Report Overview

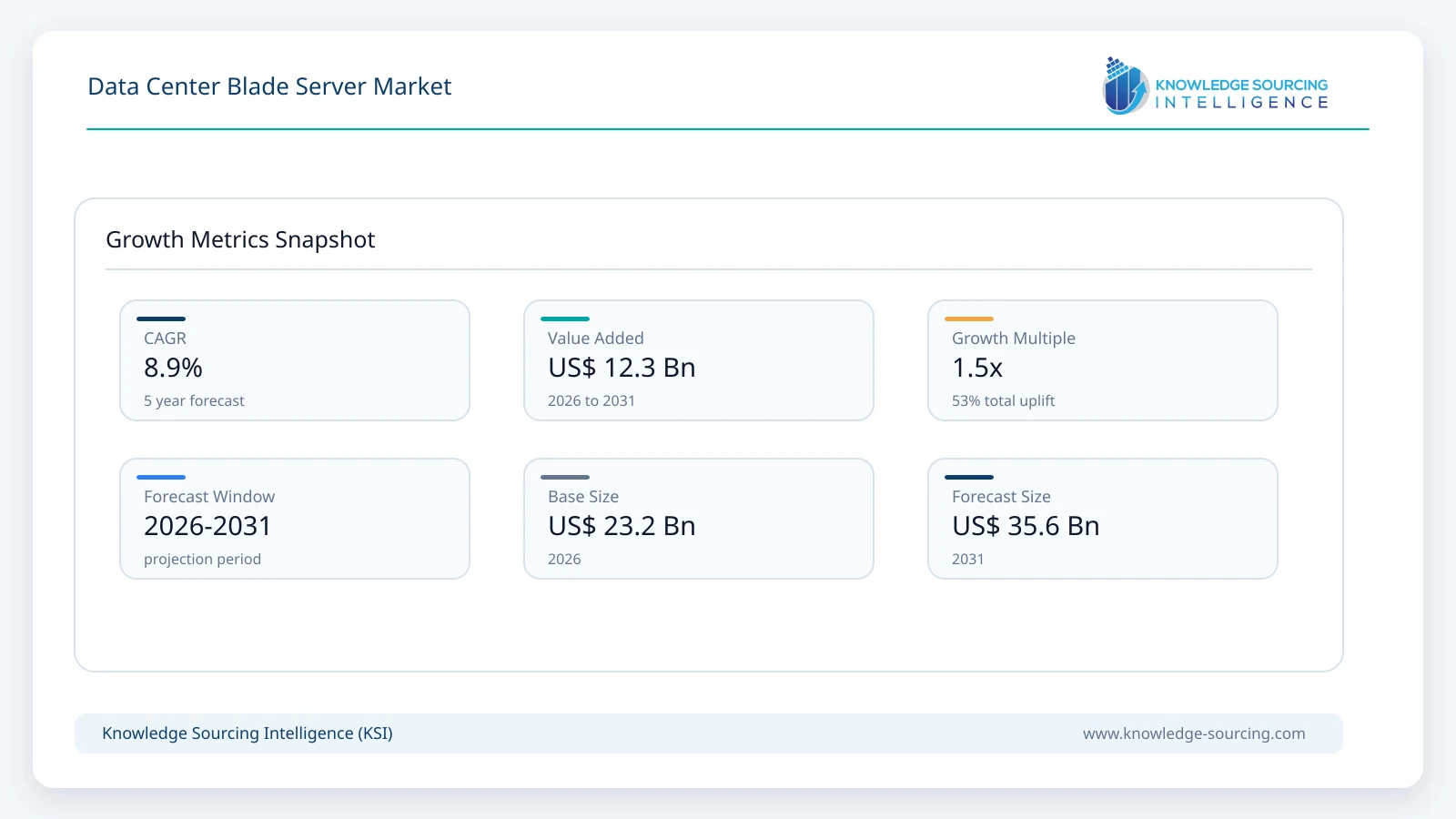

The Data Center Blade Server Market is forecast to grow at a CAGR of 8.90%, reaching USD 35.56 billion in 2031 from USD 23.22 billion in 2026.

Highlights:

- 1Growing enterprise virtualization and hybrid cloud deployment continue to support demand for dense blade server infrastructure.

