Strategic Petroleum Reserve (SPR) Utilization Trends: Global Capacity, Deployment Patterns, and Market Implications (2026)

Strategic Petroleum Reserves have evolved into active tools for stabilizing oil markets, addressing geopolitical disruptions, and managing inflation, though rising utilization, declining reserves, and replenishment challenges highlight the need for coordinated policies and sustained investment.

1. Introduction

The Strategic Petroleum Reserves (SPRs) are among the most important blocks of energy security globally. They protect economies in case of an abrupt shortage of crude oil. The need for these reserves was experienced because of the energy crises of the 1970s, where the countries that import oil experienced allowed them to realize their helplessness. The nature and objectives of SPRs have changed drastically since then.

The table below shows SPR Sites and their volumes:

Crude Oil Inventory by Site (as of March 18, 2026)

SPR Site | Sweet Volume | Sour Volume | Combined Volume | Total Number of Caverns |

|---|---|---|---|---|

Bayou Choctaw | 13 MMB | 40 MMB | 53 MMB | 6 |

Big Hill | 28 MMB | 62 MMB | 90 MMB | 14 |

Bryan Mound | 66 MMB | 119 MMB | 185 MMB | 19 |

West Hackberry | 48 MMB | 40 MMB | 88 MMB | 22 |

Total | 155 MMB | 261 MMB | 416 MMB | 61 |

By the close of CY 2025 (31 December 2025), the SPR crude oil stock was 411 MMbbl. The original use of SPRs was in their first generation, as emergency stocks to be used in case of a major supply disruption.

However, in the era of energy, that role has changed a lot. Governments have turned to SPRs as a political instrument in influencing oil markets in order to stabilize domestic fuel prices and to control inflation. Increased market volatility and geopolitical tensions, coupled with the growing interdependency of worldwide energy supplies, have helped to force this change. As of 2026, the world has piled up colossal global stocks of strategic petroleum, both those controlled by the government and those required by law in industry inventories.

Not only the strategic reserves but the global oil inventory, which consists of commercial storage as well, is more than 8.2 billion barrels, indicating investments in storage infrastructure as well as ‘precautionary stockpiling’. The buildup clearly showcases the immense importance being attached to energy security by developed and emerging countries. The recent geopolitical events have actually demonstrated the extent to which these reserves can be strategic. When supply routes to the West were in danger, as in the case of the Strait of Hormuz, that supply hazard was so severe as to motivate the significant importers to unite and act over it.

2. Historical Evolution of SPR Systems

The idea of strategic petroleum reserves appeared as a result of the oil embargo in 1973 that led to acute shortages of supplies and economic havoc in the countries that imported oil. Countries responded to this by building national reserves so that they could be less susceptible to external shocks.

The SPR systems have experienced several phases of development over time:

1970s–1980s: Establishment phase, focused on building storage infrastructure and accumulating reserves.

1990s–2000s: Stabilization, which involved reserves maintenance and minimal use in case of conflicts within the region.

Post-2010: Growth stage, because of the growing energy needs in the emerging economies and the growing geopolitical insecurity.

Post-2020: Active utilization phase, marked by frequent releases and integration with broader economic policy objectives.

This historical progression reflects a shift from passive storage to active market intervention, fundamentally redefining the role of SPRs in global energy systems.

3. Regional SPR Utilization Patterns

Strategic Petroleum Reserves by Country

Country | Estimated Strategic Reserves | Type of Reserves | Key Notes |

|---|---|---|---|

United States | ~400+ million barrels (current levels; capacity ~700+ million) | Government-controlled | Largest publicly reported SPR globally; created after 1975 oil crisis |

Japan | ~260 million barrels | Government + private | Among the largest reserves; exceeds IEA requirements |

China | ~500–600 million barrels (SPR only; higher incl. commercial) | Government + commercial | Rapidly expanding; hybrid storage model |

South Korea | ~146 million barrels | Public + private | Highly integrated system |

India | ~35–40 million barrels (approx) | Government-controlled | Expanding capacity in phases |

Germany | ~200+ million barrels (incl. industry stocks) | Industry obligation | Part of EU mandated system |

United Kingdom | ~100+ million barrels (approx, incl. industry stocks) | Industry obligation | No centralized SPR; relies on companies |

France | ~100+ million barrels | Industry + government mix | Strong compliance with EU norms |

IEA Total | ~1.2 billion barrels (public) + ~600 million barrels (industry) | Combined | Collective emergency reserves across member countries |

3.1 North America

North America, especially the United States, has the best and most advanced infrastructure of SPR globally. Its capacity to discharge vast amounts of crude oil in a short period of time renders it an important pillar of energy security in the world.

