Report Overview

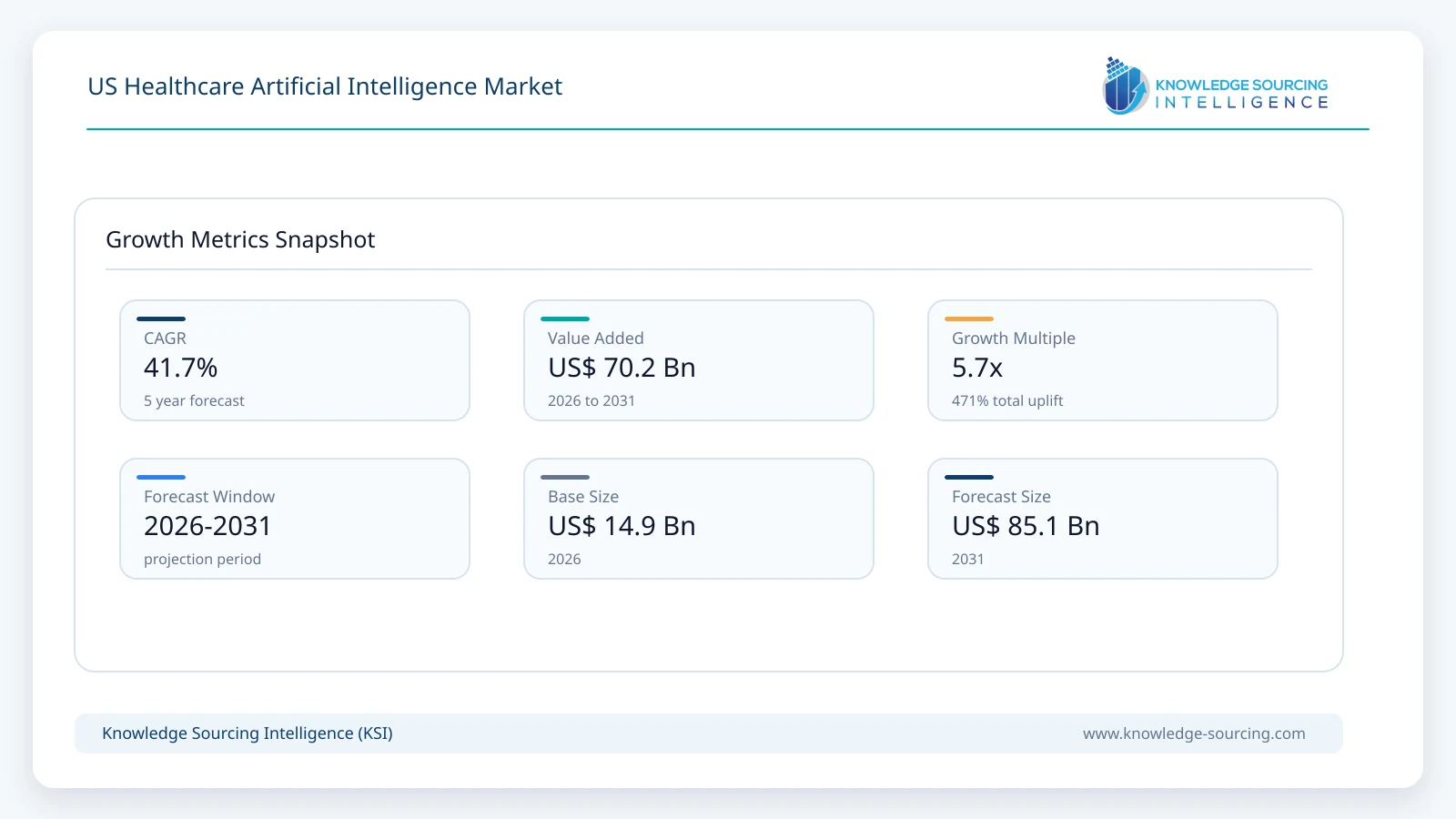

The US Healthcare Artificial Intelligence Market is projected to grow at a CAGR of 41.7%, rising from USD 14.9 billion in 2026 to USD 85.1 billion by 2031.

Highlights:

- 1Medical imaging and diagnostics remain the largest commercial application due to established reimbursement pathways and extensive imaging volumes across US healthcare systems.

- 2Hospitals and integrated healthcare providers represent the primary purchasing group because of broad enterprise-level AI implementation requirements.

- 3Generative AI is expanding investment across clinical documentation, patient communication, and administrative workflow optimization.

- 4Federal initiatives supporting responsible AI deployment and healthcare interoperability continue to shape purchasing requirements.

