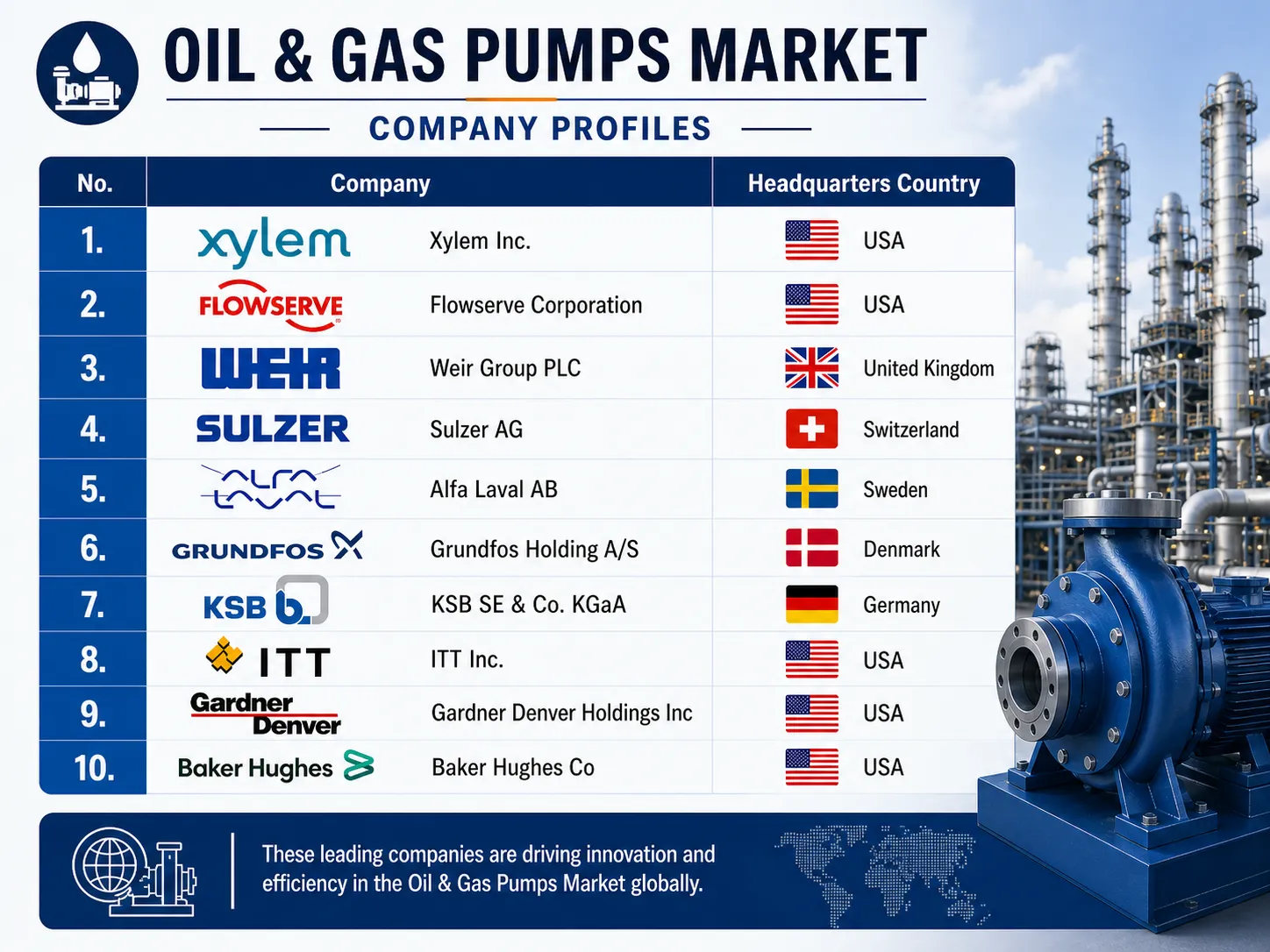

Top 10 Companies Driving Innovation in Oil and Gas Pumping Systems

The gas pump market is transforming into a high-tech, efficiency-driven sector integrating digital intelligence, advanced materials, and sustainability goals. Driven by decarbonization, extreme-environment demands, and energy transition needs, pumps are evolving into smart systems, enabling precision fluid management, reduced emissions, and resilient operations across increasingly complex and high-risk energy infrastructures.

The global energy landscape is currently experiencing a significant and understated transformation. While public discussions often focus on the "end of oil" or the rapid growth of renewable energy, the essential processes of moving fluids, such as hydrocarbons, produced water, and liquefied gases, remain crucial for industrial stability worldwide. The oil and gas pump market, which was valued at USD 9.7 billion in 2026, is projected to reach USD 13.5 billion by 2031, growing at a CAGR of 6.8%.