In 2025, the United States had an average import of approximately 490,000 barrels per day of crude oil in the Middle East Gulf region, comprising Bahrain, Iraq, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates. These imports are predominantly of medium sour crude and are usually delivered to refineries on the U.S. Gulf Coast and West Coast.

The U.S. Strategic Petroleum Reserve is developed to store crude oil and release it to the domestic refineries in the case of a disruption in the market. The SPR has been purchasing two crude types since 2024: sweet (low sulfur) and sour (high sulfur), with medium API gravity. The majority of the SPR oil is shipped to the Gulf Coast refineries, but with temporary waivers under the Jones Act, refineries located on the West Coast can be served when transportation is required.

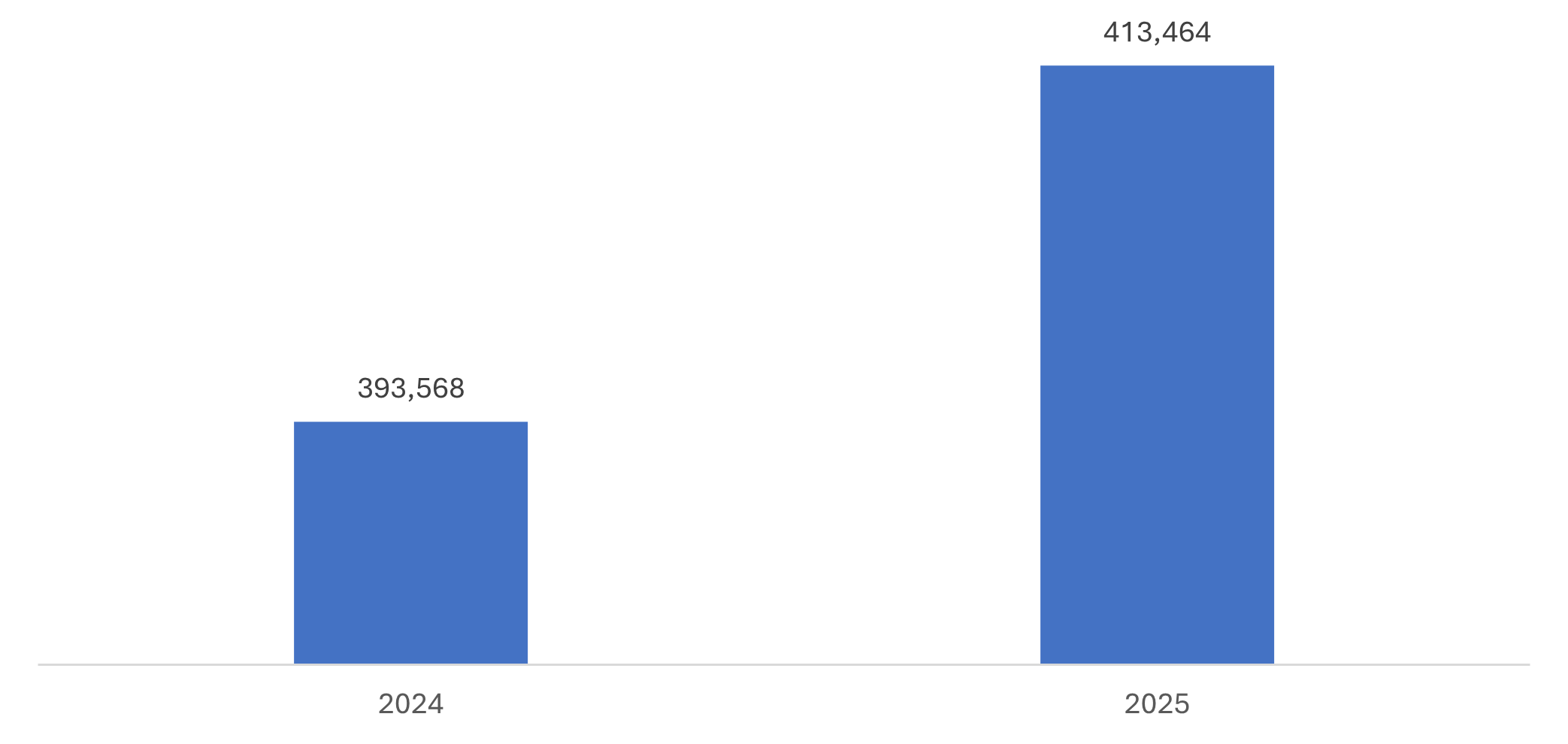

United States Crude Oil and Petroleum, Strategic Petroleum Reserve, Thousand Barrels, 2024-2025

Moreover, its extensive use has decreased the level of reserves, which is why it is necessary to develop effective replenishment strategies that would help to preserve resilience in the long-term perspective.

3.2 Asia-Pacific

The Asia-Pacific region is experiencing a high rate of increase in the SPR capacity due to increased emphasis on energy security. This change can be noted by the massive investments by China and the continuous expansion initiatives by India. Key state-owned enterprises such as Sinopec and CNOOC are intending to increase storage capacity by at least 169 million barrels (11 locations) by 2025-2026, of which approximately 37 million barrels have already been accomplished.

