexican presence. In May 2026, GM announced a new assembly project at Ramos Arizpe, Coahuila, forming part of the USD 1 billion investment announced earlier in the year to strengthen its Mexican operations. The project is initially focused on Chevrolet Groove and later Chevrolet Aveo production for the domestic market.

Although this specific investment is not an announced BEV program, the broader significance for the EV market lies in GM's continued investment in Mexican production capacity. A large installed manufacturing and supplier base can facilitate future platform, component and electrification changes while strengthening the company's ability to serve the domestic market.

BMW AG

BMW is strengthening its Mexico electrification position through both product expansion and local manufacturing. In February 2026, BMW reported record BEV sales for BMW and MINI in Mexico during 2025. In April 2026, the company announced that the new BMW iX3 would arrive in Mexico during 2026. In June 2026, BMW confirmed that its San Luis Potosí operation will enter a new phase involving Neue Klasse electric vehicles and high-voltage batteries from 2027.

BYD Company Limited

BYD has become an increasingly important competitor in Mexico because of its broad range of BEV and plug-in hybrid models. Its Mexican portfolio includes the Dolphin Mini EV, Seal EV, Yuan Pro EV, Sealion 7 EV, King DM-i and Song Plus DM-i, among others. The company also has active Mexican sales and service infrastructure and continues to introduce 2026-model-year products.

BYD's competitive positioning is particularly relevant to the price-accessibility dimension of the Mexican EV market. Its use of internally developed battery and electric-powertrain technologies, combined with a broad portfolio, allows the company to compete across several electrified-vehicle categories rather than relying solely on premium BEVs.

Mexico Electric Vehicle Market Developments:

June 2026: BMW Group confirmed that its San Luis Potosí plant will enter its next electrification phase, with production of Neue Klasse electric vehicles and high-voltage batteries planned from 2027. The development strengthens Mexico's role in BMW's global electric-vehicle production network.

May 2026: General Motors announced a new vehicle-assembly project at its Ramos Arizpe, Coahuila complex as part of the USD 1 billion investment announced in January 2026 to strengthen its Mexican operations. Production for the Mexican market is scheduled to begin with Chevrolet Groove in 2027, followed by Chevrolet Aveo in a later phase.

May 2026: Mexico's Presidency presented the Olinia electric minivehicle prototype and stated that production is planned to begin in 2027. The vehicle is designed as a low-cost, fully electric urban-mobility solution capable of charging from a conventional outlet.

Mexico Electric Vehicle Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 2.4 billion |

| Total Market Size in 2031 | USD 4.9 billion |

| Forecast Unit | Billion |

| Growth Rate | 15.3% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Vehicle Type, Propulsion Type, Drive Type, Component, End User |

| Companies |

|

Market Segmentation

By Vehicle Type

By Propulsion Type

By Drive Type

By Component

By End User

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Taxonomy

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Charging Infrastructure and Investment Landscape

3.8. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

4.1. Battery Technology

4.2. Electric Motor and Power Electronics

4.3. Battery Management Systems

4.4. Charging Technology

4.5. Fast-Charging Technology

4.6. Vehicle Connectivity and Software

4.7. Vehicle-to-Grid and Bidirectional Charging

5. MEXICO ELECTRIC VEHICLE MARKET BY VEHICLE TYPE

5.1. Introduction

5.2. Passenger Vehicles

5.3. Commercial Vehicles

6. MEXICO ELECTRIC VEHICLE MARKET BY PROPULSION TYPE

6.1. Introduction

6.2. Battery Electric Vehicle (BEV)

6.3. Hybrid Electric Vehicle (HEV)

6.4. Plug-in Hybrid Electric Vehicle (PHEV)

6.5. Fuel Cell Electric Vehicle (FCEV)

7. MEXICO ELECTRIC VEHICLE MARKET BY DRIVE TYPE

7.1. Introduction

7.2. Front-Wheel Drive

7.3. Rear-Wheel Drive

7.4. All-Wheel Drive

8. MEXICO ELECTRIC VEHICLE MARKET BY COMPONENT

8.1. Introduction

8.2. Battery Cells and Packs

8.3. Electric Motors

8.4. Onboard Chargers

8.5. Power Electronics and Inverters

8.6. Braking, Wheels, and Suspension

8.7. Thermal Management Systems

8.8. Others

9. MEXICO ELECTRIC VEHICLE MARKET BY END USER

9.1. Introduction

9.2. Individual Consumers

9.3. Commercial Fleets

9.4. Government and Public-Sector Fleets

10. COMPETITIVE ENVIRONMENT AND ANALYSIS

10.1. Major Players and Strategy Analysis

10.2. Market Share Analysis

10.3. Mergers, Acquisitions, Agreements, and Collaborations

10.4. Competitive Dashboard

11. COMPANY PROFILES

11.1. Volkswagen Group

11.2. Ford Motor Company

11.3. General Motors Company

11.4. Tesla, Inc.

11.5. Anhui Jianghuai Automobile Group Corp., Ltd. (JAC)

11.6. Toyota Motor Corporation

11.7. BMW AG

11.8. Hyundai Motor Company

11.9. Stellantis N.V.

11.10. Zacua, S.A. de C.V.

11.11. Kia Corporation

11.12. Mazda Motor Corporation

11.13. BYD Company Limited

12. RESEARCH METHODOLOGY

List of Figures

List of Tables

Navigate

Trusted by the world's leading organizations