This market is no longer solely about physical strength and traditional equipment. It has evolved into a sophisticated field incorporating computational fluid dynamics, material science, and edge computing. In this context, a "pump" is shifting from being a standalone piece of machinery to an intelligent, networked component within a digital twin ecosystem. As reservoirs grow more complex, featuring higher pressures, deeper waters, and more corrosive materials, the margin for mechanical failure has virtually disappeared. This change is not just about moving fluids; it focuses on precision, energy efficiency, and significantly reducing methane emissions and operational downtime.

The industry is currently defined by three tectonic shifts: decarbonization of the extraction process, the "digitalization of the wet end," and the push for extreme-environment resilience. We are seeing a move away from traditional oversized pumping systems toward right-sized, variable-speed driven (VSD) solutions that drastically lower the carbon intensity of every barrel produced. Furthermore, as the industry pivots toward Carbon Capture and Storage (CCS), the demand for specialized CO2 injection pumps is creating a secondary market that bridges the gap between fossil fuels and climate goals.

The Strategic Value Chain: Beyond Simple Displacement

To understand the pumping sector, one must view it as the circulatory system of the global economy. In the upstream segment, pumps are the primary drivers of artificial lift, essential for maintaining production as reservoir pressures naturally decline. In the midstream, they are the literal engines of the pipeline networks that traverse continents. Downstream, in the refining and petrochemical stage, pumps handle the volatile, high-temperature chemistry required to turn crude into high-value polymers and fuels.

The value chain begins with metallurgical innovation, developing alloys that can withstand the abrasive nature of fracking fluids or the cryogenic temperatures of LNG. It then moves into the integration phase, where mechanical seals and bearings are paired with sensors to monitor vibration and heat in real-time. The criticality of this equipment cannot be overstated; a single pump failure on an offshore platform can result in millions of dollars in lost revenue and potential environmental catastrophes. Consequently, the industry is moving toward "Pumps-as-a-Service" models, where manufacturers are not just selling a machine, but guaranteeing uptime through predictive maintenance and remote monitoring. This shift moves the industry from a CAPEX-heavy model to an OPEX-optimized framework, making the pump manufacturer a long-term strategic partner rather than a mere vendor.

1. Xylem Inc.

Xylem has successfully pivoted from being a water-centric entity to a powerhouse in the oil and gas sector, primarily by leveraging its expertise in "produced water" management. As unconventional oil extraction (fracking) continues to dominate the North American landscape, the volume of water that needs to be moved, treated, and reinjected has skyrocketed. Xylem doesn’t just sell a pump; they sell a water cycle solution. Their strategic distinction lies in their ability to integrate smart analytics, what they call "Decision Intelligence", into the pumping process. By using advanced sensors to detect cavitation before it happens, Xylem reduces the total cost of ownership for operators who are often working on razor-thin margins in the shale plays. Their focus on modularity allows for rapid deployment in remote fields, a critical advantage in the fast-paced Permian Basin.

Product | Developments | Country |

Flygt 3000 Series and Godwin Dri-Prime | Integration of "SmartRun" intelligence for autonomous clog detection and energy optimization in midstream operations (2024-2025). | USA |

2. Flowserve Corporation

Flowserve is the incumbent heavyweight that has embraced the energy transition with surprising agility. While they maintain a massive installed base of traditional centrifugal and positive displacement pumps, their recent strategic focus has shifted toward high-energy recovery and CCS applications. They are currently leading the charge in developing pumps that can handle supercritical CO2, which is notoriously difficult to pump due to its phase-change characteristics. Flowserve’s RedRaven platform represents the gold standard in IoT-enabled asset management, allowing operators to visualize the health of their fleet globally. Their strength lies in their massive global service network; in an industry where parts availability is a bottleneck, Flowserve’s regional Quick Response Centers (QRCs) provide a moat that smaller competitors struggle to cross.

Product | Developments | Country |

VTP and CHTA Multistage Pumps | Launch of specialized supercritical CO2 injection pumps for large-scale carbon capture projects. | USA |

3. Weir Group PLC

The Weir Group has undergone a radical transformation, divesting its oil and gas division to focus more on mining, yet they remain a vital innovator in the high-pressure pumping space through its remaining engineering synergies and specialized fluid end technologies. Their focus is on "extreme durability." In the pumping world, Weir is synonymous with the ability to handle the most abrasive slurries and high-pressure fracking environments. Their innovation is currently focused on material science, developing proprietary coatings that extend the life of pump components by 3x or 4x compared to standard stainless steel. For an operator, this means fewer "trips" to replace equipment, which is the single biggest factor in operational safety and cost-efficiency in high-pressure environments.