China is especially hastening the pace of its reserve complexes development as a larger part of a wider drive to accumulate crude reserves, which took on urgency with the Russian invasion of Ukraine. In the future, the region is likely to be at the center of global capacity growth, with the increase in energy demand and geopolitical factors. Strategic reserves in India are primarily kept in underground systems in Visakhapatnam, Mangalore, and Padur (Karnataka) with a total capacity of 5.33 million metric tonnes of crude oil, which are operated by Indian Strategic Petroleum Reserve Limited (ISPRL).

3.3 Europe

Europe adopts a decentralized model in the management of its strategic reserves with regulatory provisions that stipulate minimum levels of stock in member states. This guarantees a minimum level of preparedness in case of disruption of supplies. For example, in March 2026, Germany agreed to release approximately 2.5 million tonnes of oil in its strategic stocks under a larger initiative organized by the International Energy Agency (IEA) to relieve the pressure on prices associated with the tension in Iran and the Persian Gulf region in general. Germany would therefore do its part and respond to a request by the IEA for countries around the world to release a total of 400 million barrels from their reserves.

The SPR Petroleum Account, which is used to purchase oil for the reserve, received approximately $17 billion from emergency oil sales in response to market conditions related to Russia's invasion of Ukraine in 2022.

The European Commission for Energy has previously shown some support for the idea of European strategic gas reserves, as this provides the bloc with stable and predictable supplies. The current Commissioner for Energy, Kadri Simson, has pondered the idea of EU strategic gas reserves, and a decision regarding its approval was made in the first half of 2022.

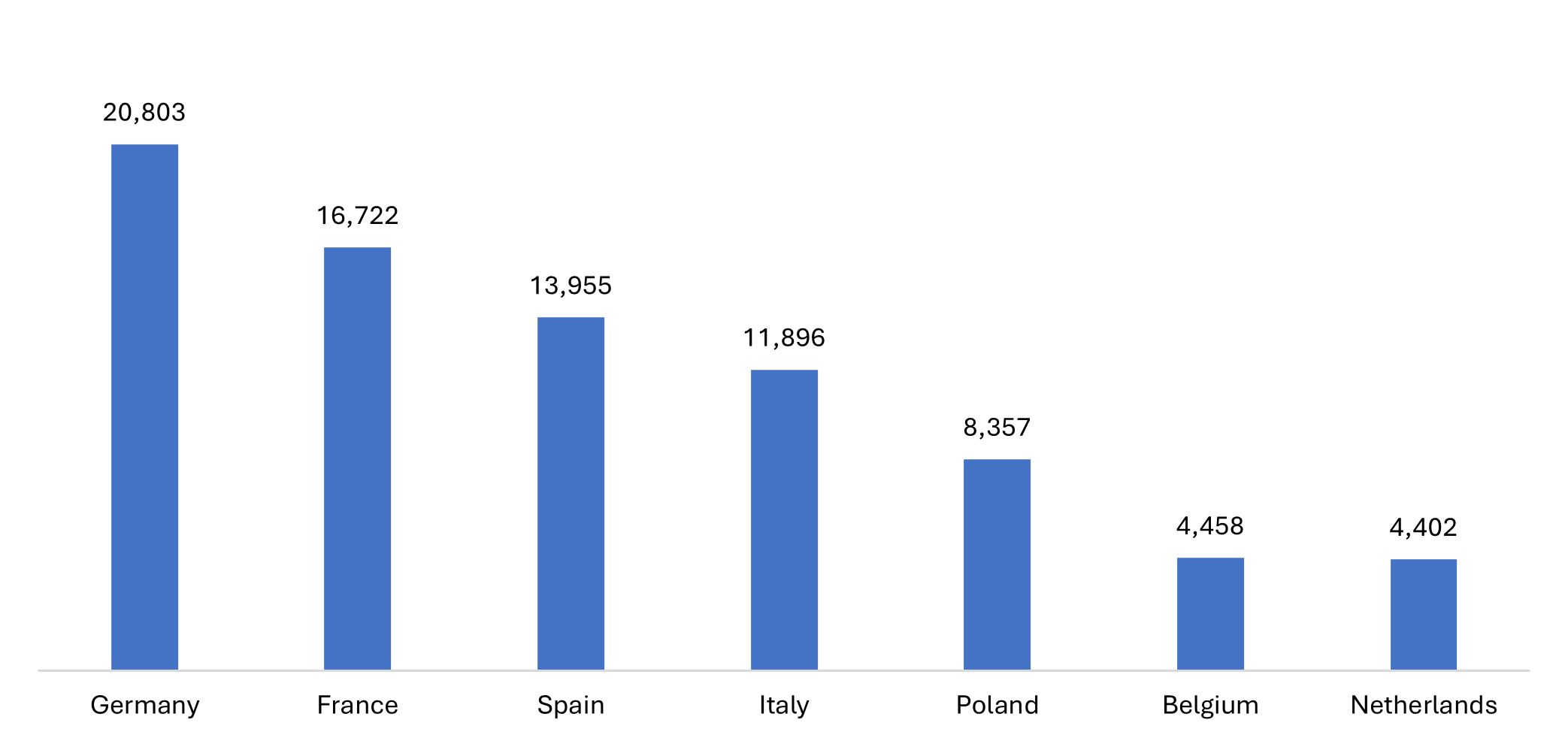

In May 2025, the EU held 108.6 million tonnes of emergency oil stocks, an increase of +7.3% from June 2022, which recorded a historical low of 101.1 million tonnes.

Top EU countries and their emergency oil stocks, in 1000 Tonnes, May 2025

However, while this system provides stability, it can limit flexibility in responding to rapidly changing market conditions.

3.4 Middle East & Africa

The Middle East & Africa region plays a very different role in the global oil landscape. Unlike major consuming regions, it is primarily a key oil-producing hub and does not rely heavily on large-scale strategic reserves. Countries such as Saudi Arabia and the United Arab Emirates maintain substantial production capacity, including spare output, which often serves as a practical alternative to holding extensive reserves.

In response to market disruptions caused by conflict in the Middle East, all 32 member countries of the International Energy Agency (IEA) agreed to release a combined 400 million barrels of oil from their emergency reserves to stabilize global markets. However, many countries within the Middle East and Africa do not maintain large strategic petroleum reserves, as their energy security is largely supported by strong domestic production and the flexibility to adjust exports.

Some nations in the region are gradually investing in storage infrastructure to strengthen resilience against geopolitical uncertainty and market volatility. In times of global supply disruption, the region’s importance lies less in releasing stored oil and more in its ability to quickly adjust production levels. At the same time, ongoing geopolitical tensions, especially around key transit routes, continue to pose significant risks to global oil flows.

3.5 South America

South America has a relatively limited presence in global SPR systems, with most countries lacking large-scale strategic reserves comparable to those in North America, Europe, or Asia-Pacific. Countries such as Brazil and Argentina rely more on domestic production and commercial inventories rather than dedicated government-controlled reserves.

In March 2026, Brazilian President Lula da Silva called for the establishment of a strategic petroleum reserve to protect the economy from global price shocks, particularly due to rising Middle East tensions. While Brazil holds large proven oil reserves (16.8 billion barrels as of 2024), it currently lacks a formal government-managed strategic reserve.

The region’s energy security strategy is largely influenced by resource availability and domestic production capabilities, reducing the immediate need for extensive SPR infrastructure. However, fluctuations in production levels, economic instability, and infrastructure constraints can impact supply reliability.

While South America does not play a major role in coordinated SPR releases, its production capacity contributes to global supply dynamics, particularly during periods of market imbalance.

4. Utilization Trends: Increasing Frequency and Strategic Deployment

4.1 Record-Breaking Coordinated Releases

The growing frequency and scale of SPR use mark a significant shift in global energy policy. In 2026, a coordinated release of around 400 million barrels was carried out, the largest of its kind in history. This move was triggered by disruptions to key oil supply routes, highlighting how vulnerable global energy systems remain to geopolitical events.

At the same time, it showed how effective international coordination can be in managing supply risks. The United States contributed a substantial share of the total release, reinforcing its leading role in global energy security, while other countries also participated actively, reflecting a collective effort to stabilize the market.

4.2 Transition from Emergency Use to Market Stabilization

Over time, the role of SPRs has expanded beyond purely emergency use. Governments now rely on these reserves as tools to manage broader economic challenges, including price volatility, inflation, and domestic fuel market stability. This reflects a more proactive approach to energy management, where SPRs are used not just in response to crises but also to prevent potential disruptions.

Decisions around their use are increasingly influenced by market conditions such as price trends and supply expectations.

4.3 Declining Reserve Levels and Refill Challenges

Despite increased usage, replenishing reserves has become more difficult. High oil prices have made it expensive for countries to rebuild their stockpiles, delaying refill efforts in several cases. In the United States, reserve levels have dropped significantly from past highs, raising concerns about long-term energy security. Restoring these levels will require sustained investment and careful planning. Emerging economies face additional hurdles, including limited infrastructure and financial constraints, which can restrict their ability to expand and maintain reserves.

5. Policy and Regulatory Frameworks

Government policy plays a central role in shaping how SPRs are managed and used. IEA member countries are required to maintain reserves equivalent to at least 90 days of net imports, ensuring a basic level of energy security.

National policies determine when and how these reserves are deployed, influencing both the timing and scale of releases. Greater coordination between countries has improved the effectiveness of global responses to supply disruptions. At the same time, governments are introducing more flexible frameworks to enable quicker decision-making during crises.

6. SPR Utilization Efficiency and Constraints

6.1 Operational Constraints

Several operational factors can affect how efficiently SPRs are used, including withdrawal rates, infrastructure capacity, and transportation logistics. These challenges can slow down the delivery of released oil, reducing the immediate impact of such interventions.

6.2 Market Impact Limitations

While SPR releases are effective in addressing short-term supply disruptions, their influence on long-term market trends is limited. Oil prices continue to be shaped by broader factors such as geopolitical developments, production decisions, and shifts in demand. These trends are also heavily influenced by ongoing risks in key oil-producing regions.

7. Geopolitical Risk Scenario: Impact of a U.S.–Iran Conflict on SPR Utilization

The military conflict between the United States and Iran represents one of the most significant geopolitical risks to global oil markets. Given Iran’s role as a major oil producer and its strategic location near critical supply routes, such a conflict would have immediate and far-reaching implications for supply stability, pricing, and reserve utilization.

One of the primary risks arises from potential disruptions to the oil supply. Iran produces approximately 3–4 million barrels per day, and any conflict could significantly reduce or halt its exports due to sanctions, infrastructure damage, or military blockades. In addition, an average of 20 million barrels per day of crude oil and oil products transited the Strait of Hormuz in 2025, or around 25% of the world’s seaborne oil trade. Any restriction in this route severely impacts global oil flows and creates immediate supply shortages.

In such a scenario, oil prices would likely experience sharp increases driven by both actual supply constraints and market speculation. Even the anticipation of conflict can trigger volatility, as traders factor in risk premiums. A full-scale disruption could push prices significantly higher, affecting both crude and refined product markets globally.

Strategic Petroleum Reserves would play a critical role in mitigating the immediate impact of such disruptions. Major economies, including the United States, European countries, and key Asian importers, would likely initiate coordinated SPR releases to stabilize supply and manage price spikes. These releases would help offset short-term shortages and maintain market confidence.

The U.S. Department of Energy (DOE) announced that contracts have been awarded for the acquisition of approximately one million barrels of crude oil for the Strategic Petroleum Reserve (SPR). The contracts awarded on November 12, 2025, are for deliveries beginning in December 2025 through January 2026 to the Bryan Mound site. This announcement follows the Request for Proposal (RFP) that was announced on October 21, 2025.

However, the effectiveness of SPR releases in such a scenario would be limited by several factors. The scale of potential disruption, particularly if shipping routes are affected, may exceed the capacity of reserves to fully stabilize the market. Additionally, logistical challenges such as transportation delays and refining compatibility could reduce the immediate impact of released oil.

The economic implications of such a conflict would extend beyond the energy sector. Higher oil prices would contribute to inflationary pressures, increase transportation and production costs, and affect global trade balances. Import-dependent economies would face significant challenges, including rising import bills and currency pressures.

Overall, a U.S.–Iran conflict would reinforce the importance of maintaining adequate SPR levels and highlight the need for coordinated international response mechanisms. It would also accelerate efforts to diversify energy sources and reduce dependence on geopolitically sensitive regions.

Volume of crude oil and petroleum liquids transported through world chokepoints and the Cape of Good Hope, 2023–2024

Location | 2023 | 2024 |

Strait of Malacca | 24.0 | 23.2 |

Strait of Hormuz | 20.7 | 20.9 |

Suez Canal and SUMED Pipeline | 4.8 | 4.9 |

Bab el-Mandeb | 4.1 | 4.2 |

Danish Straits | 4.9 | 4.9 |

Turkish Straits (Dardanelles) | 3.6 | 3.7 |

Panama Canalb | 2.0 | 2.3 |

Cape of Good Hope | 9.3 | 9.1 |

8. Replenishment Strategies and Economic Considerations

Replenishing SPRs is a complex process shaped by market conditions, government policies, and logistical constraints. Governments need to carefully balance the urgency of rebuilding reserves with the cost of purchasing oil at current market prices.

To manage this, some countries are adopting phased replenishment strategies, buying oil when prices are lower to reduce costs, while others are exploring alternatives such as long-term supply agreements and swap deals. These decisions carry significant economic implications, as large-scale purchases can influence global oil prices and overall market dynamics.

9. Emerging Trends in SPR Strategy

Greater integration between strategic reserves and commercial storage systems

Increased use of financial tools, such as loan-based release mechanisms

Wider adoption of technology for monitoring, management, and optimization

Closer alignment with broader energy transition and sustainability goals

10. Future Outlook

The role of SPRs is expected to keep evolving as global energy systems move toward greater sustainability. While oil will remain an important energy source in the near term, the significance of strategic reserves may gradually shift as alternative energy sources become more prominent.

Going forward, countries are likely to focus on improving efficiency, expanding storage capacity, and strengthening coordination mechanisms. Advances in technology, along with the development of alternative energy storage solutions, will play an increasingly important role in shaping how SPR systems function in the future.

11. Conclusion

Strategic Petroleum Reserves have become essential tools for managing risks in an increasingly complex global energy landscape. Their growing use reflects not only rising market uncertainty but also the need for more proactive and flexible energy management strategies. Although challenges such as declining reserve levels and difficulties in replenishment remain, continued investment and policy improvements are expected to enhance the effectiveness of these systems. Ultimately, maintaining the right balance between utilization, replenishment, and capacity expansion will be key to ensuring long-term energy security in an unpredictable global environment.

Get in Touch

Interested in this topic? Contact our analysts for more details.

Related Insights

How AI and Smart Sensors Are Revolutionizing EV Battery Cooling in India

Jul 23, 2026

Top Companies Shaping India's Electric Vehicle Drivetrain Market

Jul 22, 2026

Top 10 Generative AI Companies in 2026: Products, Pricing, Funding, and Competitive Analysis

Jul 21, 2026

How At-Home Diagnostic Kits Are Transforming Healthcare in the U.S.

Jul 21, 2026

The Rise of Advanced Battery Technologies in India's Electric Vehicle Market

Jul 20, 2026