Report Overview

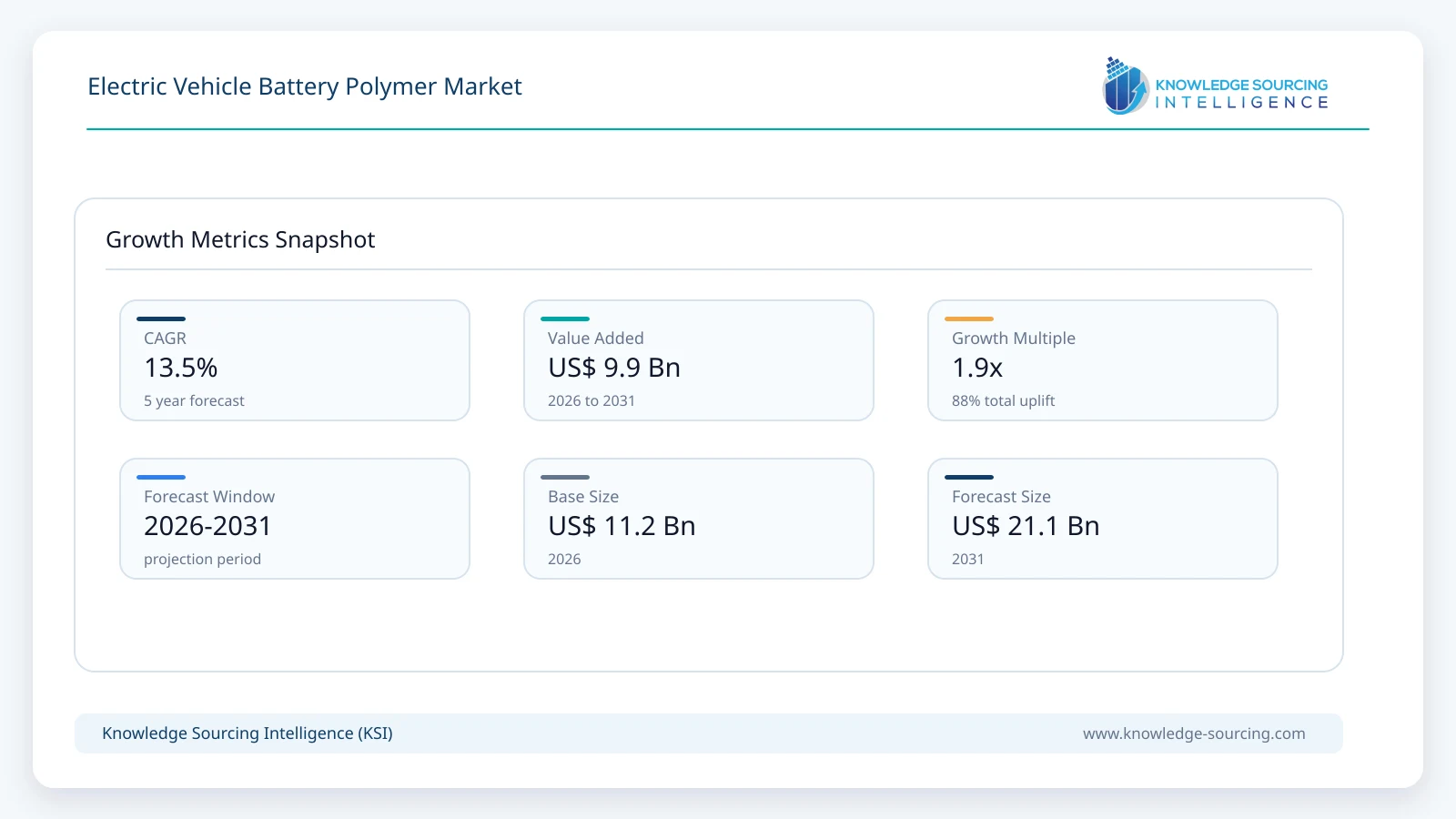

The electric vehicle battery polymer market will grow at a CAGR of 13.5% from USD 11.2 billion in 2026 to USD 21.1 billion in 2031.

Highlights:

- 1EV adoption is expanding the addressable polymer baseGlobal electric car sales exceeded 20 million in 2025, representing one-quarter of new car sales, while the International Energy Agency expects sales to reach about 23 million in 2026.

- 2Battery safety is increasing material requirementsHigher-voltage architectures, thermal management requirements, electrical insulation, flame resistance, and protection against thermal propagation are increasing demand for engineered polymer solutions.

- 3Engineering plastics remain strategically importantPolyamides, polycarbonate, PPS, fluoropolymers, polyurethane, and other engineered materials are increasingly used where lightweighting, dimensional stability, insulation, chemical resistance, and thermal performance are required.

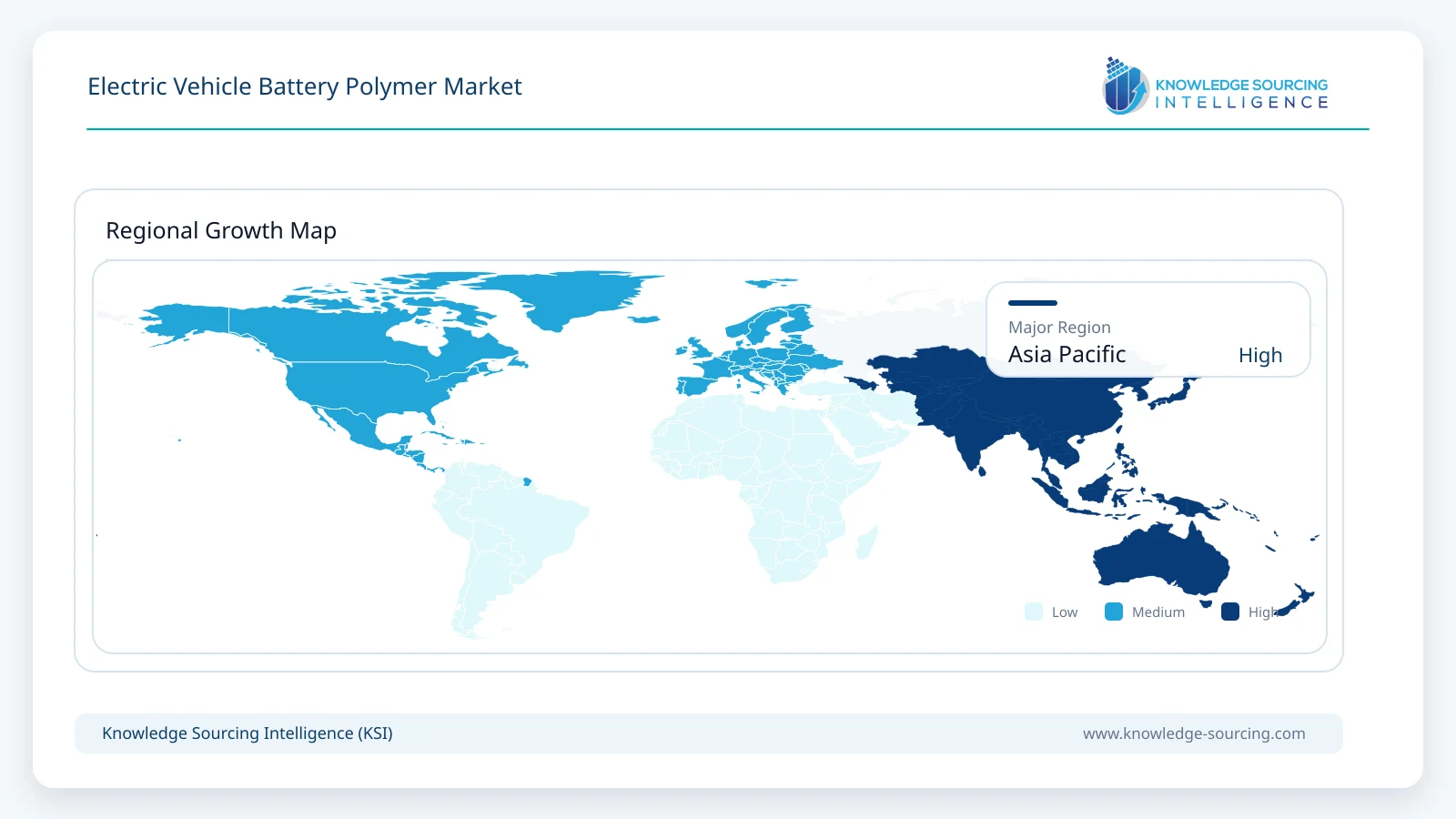

- 4Asia Pacific remains the principal demand centerChina continues to dominate global EV manufacturing and sales, while India, South Korea, Japan, and Southeast Asian economies are expanding EV production and adoption.

- 5Policy support is shifting from broad subsidies toward industrial developmentGovernments are increasingly combining EV incentives with domestic manufacturing, battery supply-chain localization, charging infrastructure, and material-security measures.

- 6Material innovation is moving toward higher performance and lower processing complexitySuppliers are developing polymers and compounds that can replace metals, integrate multiple functions, improve thermal safety, reduce weight, and support higher-voltage battery and power-electronics architectures.

The electric vehicle battery polymer market comprises polymeric materials used in and around EV battery systems to provide structural support, electrical insulation, thermal management, sealing, protection, lightweighting, and other performance functions. Depending on the application and material formulation, polymers can be incorporated into battery housings, covers, module components, insulation systems, sealing elements, encapsulation materials, connectors, thermal-management components, and related electric-drive systems.

The importance of polymers is increasing as battery and vehicle architectures become more compact, power-dense, and thermally demanding. Conventional metals remain important for structural battery components, but engineered polymers can provide lower density, electrical insulation, corrosion resistance, design flexibility, part integration, and manufacturing advantages. In selected applications, polymer compounds can combine reinforcement, flame retardancy, dimensional stability, and impact resistance in a single molded component. This makes material selection an increasingly important part of EV battery engineering rather than simply a substitution decision between plastics and metals.

The market is also supported by the broader expansion of electric mobility. According to the International Energy Agency's Global EV Outlook 2026, global electric car sales exceeded 20 million in 2025 and represented 25% of new car sales. The IEA expects global electric car sales to reach approximately 23 million in 2026, equivalent to around 28% of total car sales. China is expected to remain the largest EV market, while Europe, Asia Pacific excluding China, and Latin America are also expected to record substantial growth in 2026. These trends expand the installed base of battery-powered vehicles and, consequently, the need for materials used in battery packs and associated electrical systems.

China's scale is particularly important for the electric vehicle battery polymer market. Government data released in July 2026 showed that new energy vehicles represented 49.42% of newly registered automobiles in China during the first half of 2026. More than 5.19 million new energy vehicles were registered during the period, and the country's NEV fleet reached approximately 48.97 million by the end of June 2026. Pure electric vehicles represented nearly 69% of China's NEV stock. This scale supports demand for battery-pack polymers, insulation materials, engineering plastics, elastomers, thermal-management materials, and other polymer components across the country's large EV and battery manufacturing ecosystem.

India is also becoming an increasingly relevant growth market. The Government of India has continued to support EV adoption through the PM Electric Drive Revolution in Innovative Vehicle Enhancement (PM E-DRIVE) Scheme. Government data published in 2026 showed that 26.59 lakh EVs had been supported or sold under PM E-DRIVE as of June 30, 2026. The government also reported that EV adoption in India increased from 0.08% of vehicle sales in FY2015-16 to 8.26% in FY2025-26. Such expansion provides a growing downstream base for polymer demand across electric two-wheelers, three-wheelers, passenger vehicles, commercial vehicles, and their battery systems.

The market therefore extends beyond passenger cars. Electric two-wheelers, three-wheelers, buses, commercial vehicles, and other electrified platforms require polymers for battery enclosures, electrical insulation, connectors, seals, thermal-management components, and protective structures. The increasing diversity of EV platforms creates demand for different material grades rather than a single universal polymer solution.

Electric Vehicle Battery Polymer Market Trends:

The electric vehicle battery polymer market is being shaped by five major trends: increasing EV production, greater battery power density, stricter safety requirements, vehicle lightweighting, and localization of battery supply chains. These trends are changing the technical specifications required from polymers and are encouraging material suppliers to develop higher-performance grades.

One of the most important trends is the increasing emphasis on battery safety. As battery packs move toward higher voltage and greater energy density, materials used around cells and modules must withstand mechanical, thermal, electrical, and chemical stresses. Polymer components can provide electrical insulation and help reduce the risk of short circuits, while flame-retardant and thermally stable materials can contribute to limiting the propagation of heat and fire during abnormal battery events. The material requirement is therefore shifting from basic mechanical performance toward a combination of mechanical strength, insulation, thermal resistance, flame retardancy, and long-term durability.

Higher-voltage EV architectures are reinforcing this trend. Modern vehicle platforms are increasingly moving toward 800-volt electrical architectures to support higher power levels and faster charging. This increases the importance of insulation materials, connectors, housings, busbar components, and other polymer parts that must maintain electrical performance under demanding thermal conditions. Material suppliers are consequently developing polymers that combine high dielectric performance with dimensional stability and resistance to elevated temperatures.

Lightweighting is another structural market driver. Battery packs are among the heaviest components in an EV, and reducing the weight of supporting components can improve vehicle efficiency and offset some of the mass associated with larger batteries. Engineering plastics and polymer composites can replace or partially replace metal in selected housings, covers, brackets, connectors, and other components. The resulting benefits can include lower component weight, part consolidation, corrosion resistance, and greater freedom in component geometry.

Thermal management is also becoming increasingly important. Battery performance and life are closely linked to temperature control. Polymer materials can be used in thermal interface systems, insulation, cooling-system components, encapsulation materials, and other areas where controlled heat transfer or thermal isolation is required. The choice of polymer depends on the required thermal conductivity, electrical insulation, dimensional stability, chemical resistance, and operating-temperature range.

Another major trend is the development of materials for next-generation battery technologies. Solid-state and other advanced battery architectures may require different binders, separators, electrolytes, encapsulation systems, and structural materials than conventional lithium-ion batteries. This creates opportunities for specialty polymers with controlled chemical compatibility, elasticity, ionic-conductivity characteristics, or resistance to mechanical stresses generated during repeated charging and discharging.

Battery polymer suppliers are also focusing on processing efficiency. High-volume EV production requires materials that can be molded, extruded, or assembled consistently at automotive production speeds. Materials that reduce processing steps or allow multiple functions to be integrated into one component can provide cost and manufacturing advantages. This is particularly relevant for battery enclosures and large structural parts, where polymer compounds can potentially reduce the number of separate components required.

Sustainability is becoming another consideration in polymer selection. Automakers and battery manufacturers are increasingly examining recycled content, lower-carbon feedstocks, material efficiency, recyclability, and end-of-life recovery. This does not eliminate the importance of high-performance virgin polymers, because battery safety and reliability remain critical, but it is encouraging suppliers to develop lower-impact grades and more circular material systems.

Government policy is also influencing the market. Rather than relying exclusively on consumer purchase incentives, many governments are combining EV demand support with domestic manufacturing programs and supply-chain localization. In India, the PM E-DRIVE program supports EV adoption while incorporating measures intended to strengthen domestic manufacturing. In the United States and Europe, industrial policies have also encouraged domestic battery and critical-material supply chains. Such policies can influence where polymer production, compounding, and battery-component manufacturing are located.

The market nevertheless faces challenges. Advanced polymers can be more expensive than conventional materials, particularly when they require specialty additives, reinforcement, flame-retardant systems, or tight processing specifications. Qualification cycles in the automotive industry can also be lengthy because battery components must demonstrate reliability over extended operating conditions. In addition, polymer selection must consider thermal runaway behavior, chemical compatibility, electrical performance, aging, and manufacturability simultaneously. These requirements can increase development costs and create barriers for suppliers without automotive-grade testing and application-engineering capabilities.

Raw-material price volatility is another restraint. Many engineering polymers and specialty elastomers depend on petrochemical feedstocks, while fluoropolymers and other specialty materials may face additional supply-chain or regulatory considerations. As EV production scales, manufacturers are likely to place greater emphasis on long-term supply security, regional production, recycled feedstocks, and multi-source qualification.

Electric Vehicle Battery Polymer Market Segment Analysis:

The exterior segment by component is expected to remain an important application area for EV battery polymers.

In the electric vehicle battery polymer market, the exterior component segment covers polymer materials used in externally positioned or externally exposed battery-related structures and supporting components. The segment benefits from the demand for lighter, corrosion-resistant, electrically insulating, and durable materials that can withstand road exposure and demanding environmental conditions.

Battery covers, housings, protective structures, connectors, cable-management components, and selected enclosure elements can require polymers with a combination of impact resistance, dimensional stability, flame resistance, chemical resistance, and weathering performance. In suitable designs, reinforced thermoplastics can reduce weight compared with metal components while enabling complex geometries through injection molding or other high-volume manufacturing processes.

Exterior battery components also need to withstand water, dust, road contaminants, temperature cycling, vibration, and mechanical impact. Consequently, material selection cannot be based solely on low density. Automotive-grade polymers must maintain their mechanical and electrical characteristics over the expected operating life of the vehicle. Flame-retardant grades are particularly important where the component forms part of the battery enclosure or provides a barrier around high-voltage components.

The shift toward integrated battery-pack designs is creating additional opportunities for polymer suppliers. As manufacturers seek fewer components and simplified assembly, polymer compounds can support component integration by combining structural, insulation, thermal, and flame-retardant functions. This can potentially reduce assembly complexity and create opportunities for large molded components.

Government and OEM efforts to improve vehicle efficiency further support this segment. Lower component mass can contribute to overall vehicle efficiency, while polymeric materials can provide design flexibility that supports aerodynamic and packaging objectives. However, exterior battery applications remain subject to stringent durability and safety requirements, limiting the use of lower-cost polymers where higher-performance materials are required.

The engineering plastics segment by type is expected to remain a major growth area within the electric vehicle battery polymer market.

Engineering plastics are increasingly important because EV battery systems require materials that can deliver more than basic structural performance. Polyphenylene sulfide (PPS), acrylonitrile butadiene styrene (ABS), fluoropolymers, polyurethane, thermoplastic polyester, polycarbonate, and polyamide can address different requirements across battery and electrical systems.

PPS is particularly relevant where high-temperature resistance, dimensional stability, chemical resistance, and electrical performance are required. These characteristics can support applications involving connectors, electrical components, battery-related structures, and power-electronics systems. Fluoropolymers are important in applications requiring chemical resistance and specialized electrochemical performance, including selected binder and separator-coating applications.

Polycarbonate and polyamide grades can provide impact resistance, dimensional stability, and processing flexibility, while reinforced grades can improve stiffness and mechanical strength. Polyurethane can be used in encapsulation, cushioning, sealing, and thermal-management applications where its flexible or rigid characteristics are advantageous. Thermoplastic polyester materials can support electrical and structural applications where dimensional stability and processing performance are important.

The growth of this segment is being supported by the move toward higher-voltage electrical systems and more integrated battery packs. Material suppliers are developing grades with improved flame retardancy, electrical insulation, thermal stability, and mechanical performance. This is particularly relevant as automakers attempt to reduce component thickness and weight without compromising safety.

Recent supplier activity demonstrates this direction. In June 2026, SABIC highlighted its EV battery materials portfolio at Battery Show Europe, including specialty thermoplastics for battery packs and power electronics. The company showcased LNP THERMOCOMP OFM compounds based on PPS for high-power and high-voltage applications and highlighted NORYL NHP resin for insulation films in EV battery modules. Such developments illustrate how engineering plastics are being positioned for higher-voltage and higher-power vehicle architectures.

The engineering plastics segment will nevertheless face cost and qualification constraints. Automotive battery components often require extensive validation before entering series production. Suppliers that can provide consistent quality, application engineering, simulation, processing support, and global supply capabilities are therefore better positioned to participate in large-scale EV programs.

Electric Vehicle Battery Polymer Market Geographical Outlook:

Asia Pacific is expected to maintain a significant share of the electric vehicle battery polymer market.

Asia Pacific is the most important regional market because it combines large EV demand, extensive battery manufacturing capacity, major polymer producers, and strong automotive supply chains. China is the principal contributor, while Japan, South Korea, India, Vietnam, Indonesia, and Australia add to regional demand through different stages of the EV and battery value chain.

China is the dominant regional market. According to China's Ministry of Public Security, new energy vehicles accounted for 49.42% of newly registered automobiles during the first half of 2026. More than 5.19 million NEVs were registered between January and June, taking the national NEV fleet to approximately 48.97 million vehicles by the end of June. The scale of China's EV ecosystem supports demand for polymers across battery packs, electrical systems, thermal-management components, connectors, insulation systems, and vehicle structures.

China's battery and EV manufacturing concentration also creates opportunities for polymer suppliers to establish localized production and technical support. The country's large domestic market encourages material suppliers to qualify new polymer grades rapidly and to adapt materials for different cell formats, battery chemistries, and vehicle platforms.

India represents a high-growth opportunity within Asia Pacific. Government initiatives continue to encourage EV adoption and domestic manufacturing. The PM E-DRIVE Scheme provides incentives for several EV categories and supports the broader EV manufacturing ecosystem. As of June 30, 2026, government data indicated that 26.59 lakh EVs had been sold or supported under PM E-DRIVE. India also continues to promote domestic manufacturing through policies such as the Scheme to Promote Manufacturing of Electric Passenger Cars in India and broader production-linked initiatives.

The Indian market has a different demand profile from China because electric two-wheelers and three-wheelers represent important portions of EV adoption. This creates demand for polymer components suited to smaller battery packs, compact electrical systems, lightweight enclosures, connectors, insulation, and protective components. As passenger EV manufacturing expands, demand is expected to broaden toward higher-performance engineering plastics and battery-pack materials.

Japan and South Korea remain important because of their established automotive, electronics, battery, and advanced-material industries. These countries have strong capabilities in engineering plastics, battery materials, specialty chemicals, and high-precision manufacturing. Their importance is therefore not determined only by domestic EV sales but also by their roles as technology and materials suppliers to global EV value chains.

Southeast Asia is becoming increasingly relevant. The IEA reported that electric car sales in Southeast Asia more than doubled in 2025, reaching a sales share of nearly 20%, with Vietnam, Indonesia, and Thailand among the leading markets. The region is also attracting EV manufacturing investments, which can support local demand for battery polymers and other automotive materials.

North America is another significant market, supported by EV production, battery manufacturing investments, and demand for localized supply chains. Polymer suppliers are increasingly evaluating regional manufacturing strategies because automakers and battery manufacturers want secure supplies of qualified materials. The United States also has a large installed base of automotive polymer-processing capabilities, making it an important market for engineering plastics, elastomers, fluoropolymers, and specialized compounds.

Europe is driven by stringent vehicle emissions requirements, established automotive manufacturing, and demand for high-performance materials. The region's transition toward higher-voltage EV architectures and greater battery safety requirements is supporting demand for flame-retardant, electrically insulating, and thermally stable polymers. European material suppliers are also placing greater emphasis on circularity, lower-carbon production, and regulatory compliance.

South America is expected to develop gradually as EV adoption expands, particularly in Brazil and Mexico. Increasing availability of Chinese EVs, local manufacturing investments, and government policy changes are supporting electrification. Brazil recorded strong EV growth in 2025, while Mexico experienced a substantial increase in electric car sales. This creates longer-term opportunities for polymer suppliers serving localized vehicle assembly and battery-related component manufacturing.

The Middle East and Africa region remains smaller than Asia Pacific, Europe, and North America but offers selected opportunities. Saudi Arabia is developing an EV manufacturing ecosystem, while the UAE and Israel have technology, mobility, and fleet-electrification initiatives. Growth in these markets will depend on vehicle imports, local assembly, charging infrastructure, fleet electrification, and investment in regional manufacturing.

Electric Vehicle Battery Polymer Market Developments:

June 2026: Asahi Kasei Corporation announced that German battery manufacturer EAS Batteries had started sales of an ultra-high-power lithium-ion LFP cell using Asahi Kasei's Acetolyte™ electrolyte technology. The company reported that the acetonitrile-containing electrolyte provides high ionic conductivity, reduces internal resistance, and improves rate capability under demanding temperature conditions. The 22 Ah cell was reported to deliver 2,550 W/kg under continuous discharge and 3,760 W/kg during a two-second pulse discharge. Asahi Kasei and EAS Batteries are also evaluating the technology in a 46xxx cell format targeted at low-voltage EV battery applications. This development is relevant to the polymer market because it demonstrates the broader movement toward specialized polymer and chemical materials that enable higher-performance battery architectures.

June 2026: BASF SE introduced Oppanol® N PLUS, a high-performance polyisobutene-based binder for next-generation EV batteries. BASF stated that the binder is designed for modern battery concepts, including solid-state batteries, and can be used in cathode, anode, or electrolyte-related applications. The company highlighted the material's elasticity, extensibility, chemical inertness, and narrow product specifications, which are intended to improve process consistency and reduce production variability. The development demonstrates the increasing importance of specialty polymer binders as battery manufacturers pursue higher performance, longer life, and new cell architectures.

June 2026: Saudi Basic Industries Corporation (SABIC) showcased an expanded EV battery material portfolio at Battery Show Europe, including new LNP™ THERMOCOMP™ OFM compounds based on PPS for high-power and high-voltage electric-drive and power-module applications. SABIC also highlighted ULTEM™ resin for lightweight EV inverter housings, LNP KONDUIT™ compounds for high-voltage headers and thermal management, and NORYL™ NHP resin for insulation film in EV battery modules. The portfolio demonstrates the growing role of engineering thermoplastics in reducing weight, supporting electrical insulation, managing heat, and enabling higher-power EV architectures.

List of Top Electric Vehicle Battery Polymer Companies:

Asahi Kasei Corporation

BASF SE

Celanese Corporation

Covestro AG

LyondellBasell Industries N.V.

Saudi Basic Industries Corporation (SABIC)

Solvay

Electric Vehicle Battery Polymer Market Scope:

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 11.2 billion |

| Total Market Size in 2031 | USD 21.1 billion |

| Forecast Unit | Billion |

| Growth Rate | 13.5% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Component, Type, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Component

- Exterior

- Interior

By Type

- Elastomers

- Silicone Elastomer

- Synthetic Rubber

- Fluoroelastomer

- Engineering Plastics

- Polyphenylene Sulphide (PPS)

- Acrylonitrile Butadiene Styrene (ABS)

- Fluoropolymer

- Polyurethane

- Thermoplastic Polyester

- Polycarbonate

- Polyamide

- Others

By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- United Kingdom

- Germany

- France

- Spain

- Others

- Middle East and Africa

- Saudi Arabia

- Israel

- United Arab Emirates

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Vietnam

- Indonesia

- Others

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

1.8. Key benefits for the stakeholders

2. RESEARCH METHODOLOGY

2.1. Research Design

2.2. Research Process

3. EXECUTIVE SUMMARY

3.1. Key Findings

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Porter’s Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of New Entrants

4.3.4. Threat of Substitutes

4.3.5. Competitive Rivalry in the Industry

4.4. Industry Value Chain Analysis

4.5. Analyst View

5. ELECTRIC VEHICLE BATTERY POLYMER MARKET BY COMPONENT

5.1. Introduction

5.2. Exterior

5.3. Interior

6. ELECTRIC VEHICLE BATTERY POLYMER MARKET BY TYPE

6.1. Introduction

6.2. Elastomers

6.2.1. Silicone Elastomer

6.2.2. Synthetic Rubber

6.2.3. Fluoroelastomer

6.3. Engineering Plastics

6.3.1. Polyphenylene Sulphide (PPS)

6.3.2. Acrylonitrile Butadiene Styrene (ABS)

6.3.3. Fluoropolymer

6.3.4. Polyurethane

6.3.5. Thermoplastic Polyester

6.3.6. Polycarbonate

6.3.7. Polyamide

6.3.8. Others

7. ELECTRIC VEHICLE BATTERY POLYMER MARKET BY GEOGRAPHY

7.1. Introduction

7.2. North America

7.2.1. By Component

7.2.2. By Type

7.2.3. By Country

7.2.3.1. United States

7.2.3.2. Canada

7.2.3.3. Mexico

7.3. South America

7.3.1. By Component

7.3.2. By Type

7.3.3. By Country

7.3.3.1. Brazil

7.3.3.2. Argentina

7.3.3.3. Others

7.4. Europe

7.4.1. By Component

7.4.2. By Type

7.4.3. By Country

7.4.3.1. United Kingdom

7.4.3.2. Germany

7.4.3.3. France

7.4.3.4. Spain

7.4.3.5. Others

7.5. Middle East and Africa

7.5.1. By Component

7.5.2. By Type

7.5.3. By Country

7.5.3.1. Saudi Arabia

7.5.3.2. Israel

7.5.3.3. United Arab Emirates

7.5.3.4. Others

7.6. Asia Pacific

7.6.1. By Component

7.6.2. By Type

7.6.3. By Country

7.6.3.1. China

7.6.3.2. Japan

7.6.3.3. India

7.6.3.4. South Korea

7.6.3.5. Australia

7.6.3.6. Vietnam

7.6.3.7. Indonesia

7.6.3.8. Others

8. COMPETITIVE ENVIRONMENT AND ANALYSIS

8.1. Major Players and Strategy Analysis

8.2. Market Share Analysis

8.3. Mergers, Acquisitions, Agreements, and Collaborations

8.4. Competitive Dashboard

9. COMPANY PROFILES

9.1. Asahi Kasei Corporation

9.2. BASF SE

9.3. Celanese Corporation

9.4. Covestro AG

9.5. LyondellBasell Industries N.V.

9.6. Saudi Basic Industries Corporation (SABIC)

9.7. Solvay

Navigate

Trusted by the world's leading organizations