Product | Developments | Country |

SPM® QEM 3000 Frac Pump | Introduction of "Endurance" fluid ends designed to handle high-concentration proppants with minimal erosion. | UK |

4. Sulzer AG

Sulzer is the "specialist’s specialist." When an operator has a problem that a standard pump cannot solve, such as ultra-deepwater subsea injection, they turn to Sulzer. The company has carved out a niche in the subsea segment, where pumps must operate autonomously on the ocean floor for years without maintenance. Sulzer’s innovation in multiphase pumping, including moving oil, gas, and water simultaneously through a single unit, is a game-changer for marginal field development. It eliminates the need for expensive topside separation equipment. Their recent move toward more sustainable manufacturing processes and the development of pumps specifically for the hydrogen economy show they are looking well beyond the current oil cycle.

Product | Developments | Country |

HPcp (Barrel Pumps) | Commercialization of high-speed subsea multiphase boosting systems for deepwater Brazil and Gulf of Mexico fields. | Switzerland |

5. Alfa Laval AB

Alfa Laval occupies a unique space, sitting at the intersection of heat transfer, separation, and fluid handling. In the oil and gas sector, they are the masters of the downstream and midstream processing phases. Their pumping solutions are often integrated into larger modules, such as their Framo submerged pumping systems, which are the industry standard for cargo pumping on tankers and FPSOs (Floating Production Storage and Offloading). Alfa Laval’s strategic edge is its "total system" approach. They don't just look at the pump; they look at how the pump interacts with the heat exchanger and the separator. Their recent innovations focus on the "green tanker" concept, reducing the energy required for cargo discharge and ballast water management.

Product | Developments | Country |

Framo Submerged Pumps | Upgrade of the Framo hydraulic power units to include electric-drive options, reducing fuel consumption during offloading. | Sweden |

6. Grundfos Holding A/S

Grundfos is often associated with commercial buildings, but its "iSolutions" philosophy is making significant inroads into the oil and gas sector, particularly in chemical dosing and utility water management. Their pumps are perhaps the most digitally "native" in the industry. Grundfos has perfected the integrated frequency converter, enabling its pumps to adjust to flow requirements with millisecond precision. In refinery applications, where precise chemical dosing is crucial to prevent corrosion, Grundfos’s digital dosing pumps provide a level of accuracy that traditional mechanical pumps cannot achieve. They are driving the industry towards a "zero-leakage" future through advanced magnetic drive technologies.

Product | Developments | Country |

CR Range (Multistage) | Launch of the "CUE" series high-pressure pumps with integrated AI for autonomous pressure management in refinery utility systems. | Denmark |

7. KSB SE & Co. KGaA

KSB represents the pinnacle of German engineering in the pumping world. They are particularly strong in the power generation and refining sectors of the oil and gas value chain. Their pumps are known for their massive scale and reliability in high-temperature settings. KSB has been a leader in the "Additive Manufacturing" (3D printing) of spare parts. This is a critical innovation for the oil and gas industry; rather than waiting months for a cast part to arrive at a remote refinery, KSB can provide the digital blueprints for local 3D printing of impellers and casings. This dramatically reduces the "dead capital" operators hold in spare parts inventory.

Product | Developments | Country |

CHTR Multistage Pumps | Implementation of 3D-printed "optimized hydraulics" impellers for custom refinery retrofit projects to increase efficiency. | Germany |

8. ITT Inc.

Through its Goulds Pumps brand, ITT is a staple of the North American downstream sector. They have built a reputation on the "i-ALERT" monitoring system, which was one of the first successful forays into Bluetooth-enabled pump health tracking. ITT’s strategic focus is on the "harsh environment" niche, handling liquids that are chemically aggressive, high-temperature, or laden with solids. Their recent development focus has been on the "API 610" standard (the rigorous industry standard for refinery pumps), pushing the boundaries of what a centrifugal pump can handle without failing. They are increasingly focused on modular "skid" solutions that can be dropped into a facility with minimal on-site engineering.

Product | Developments | Country |

Goulds 3700 API 610 | Introduction of the i-ALERT3 sensor suite with automated spectral analysis for early bearing failure detection in petrochemical plants. | USA |

9. Gardner Denver Holdings Inc (Ingersoll Rand)

Gardner Denver (now part of Ingersoll Rand) is the dominant player in the "workhorse" segment of the industry, including upstream drilling and well servicing. If you see a high-pressure pump on a drilling rig or a frac truck, there is a high probability it’s a Gardner Denver. Their innovation is focused on "serviceability." In the middle of a fracking operation, every minute of downtime costs thousands of dollars. Gardner Denver has redesigned their pump fluid ends to allow for "valves-in-minutes" replacement. They are also leading the shift toward electric fracking (e-frac), developing massive electric-motor-driven pumps that replace the noisy, emissions-heavy diesel engines traditionally used in the field.