- 2Cloud service providers represent one of the most influential end-user groups because of continuous capacity expansion and workload consolidation.

- 3Asia Pacific offers substantial long-term opportunities as governments and private investors expand hyperscale and enterprise data center infrastructure.

- 4Integration of advanced processors, GPU acceleration, automation software, and intelligent infrastructure management is reshaping procurement priorities.

- 5Energy efficiency regulations and sustainability targets are encouraging adoption of higher-density computing platforms with optimized power utilization.

- 6Competition is increasingly centered on integrated infrastructure ecosystems, lifecycle services, and software-enabled infrastructure management rather than hardware specifications alone.

The data center blade server market comprises compact, modular server systems designed to share common infrastructure components such as power supplies, cooling systems, networking modules, and management software within a single chassis. Blade server architecture enables organizations to maximize computing density while reducing physical footprint and simplifying infrastructure management. These systems are widely deployed in enterprise data centers, cloud facilities, government computing environments, financial institutions, and high-performance computing (HPC) clusters where processing efficiency, scalability, and centralized administration are operational priorities.

Demand for blade servers is closely linked to enterprise computing modernization and the expansion of digital infrastructure. Organizations continue to consolidate workloads while accommodating growing volumes of business applications, virtualization platforms, databases, analytics, artificial intelligence (AI), and cloud-native services. Blade servers remain relevant in environments requiring predictable performance, centralized management, and high compute density, particularly where space and energy utilization directly influence operating costs.

Purchasing decisions increasingly reflect total cost of ownership rather than hardware acquisition alone. Buyers evaluate server density, power efficiency, lifecycle management, compatibility with virtualization platforms, processor roadmap support, security capabilities, and serviceability. Enterprises also prioritize vendor support, firmware lifecycle management, and integration with existing networking and storage ecosystems. These considerations are especially important for organizations operating mission-critical applications with stringent availability requirements.

Cloud service providers and colocation operators represent major procurement groups due to continuous expansion of computing capacity. Large enterprises remain important buyers as they modernize legacy server estates and consolidate multiple rack servers into modular architectures. Government agencies and financial institutions continue investing in blade infrastructure to support secure computing environments, disaster recovery capabilities, and regulated workloads requiring high reliability.

Industry structure reflects a concentrated competitive environment where established infrastructure vendors compete through platform integration, system reliability, management software, processor compatibility, and global service capabilities. Suppliers increasingly combine blade servers with storage, networking, software-defined infrastructure, and lifecycle services to address broader data center modernization initiatives. Hardware sales are therefore supported by recurring revenue from maintenance contracts, software subscriptions, consulting services, and infrastructure management.

Market Drivers

One of the primary drivers is sustained investment in cloud computing infrastructure. Public cloud providers, managed service providers, and enterprise private cloud operators require server platforms capable of supporting large numbers of virtual machines with efficient resource allocation. Blade servers enable centralized administration and high compute density, allowing operators to expand capacity while optimizing data center space and operational efficiency. Vendors continue introducing platforms compatible with new processor generations, high-speed networking, and memory-intensive workloads to meet these procurement requirements.

Virtualization remains another important demand catalyst. Organizations seek to reduce infrastructure complexity by consolidating multiple physical servers into virtualized environments. Blade systems support this objective by providing standardized hardware, integrated networking, and centralized management tools. Procurement teams increasingly evaluate infrastructure according to workload flexibility, hardware utilization rates, and lifecycle efficiency instead of standalone server performance. Suppliers respond through management software that automates provisioning, monitoring, firmware updates, and workload balancing.

Expansion of artificial intelligence, analytics, and high-performance computing workloads also supports commercial demand. Research institutions, manufacturing companies, healthcare organizations, engineering firms, and financial institutions process increasingly complex computational tasks requiring scalable computing platforms. Modern blade server architectures support high-core-count processors, accelerator technologies, and advanced networking capabilities that improve computational efficiency for parallel processing environments. This strengthens demand among organizations pursuing advanced digital workloads while maintaining centralized infrastructure management.