- 5Demand increasingly favors vendors offering clinically validated, interoperable, and scalable AI platforms rather than standalone algorithms.

- 6Cloud infrastructure partnerships between healthcare software providers and hyperscale technology companies continue to influence competitive positioning.

The US Healthcare Artificial Intelligence (AI) market comprises software platforms, AI models, computing infrastructure, and professional services that enable healthcare organizations to improve clinical decision-making, operational efficiency, medical research, patient engagement, and administrative processes through data-driven automation and predictive analytics. The market spans technologies including machine learning, deep learning, natural language processing (NLP), computer vision, and generative AI, serving hospitals, physician groups, pharmaceutical companies, diagnostic laboratories, research institutions, and healthcare technology providers.

Demand for healthcare AI in the United States is supported by structural pressures affecting the healthcare system rather than short-term technology trends. Healthcare providers continue to manage rising treatment costs, clinician shortages, increasing chronic disease prevalence, and expanding diagnostic workloads. AI applications are being evaluated based on measurable financial outcomes such as shorter reporting times, lower administrative expenses, improved resource utilization, reduced readmissions, and enhanced diagnostic consistency.

Procurement priorities have also changed considerably over the past several years. Healthcare organizations now place greater emphasis on interoperability with electronic health record (EHR) systems, cybersecurity controls, explainable AI capabilities, regulatory compliance, and clinical validation before large-scale deployment. Purchasing decisions increasingly involve multidisciplinary teams consisting of clinical leadership, IT departments, compliance officers, procurement specialists, and finance executives, reflecting the operational impact of AI implementation.

The industry structure combines established healthcare technology vendors with cloud computing providers, semiconductor manufacturers, specialized medical AI developers, and clinical software companies. Competition is driven by model performance, workflow integration, regulatory clearances, implementation support, and long-term service capabilities rather than algorithmic accuracy alone.

Revenue generation is becoming more diversified across software licensing, cloud subscriptions, AI-enabled medical devices, infrastructure investments, implementation consulting, and managed AI services. Large integrated delivery networks often pursue enterprise-wide AI deployment strategies, while smaller healthcare providers increasingly adopt cloud-based subscription models to minimize upfront capital expenditure.

Technology adoption varies across healthcare functions. Diagnostic imaging remains among the most mature applications because standardized imaging datasets support model development and clinical validation. Administrative workflow automation, clinical documentation, drug discovery, remote patient monitoring, and generative AI-assisted clinical decision support are expanding as healthcare organizations gain greater confidence in AI governance frameworks and regulatory oversight.

Market Drivers

Growing Diagnostic Workloads and Workforce Constraints

US healthcare providers continue to experience rising diagnostic volumes alongside shortages of radiologists, pathologists, nurses, and administrative personnel. AI enables healthcare organizations to prioritize abnormal cases, automate repetitive image analysis, and reduce documentation burdens, allowing clinicians to focus on complex patient care.

Hospital buyers increasingly seek measurable productivity improvements rather than experimental AI capabilities. Vendors therefore compete by demonstrating workflow efficiency, shorter turnaround times, and clinical validation studies. This purchasing behavior favors suppliers capable of integrating AI directly into existing hospital information systems.

Expansion of Precision Medicine and Data-Driven Clinical Care

Healthcare organizations are investing in personalized treatment strategies supported by genomic sequencing, biomarker analysis, and large clinical datasets. AI improves the interpretation of complex biological information, helping physicians identify appropriate treatment pathways while accelerating pharmaceutical research.

Pharmaceutical companies and academic medical centers represent important demand sources because AI reduces analytical complexity and supports larger research programs. Technology providers continue expanding specialized AI platforms capable of integrating genomic, imaging, laboratory, and clinical data into unified analytical environments.

Increasing Administrative Cost Pressures

Administrative activities account for a substantial portion of healthcare expenditure in the United States. Clinical documentation, coding, prior authorization, appointment scheduling, and revenue cycle management remain labor-intensive processes.

Natural language processing and generative AI are being adopted to automate documentation and administrative workflows while maintaining regulatory compliance. Healthcare organizations increasingly evaluate AI investments based on operational cost savings, creating opportunities for software providers with enterprise automation capabilities.

Growth in Cloud-Based Healthcare Infrastructure

Healthcare organizations continue migrating clinical applications toward cloud environments to improve scalability, computing performance, and data accessibility. AI model training and deployment require substantial computational resources, making cloud infrastructure an attractive option for providers with limited internal computing capacity.