Product | Developments | Country |

Thunder 5000 HP Frac Pump | Full-scale deployment of the "e-Frac" pump series, capable of continuous duty at 5000 HHP with zero onsite diesel emissions. | USA |

10. Baker Hughes Co.

Baker Hughes is not just a pump company; they are an energy technology company. Their acquisition and development of the Centrilift brand placed them at the top of the Electric Submersible Pump (ESP) market. ESPs are the lifeblood of maturing oil fields, used to lift fluids from deep underground to the surface. Baker Hughes’ innovation lies in the "extreme heat" category. As operators drill deeper into hotter formations, standard ESPs fail because their internal motors burn out. Baker Hughes has developed specialized motor cooling systems and high-temperature elastomers that allow their pumps to function in environments exceeding 200°C. Their integration of AI-driven "Production Optimization" allows these pumps to automatically adjust their speed based on the inflow of the well, maximizing recovery while protecting the pump's lifespan.

Product | Developments | Country |

Cenesis5™ ESP System | Launch of the "Cenesis" platform featuring high-temperature sensors and automated gas-handling software for volatile shale wells. | USA |

The Technological Frontier: Why it Matters Globally

The innovation described above isn't just about corporate profits; it’s about the fundamental "energy return on investment" (EROI) of our civilization. As we transition to a more complex energy mix, the efficiency of our fluid handling systems determines the cost of energy. If we can move a barrel of oil or a cubic meter of hydrogen with 10% less energy, the cumulative impact on global carbon emissions is staggering.

We are also seeing a convergence between the oil and gas pumping sector and the nascent hydrogen economy. Many of these companies, specifically Flowserve, Sulzer, and KSB, are currently testing how their existing pump architectures can be adapted for liquid hydrogen, which must be kept at -253°C. This demonstrates that the "Oil and Gas Pumps" market is effectively a "Fluids and Energy Transition" market. The same mechanical expertise used to manage a deepwater oil field is now being repurposed to inject CO2 back into those same reservoirs or to move the green fuels of the future.

Strategic Assumptions and Market Dynamics

From an analyst's perspective, the growth toward a USD 13.5 billion market is not just a function of higher oil prices. It is a function of "complexity inflation." We have moved past the era of "easy oil." The remaining reserves are deeper, more "sour" (high sulfur/H2S), and more difficult to reach. This requires more pumps, higher-pressure pumps, and more expensive materials.

A realistic assumption for the next five years is that we will see a massive consolidation of "Smart" technologies. It will no longer be enough to sell a pump; a manufacturer will need to provide a digital "health certificate" for that pump in real-time. We also anticipate that "Remanufacturing" will become a major revenue stream. Instead of scrapping a massive barrel pump, companies like Sulzer and Flowserve will use additive manufacturing to "rebuild" them to better-than-new specs, aligning with the circular economy goals of their supermajor clients like Shell, BP, and ExxonMobil.

The competitive dynamics are also shifting geographically. While American and European firms currently lead in high-end, complex pumping systems, we are seeing a push from Asian manufacturers toward the "mid-tier" market. However, the mission-critical nature of these pumps acts as a barrier to entry; in subsea or high-pressure fracking, an unproven brand is a risk most operators are unwilling to take. This gives the "Big 10" a significant advantage in the "Complexity Era."

Conclusion

The evolution of the oil and gas pump market highlights the industry's resilience and ability to adapt to high-tech advancements. As we approach 2031, the distinction between a "pump" and a "computer" will continue to blur, with autonomous systems managing energy flow with minimal human intervention. The companies mentioned are not merely maintaining the status quo; they are fundamentally redefining the mechanical limits of fluid dynamics. For investors and industry observers, the key takeaway is clear: the energy transition will be pumped, not just imagined, and the hardware required to move the world's energy remains an indispensable, high-growth cornerstone of the global industrial economy.

Get in Touch

Interested in this topic? Contact our analysts for more details.

Related Insights

Why the U.S. Is Seeing a Surge in Mental Health Care Needs

Jun 15, 2026

Top 10 Crude Oil Reserves in the World: How Iran–U.S. Tensions Are Reshaping Global Energy Markets

Jun 12, 2026

Top 10 Generative AI Companies in 2026: Products, Pricing, Funding, and Competitive Analysis

Jun 10, 2026

The Growing Importance of Home Healthcare for America’s Elderly Population

Jun 9, 2026

The Efficacy of Digital Health Records in Improving Patient Care in the United States

Jun 5, 2026