Enterprise modernization programs further contribute to procurement activity. Many organizations continue replacing aging server infrastructure approaching end-of-support status. Modern blade platforms offer improved processor performance, memory capacity, storage flexibility, and energy efficiency compared with legacy deployments. Buyers often align infrastructure refresh cycles with broader initiatives involving cybersecurity improvements, hybrid cloud integration, disaster recovery modernization, and business continuity planning, expanding the commercial value of blade server investments.

Market Restraints and Challenges

Growing adoption of hyperconverged infrastructure presents an important competitive challenge. Many organizations are shifting toward software-defined infrastructure that combines compute, storage, and virtualization within distributed clusters. For some enterprise workloads, hyperconverged systems reduce deployment complexity and simplify scaling. This changes procurement priorities and may reduce demand for conventional blade deployments in selected application environments. Vendors address this challenge by integrating blade platforms with software-defined infrastructure and hybrid cloud management capabilities.

High capital expenditure remains another constraint, particularly for mid-sized enterprises. Blade infrastructure requires investment in chassis, networking modules, storage integration, management software, and supporting infrastructure. Organizations with limited capital budgets may extend the operational life of existing rack servers or adopt cloud-based infrastructure instead of purchasing new blade systems. Suppliers increasingly offer financing models, consumption-based infrastructure services, and lifecycle management contracts to improve purchasing flexibility.

Power availability and thermal management continue influencing infrastructure deployment decisions. Although blade servers improve computing density, they also increase localized power and cooling requirements within data centers. Operators must invest in advanced cooling technologies, electrical distribution upgrades, and environmental monitoring systems. These additional infrastructure costs can delay modernization projects, particularly where facilities have limited expansion capacity.

Supply chain resilience also remains an operational consideration. Semiconductor availability, advanced processor lead times, memory component pricing, and specialized networking equipment influence production schedules and procurement planning. Enterprise buyers increasingly diversify purchasing schedules, negotiate longer-term procurement agreements, and maintain strategic inventory to reduce deployment delays associated with component availability.

Major Segment Analysis

Cloud Service Providers represent the most commercially influential end-user segment because of continuous investment in computing infrastructure supporting enterprise workloads, digital services, artificial intelligence applications, and software platforms. These organizations operate facilities requiring standardized, scalable, and highly manageable server architectures capable of supporting millions of concurrent workloads while maintaining operational efficiency.

Purchasing decisions within this segment emphasize compute density, workload scalability, remote management, energy consumption, interoperability with networking infrastructure, and long-term platform consistency. Cloud operators also evaluate processor roadmap availability, firmware lifecycle support, hardware reliability, automation capabilities, and maintenance efficiency before making large-scale procurement commitments.

Competition within this segment extends beyond server performance. Vendors compete through integrated infrastructure portfolios, management software, deployment automation, supply assurance, global technical support, and strategic customer relationships. Procurement contracts frequently include consulting services, implementation assistance, maintenance agreements, and long-term infrastructure planning. As cloud providers continue expanding regional data center footprints, this segment is expected to remain an important contributor to industry revenues and technology adoption.

Regional Analysis

North America maintains a strong position due to extensive hyperscale data center investment, widespread enterprise cloud adoption, and sustained spending by financial institutions, healthcare providers, government agencies, and technology companies. Procurement decisions emphasize infrastructure resilience, cybersecurity compliance, energy efficiency, and operational automation. Mature digital infrastructure supports ongoing hardware refresh cycles despite relatively slower expansion compared with emerging markets.

Europe demonstrates stable demand supported by enterprise modernization, industrial digitalization, public sector computing investments, and expanding colocation services. Data protection requirements, sustainability policies, and energy efficiency regulations influence infrastructure procurement. Organizations increasingly prioritize servers capable of reducing power consumption while supporting secure hybrid cloud deployments.

Asia Pacific represents the largest long-term infrastructure opportunity as governments and private investors expand domestic cloud capacity and enterprise digital infrastructure. China, India, Japan, South Korea, Taiwan, and Southeast Asian economies continue investing in new data centers supporting manufacturing, telecommunications, e-commerce, financial services, and public administration. Rising internet usage, enterprise software adoption, and national digital economy initiatives support sustained infrastructure procurement.

Middle East and Africa continues expanding through government-led digital economy strategies, smart city initiatives, financial sector modernization, and regional cloud infrastructure investment. Demand is concentrated within Gulf Cooperation Council countries and Israel, where enterprise modernization and sovereign cloud initiatives encourage deployment of advanced computing infrastructure. Budget constraints and skilled workforce availability remain important implementation considerations across several markets.

South America experiences gradual demand expansion driven by financial services, telecommunications providers, retail digitalization, and enterprise cloud migration. Brazil represents the largest regional market because of its sizeable enterprise base and expanding colocation sector. Economic volatility, import costs, and infrastructure investment cycles continue influencing procurement timing across the region.

Competitive Landscape

Competition within the data center blade server market is characterized by established global infrastructure vendors offering integrated computing platforms rather than standalone hardware products. Hewlett Packard Enterprise Development LP, Dell Technologies Inc., Cisco Systems, Inc., Lenovo Group Limited, Super Micro Computer, Inc., Fujitsu Limited, Hitachi Vantara LLC, Oracle Corporation, NEC Corporation, and Inspur Electronic Information Industry Co., Ltd. compete through platform performance, infrastructure integration, enterprise software compatibility, lifecycle services, and global support capabilities.

Product differentiation increasingly depends on processor compatibility, chassis scalability, integrated networking, infrastructure automation, firmware security, workload optimization, and management software. Vendors continue strengthening strategic partnerships with processor manufacturers, virtualization software providers, cloud platform companies, and systems integrators to improve deployment flexibility across hybrid infrastructure environments.

Geographic expansion also influences competitive positioning. Suppliers invest in regional service centers, technical support capabilities, partner ecosystems, and local integration expertise to address enterprise modernization projects. Long-term customer relationships, consulting capabilities, and infrastructure lifecycle services have become important competitive factors alongside hardware innovation.

Recent Developments

June 2026: Supermicro expanded its AI infrastructure portfolio with the AMD Helios rack-scale platform, enabling rapid deployment of high-density data center systems and accelerating large-scale AI training and inference through scalable rack-level architecture.

June 2026: Hewlett Packard Enterprise (HPE) introduced the HPE ProLiant Compute DL394 Gen12 server powered by the NVIDIA Vera CPU, expanding its enterprise compute portfolio with a platform engineered for agentic AI, high-performance data processing, and modern data center environments.

May 2026: Dell Technologies announced expanded infrastructure solutions integrating next-generation server platforms with advanced management software designed for AI and hybrid cloud environments. The development supports enterprise workload consolidation and operational efficiency.

April 2026: Supermicro introduced its Gold Series Enterprise Server Solutions, featuring over 25 pre-configured server platforms for enterprise AI, compute, storage, and edge deployments, enabling faster deployment and reduced time-to-online for data center operators.

February 2026: Supermicro launched its MicroBlade® platform powered by AMD EPYC™ 4005 Series processors, introducing a high-density blade server architecture supporting up to 40 server nodes in a 6U enclosure for cloud, edge, cybersecurity, and SaaS workloads.

Regulatory and Policy Environment

The market operates within a regulatory framework covering cybersecurity, energy efficiency, environmental sustainability, data protection, and product safety. Government procurement standards increasingly require compliance with internationally recognized information security frameworks and supply chain assurance practices. Public sector purchasing frequently includes requirements for secure firmware management, trusted hardware components, and infrastructure resilience.

Energy efficiency policies influence procurement decisions across many regions as operators seek to reduce electricity consumption and carbon emissions. Data center operators increasingly evaluate infrastructure according to power utilization effectiveness (PUE), equipment efficiency, and lifecycle sustainability. Environmental regulations governing electronic waste management and hazardous substances also affect product design, recycling practices, and component sourcing.

International standards developed by organizations including ISO and the International Electrotechnical Commission (IEC) continue supporting interoperability, safety, quality management, and information security across enterprise computing infrastructure. Compliance with these standards improves buyer confidence and facilitates deployment across regulated industries.

Outlook and Strategic Implications

Over the forecast period, procurement activity is expected to concentrate on infrastructure capable of supporting hybrid cloud operations, artificial intelligence workloads, virtualization, and high-density enterprise computing. Buyers will continue prioritizing modularity, operational efficiency, infrastructure automation, and lifecycle cost optimization rather than hardware specifications alone.