Cloud adoption also supports continuous model updates, centralized cybersecurity management, and easier integration with enterprise healthcare applications. Vendors increasingly differentiate themselves through secure cloud architectures compliant with healthcare privacy regulations.

Market Restraints and Challenges

Regulatory Uncertainty for Clinical AI Applications

Although regulatory oversight continues to evolve, healthcare organizations remain cautious when implementing AI solutions that directly influence clinical decisions. Approval pathways for adaptive algorithms require ongoing evidence generation and post-market monitoring.

Healthcare providers therefore conduct extensive validation before procurement, extending purchasing cycles and increasing implementation costs. Suppliers must maintain continuous regulatory compliance while updating AI models to reflect changing clinical evidence.

Data Privacy and Cybersecurity Risks

Healthcare data remain among the most sensitive categories of personal information. AI deployment requires access to extensive patient datasets, increasing concerns regarding privacy protection, cybersecurity, and data governance.

Hospitals often require vendors to demonstrate compliance with HIPAA requirements, encryption standards, audit capabilities, and secure cloud environments before contract approval. These requirements increase development costs while raising barriers for smaller AI vendors.

Integration Complexity Across Healthcare Systems

Many healthcare organizations continue operating multiple legacy information systems developed by different vendors over several decades. Integrating AI applications into existing workflows frequently requires extensive customization and interoperability testing.

Implementation complexity can delay return on investment and increase project costs. Vendors capable of supporting standardized interoperability frameworks and providing implementation services generally experience stronger commercial adoption.

Clinical Trust and Explainability Requirements

Healthcare professionals remain responsible for final clinical decisions regardless of AI recommendations. Black-box algorithms without transparent reasoning may encounter resistance among physicians, particularly in high-risk specialties.

Suppliers increasingly invest in explainable AI, clinical evidence generation, and physician education to improve adoption while supporting regulatory expectations for transparency.

Major Segment Analysis

Medical Imaging and Diagnostics

Medical imaging and diagnostics represent the most commercially important application within the US Healthcare Artificial Intelligence market due to the combination of large imaging volumes, standardized workflows, and measurable productivity improvements. Radiology departments process millions of imaging studies annually, creating substantial demand for technologies that improve prioritization, interpretation, and reporting efficiency.

Hospitals purchase AI imaging platforms primarily to reduce reporting delays, improve consistency across clinical teams, and support earlier disease detection. Procurement decisions emphasize clinical validation, FDA clearances, compatibility with existing picture archiving and communication systems (PACS), and seamless integration into radiologist workflows. Healthcare providers generally prefer enterprise platforms capable of supporting multiple imaging modalities instead of single-purpose applications.

Competition within this segment increasingly centers on workflow integration rather than image recognition accuracy alone. Vendors differentiate through comprehensive clinical evidence, implementation support, cybersecurity capabilities, cloud deployment options, and long-term software maintenance. AI-assisted imaging also generates recurring revenue through subscription licensing and software updates, making it commercially attractive for suppliers while supporting continuous product improvement.

Competitive Landscape

The US Healthcare Artificial Intelligence market remains moderately concentrated, combining multinational technology companies with specialized healthcare AI developers. Competition extends across cloud infrastructure, AI software, medical imaging applications, enterprise analytics, and clinical workflow optimization.

Suppliers increasingly compete through integrated technology ecosystems that combine cloud computing, AI development platforms, healthcare data management, cybersecurity, and implementation services. Strategic collaborations between healthcare providers, pharmaceutical companies, academic institutions, and cloud service providers have become an important route for accelerating clinical validation and commercial deployment.

Product differentiation increasingly depends on interoperability with electronic health records, regulatory compliance, explainable AI capabilities, enterprise scalability, and long-term service support. Companies are also expanding computing capacity, investing in specialized healthcare foundation models, and strengthening partnerships with hospital systems to improve customer retention and broaden clinical applications.

Recent Developments

July 2026: Cigna Healthcare announced expanded deployment of AI-driven clinical programs expected to save customers US$200 million in medical expenses over three years by improving early identification of high-risk patients and expanding personalized care interventions.

May 2026: ARPA-H launched the Intelligent Generator of Research (IGoR) program, introducing an AI-powered biomedical research ecosystem designed to accelerate reproducible healthcare research, improve disease modeling, and speed scientific discovery across the United States.

February 2026: The U.S. Department of Health and Human Services (HHS) announced that TEFCA had reached nearly 500 million health records exchanged, while expanding the use of artificial intelligence to improve interoperability, lower healthcare costs, and reduce administrative burden across the U.S. healthcare ecosystem.