Investment strategies are expected to emphasize modernization of aging enterprise infrastructure, expansion of hyperscale computing capacity, and integration of intelligent management software. Vendors able to combine compute platforms with networking, storage, software-defined management, and long-term service capabilities will strengthen competitive positioning as procurement becomes increasingly solution-oriented.

Risks include supply chain disruptions, component pricing volatility, evolving cybersecurity requirements, and competition from alternative infrastructure architectures. Nevertheless, sustained enterprise investment in digital infrastructure, cloud services, and data-intensive applications is expected to support continued demand for blade server platforms that deliver scalable, centrally managed, and efficient computing environments over the next five years.

Data Center Blade Server Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 23.22 billion |

| Total Market Size in 2031 | USD 35.56 billion |

| Forecast Unit | Billion |

| Growth Rate | 8.90% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Application, End-User, Geography |

| Companies |

|

Market Segmentation

By Application

- Virtualization

- High-Performance Computing (HPC)

- Database Management

- Enterprise Applications

- Cloud Computing

By End-User

- Cloud Service Providers

- Colocation Providers

- Enterprises

- Government

- BFSI

By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- Germany

- France

- United Kingdom

- Spain

- Others

- Middle East and Africa

- Saudi Arabia

- Israel

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Taiwan

- Thailand

- Indonesia

- Others

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

1.8. Key Benefits to the Stakeholder

2. RESEARCH METHODOLOGY

2.1. Research Design

2.2. Research Processes

3. EXECUTIVE SUMMARY

3.1. Key Findings

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Porter's Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of New Entrants

4.3.4. Threat of Substitutes

4.3.5. Competitive Rivalry in the Industry

4.4. Industry Value Chain Analysis

4.5. Analyst View

5. DATA CENTRE BLADE SERVER MARKET BY APPLICATION

5.1. Introduction

5.2. Virtualization

5.3. High-Performance Computing (HPC)

5.4. Database Management

5.5. Enterprise Applications

5.6. Cloud Computing

6. DATA CENTRE BLADE SERVER MARKET BY END-USER

6.1. Introduction

6.2. Cloud Service Providers

6.3. Colocation Providers

6.4. Enterprises

6.5. Government

6.6. BFSI

7. DATA CENTRE BLADE SERVER MARKET BY GEOGRAPHY

7.1. Introduction

7.2. North America

7.2.1. By Application

7.2.2. By End-User

7.2.3. By Country

7.2.3.1. United States

7.2.3.2. Canada

7.2.3.3. Mexico

7.3. South America

7.3.1. By Application

7.3.2. By End-User

7.3.3. By Country

7.3.3.1. Brazil

7.3.3.2. Argentina

7.3.3.3. Others

7.4. Europe

7.4.1. By Application

7.4.2. By End-User

7.4.3. By Country

7.4.3.1. Germany

7.4.3.2. France

7.4.3.3. United Kingdom

7.4.3.4. Spain

7.4.3.5. Others

7.5. Middle East and Africa

7.5.1. By Application

7.5.2. By End-User

7.5.3. By Country

7.5.3.1. Saudi Arabia

7.5.3.2. Israel

7.5.3.3. Others

7.6. Asia Pacific

7.6.1. By Application

7.6.2. By End-User

7.6.3. By Country

7.6.3.1. China

7.6.3.2. Japan

7.6.3.3. India

7.6.3.4. South Korea

7.6.3.5. Taiwan

7.6.3.6. Thailand

7.6.3.7. Indonesia

7.6.3.8. Others

8. COMPETITIVE ENVIRONMENT AND ANALYSIS

8.1. Major Players and Strategy Analysis

8.2. Market Share Analysis

8.3. Mergers, Acquisitions, Agreements, and Collaborations

8.4. Competitive Dashboard

9. COMPANY PROFILES

9.1. Hewlett Packard Enterprise Development LP

9.2. Dell Technologies Inc.

9.3. Cisco Systems, Inc.

9.4. Lenovo Group Limited

9.5. Super Micro Computer, Inc.

9.6. Fujitsu Limited

9.7. Hitachi Vantara LLC

9.8. Oracle Corporation

9.9. NEC Corporation

9.10. Inspur Electronic Information Industry Co., Ltd.

Navigate

Trusted by the world's leading organizations