January 2026: GE HealthCare expanded AI-enabled imaging workflow capabilities through new intelligent imaging software enhancements presented at major healthcare technology events. Commercial relevance: strengthens enterprise imaging productivity and supports broader hospital AI adoption.

Regulatory and Policy Environment

The regulatory framework governing healthcare AI in the United States continues to mature through coordinated oversight by federal agencies. The US Food and Drug Administration regulates AI-enabled Software as a Medical Device (SaMD), establishing expectations for clinical validation, quality management, lifecycle monitoring, and post-market performance evaluation. Developers seeking commercialization of diagnostic AI applications must demonstrate safety, effectiveness, and appropriate risk management.

The Health Insurance Portability and Accountability Act (HIPAA) remains central to healthcare AI deployment by establishing requirements for patient data privacy, security safeguards, and protected health information management. Healthcare providers increasingly require AI vendors to demonstrate compliance through independent security assessments and contractual data protection commitments.

Federal initiatives supporting healthcare interoperability encourage standardized data exchange across electronic health records, facilitating AI integration while reducing implementation complexity. Government guidance regarding trustworthy and responsible AI also encourages transparency, risk management, documentation, and human oversight for clinical applications.

Outlook and Strategic Implications

Over the next five years, procurement activity is expected to shift toward enterprise-wide AI platforms capable of supporting multiple clinical and administrative functions through a unified technology architecture. Healthcare organizations will increasingly prioritize vendors that demonstrate measurable operational benefits, regulatory readiness, cybersecurity resilience, and seamless interoperability with existing clinical systems.

Investment is likely to remain concentrated in generative AI, medical imaging, clinical documentation, precision medicine, and hospital workflow optimization. Demand for accelerated computing infrastructure and secure healthcare cloud platforms should continue expanding as AI workloads become more computationally intensive.

Competitive positioning will depend less on standalone algorithms and more on comprehensive healthcare ecosystems combining cloud infrastructure, AI software, implementation services, governance capabilities, and long-term customer support. Suppliers able to demonstrate sustained clinical value, regulatory compliance, and scalable deployment models are expected to strengthen their commercial position.

Despite continuing opportunities, buyers are expected to maintain disciplined procurement practices focused on evidence generation, cybersecurity, return on investment, and responsible AI governance. These factors will shape supplier selection and determine the pace of adoption across the US Healthcare Artificial Intelligence market through the forecast period.

US Healthcare Artificial Intelligence Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 14.9 billion |

| Total Market Size in 2031 | USD 85.1 billion |

| Forecast Unit | Billion |

| Growth Rate | 41.7% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Technology, Application, Offering, End-User |

| Companies |

|

Market Segmentation

By Technology

By Application

By Offering

By End User

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter's Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. US HEALTHCARE ARTIFICIAL INTELLIGENCE MARKET BY TECHNOLOGY

5.1. Introduction

5.2. Machine Learning

5.3. Deep Learning

5.4. Natural Language Processing (NLP)

5.5. Computer Vision

5.6. Generative AI

6. US HEALTHCARE ARTIFICIAL INTELLIGENCE MARKET BY APPLICATION

6.1. Introduction

6.2. Medical Imaging and Diagnostics

6.3. Precision Medicine

6.4. Virtual Assistants

6.5. Drug Discovery and Development

6.6. Clinical Workflow and Hospital Management

6.7. Remote Patient Monitoring and Wearables

6.8. Lifestyle Management

6.9. Clinical Research

7. US HEALTHCARE ARTIFICIAL INTELLIGENCE MARKET BY OFFERING

7.1. Introduction

7.2. Hardware

7.3. Software

7.4. Services

8. US HEALTHCARE ARTIFICIAL INTELLIGENCE MARKET BY END USER

8.1. Introduction

8.2. Hospitals and Healthcare Providers

8.3. Pharmaceutical and Biotechnology Companies

8.4. Diagnostic Laboratories

8.5. Academic and Research Institutes

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Competitive Dashboard

10. COMPANY PROFILES

10.1. GE HealthCare Technologies Inc.

10.2. NVIDIA Corporation

10.3. Microsoft Corporation

10.4. Google LLC

10.5. Oracle Corporation

10.6. Enlitic, Inc.

10.7. Tempus AI, Inc.

10.8. Aidoc Medical Ltd.

10.9. Butterfly Network, Inc.

10.10. Amazon Web Services, Inc.

11. APPENDIX

11.1. Currency

11.2. Assumptions

11.3. Base and Forecast Years Timeline

11.4. Key Benefits for Stakeholders

11.5. Research Methodology

11.6. Abbreviations

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations