Report Overview

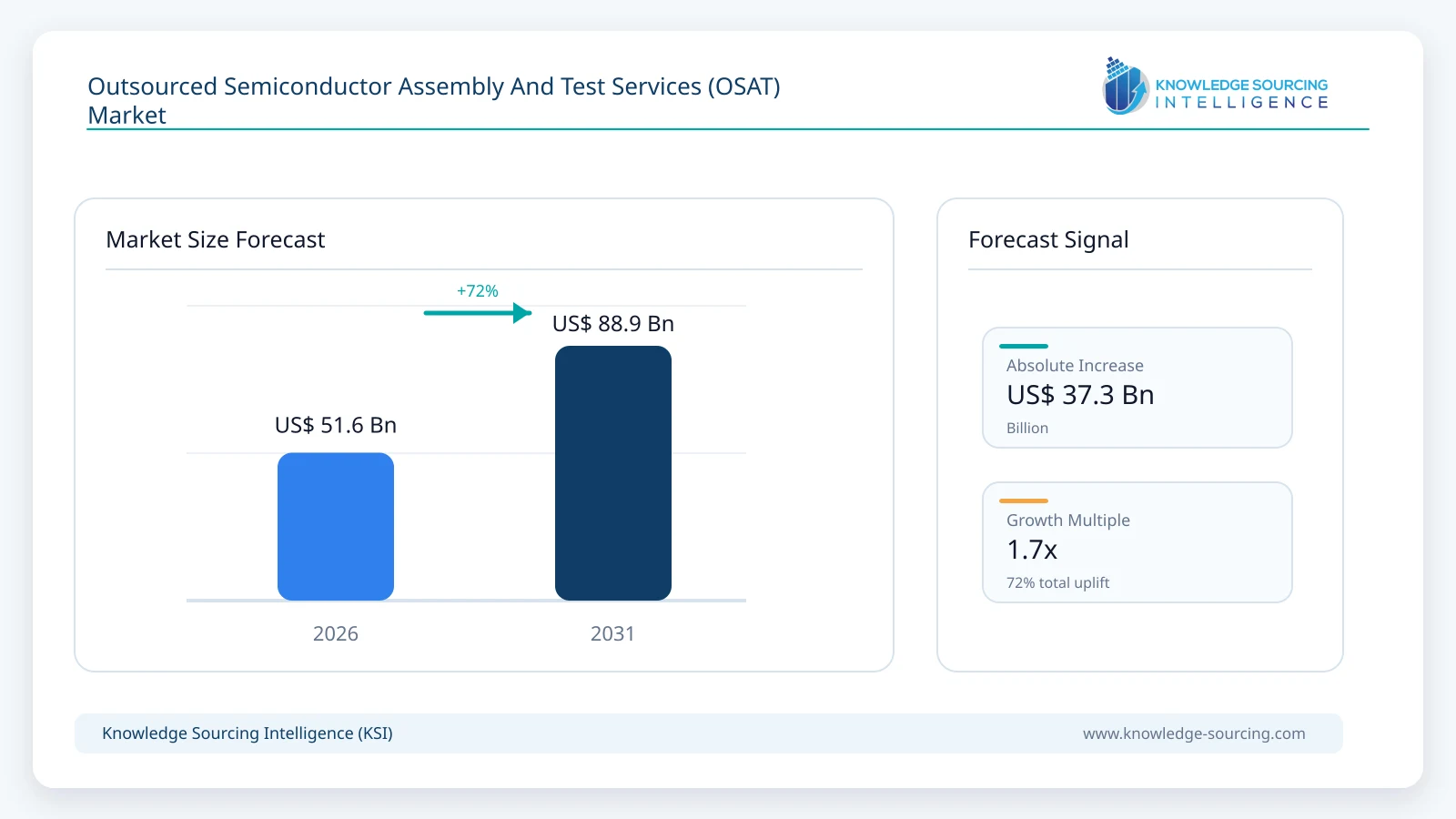

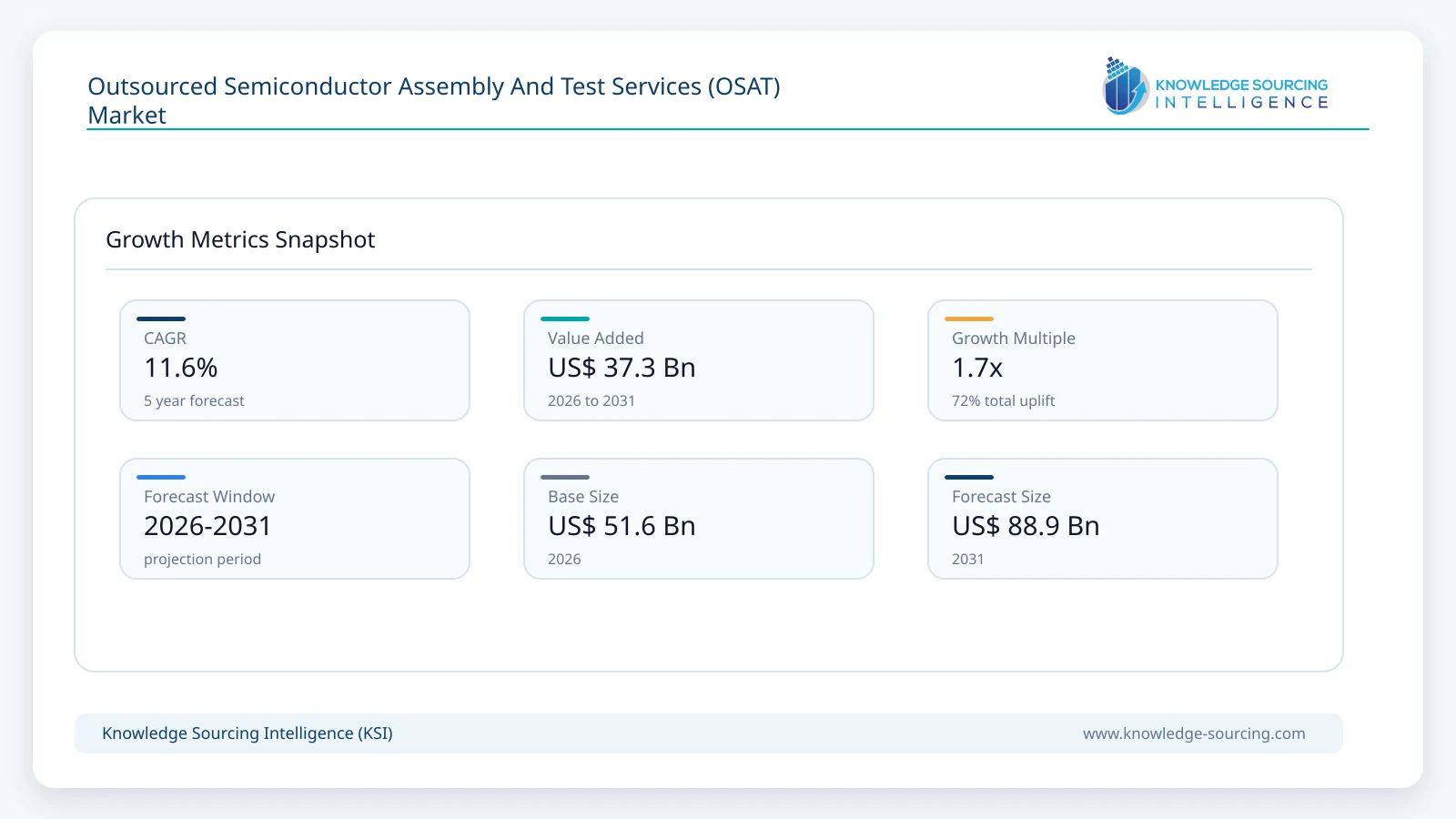

The Outsourced Semiconductor Assembly and Test (OSAT) market is forecast to grow at a CAGR of 11.5%, reaching USD 88.9 billion in 2031 from USD 51.6 billion in 2026.

Highlights:

- 1Advanced semiconductor demand is accelerating OSAT expansionGrowth in AI, high-performance computing (HPC), and edge devices is increasing reliance on outsourced packaging and testing capacity.

- 2Shift toward advanced packaging technologies2.5D/3D integration, fan-out wafer-level packaging, and chiplet architectures are reshaping OSAT service complexity and value addition.

- 3Asia Pacific remains the global production hubTaiwan, China, South Korea, and Southeast Asia dominate OSAT capacity due to dense semiconductor supply chains and foundry proximity.

- 4Supply chain restructuring is strengthening regional OSAT ecosystemsGovernments and semiconductor firms are investing in localized assembly and test capacity to reduce geopolitical and logistics risks.

Outsourced Semiconductor Assembly and Test (OSAT) services refer to the outsourced post-fabrication segment of the semiconductor value chain, covering assembly, packaging, and testing of semiconductor devices before final integration into electronic systems. OSAT providers play a critical role in enabling integrated circuit (IC) performance, thermal management, electrical reliability, and miniaturization.

The OSAT ecosystem is structurally embedded within the global semiconductor manufacturing value chain and primarily serves integrated device manufacturers (IDMs) and fabless semiconductor companies. As semiconductor designs become more complex with heterogeneous integration, chiplet-based architectures, and system-in-package (SiP) solutions, OSAT providers have transitioned from traditional packaging vendors to advanced technology partners.

Market growth is strongly driven by demand from high-growth end-use industries, including artificial intelligence, 5G infrastructure, automotive electronics, industrial automation, and consumer electronics. In particular, AI servers, advanced GPUs, and edge computing devices require high-density packaging and thermally efficient designs, significantly increasing dependency on advanced OSAT capabilities.

In addition, electric vehicles and advanced driver-assistance systems (ADAS) are increasing semiconductor content per vehicle, creating sustained demand for power management ICs, sensors, and high-reliability automotive-grade packaging and testing services.

OSAT Market Segment Analysis:

The Outsourced Semiconductor Assembly and Test (OSAT) market is segmented by:

By Service Type: Assembly services and testing services. Testing services are witnessing strong demand due to increased complexity of semiconductor devices and stringent quality and reliability requirements across automotive and industrial applications.

By Packaging Type: Ball Grid Array (BGA), Chip Scale Package (CSP), Multi-Chip Module (MCM), System-in-Package (SiP), Flip-Chip, and advanced 2.5D/3D packaging solutions. Advanced packaging is gaining share due to chiplet integration trends.

By Device Type: Memory devices, logic devices, analog and mixed-signal ICs, and power semiconductors. Logic and memory devices remain dominant due to AI compute and data center expansion.

By Application: Consumer electronics, automotive, industrial, telecommunications, and computing. Consumer electronics and automotive are key volume and value contributors.

By Region: North America, Europe, Asia Pacific, and Middle East & Africa. Asia Pacific leads due to integrated semiconductor manufacturing ecosystems.

Top Trends Shaping the OSAT Market:

Acceleration of advanced packaging adoption

The semiconductor industry is undergoing a structural transition from traditional scaling (Moore’s Law) toward heterogeneous integration and advanced packaging. Technologies such as fan-out wafer-level packaging (FOWLP), chiplet integration, and 3D stacking are increasingly central to performance improvement strategies. This transition is significantly increasing the technical intensity and capital requirements of OSAT providers.

Advanced packaging enables higher bandwidth density, lower latency, and improved power efficiency, making it essential for AI accelerators, high-performance GPUs, and data center processors.

OSAT Market Growth Drivers vs. Challenges:

Drivers:

Rising semiconductor content per device: The increasing complexity of electronic systems across automotive, industrial, and consumer sectors is driving higher semiconductor integration levels, boosting demand for packaging and testing services.

Expansion of AI and data center infrastructure: AI workloads and hyperscale data centers require advanced semiconductor packaging solutions such as high-bandwidth memory integration and chiplet-based architectures, strengthening OSAT demand.

Automotive semiconductor growth: Electrification and autonomous driving technologies are increasing demand for high-reliability, automotive-grade packaging and rigorous testing standards.

Challenges:

High capital intensity and technology barriers: Transition to advanced packaging requires substantial investment in equipment, R&D, and cleanroom infrastructure, limiting entry for new players.

Supply chain and geopolitical risks: Concentration of OSAT capacity in Asia Pacific exposes the industry to geopolitical tensions, trade restrictions, and supply chain disruptions.

Pricing pressure from integrated semiconductor players: Large IDM and foundry ecosystems are increasingly internalizing advanced packaging capabilities, creating competitive pressure for pure-play OSAT providers.

OSAT Market Regional Analysis:

Asia Pacific: Asia Pacific dominates the global OSAT market due to dense semiconductor ecosystems across Taiwan, China, South Korea, Malaysia, and Singapore. The region benefits from proximity to leading foundries, cost advantages, skilled labor availability, and strong government support for semiconductor manufacturing expansion.

Taiwan remains a critical hub for advanced packaging technologies, while China continues to expand domestic OSAT capacity to strengthen semiconductor self-sufficiency. Southeast Asia is emerging as a strategic extension for assembly and testing operations due to favorable investment conditions and supply chain diversification trends.

North America and Europe are increasingly investing in localized semiconductor packaging and testing infrastructure to reduce dependency on Asia-based supply chains and strengthen technological sovereignty in advanced semiconductor manufacturing.

OSAT Market Competitive Landscape:

The OSAT market is moderately consolidated at the top and fragmented in mid-tier segments. Leading players focus on advanced packaging innovation, geographic expansion, and capacity scaling to support AI-driven semiconductor demand. Key companies include ASE Technology Holding Co., Ltd., Amkor Technology, Inc., Powertech Technology Inc., JCET Group Co., Ltd., Tongfu Microelectronics Co., Ltd., ChipMOS Technologies Inc., and UTAC Holdings Ltd.

Competitive differentiation is increasingly based on advanced packaging capabilities, technology partnerships with foundries, automotive qualification standards, and long-term capacity agreements with fabless semiconductor companies.

OSAT Market Developments (Verified Industry-Level Events):

June 2026: Amkor Technology and TSMC announced a long-term partnership to accelerate advanced semiconductor packaging in the United States, strengthening domestic OSAT capabilities and supporting next-generation AI and high-performance computing semiconductor production.

May 2026: ASE announced the industry's first automated 310 mm × 310 mm panel-level packaging production line, enabling higher manufacturing efficiency and scalable heterogeneous integration for AI, HPC, networking, and chiplet-based semiconductor devices.

April 2026: CG Semi confirmed operational ramp-up of its OSAT facility in Sanand, Gujarat, targeting commercial production during 2026. The project is part of a ?7,600 crore investment across two facilities (G1 and G2), significantly expanding India’s semiconductor assembly, packaging, and testing ecosystem.

March 2026: Kaynes Semicon inaugurated and began commercial production at its Outsourced Semiconductor Assembly and Test (OSAT) facility in Sanand, Gujarat, on March 31, 2026. The plant, developed under India Semiconductor Mission support, delivers ~6.3 million chips per day.

February 2026: Micron Technology inaugurated its semiconductor assembly and test facility in Sanand, Gujarat, India on February 28, 2026. The site processes DRAM and NAND wafers into finished memory products, strengthening global OSAT capacity. The project represents a $2.75 billion investment expanding advanced packaging and testing operations.

OSAT Market Scope:

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 51.6 billion |

| Total Market Size in 2031 | USD 88.9 billion |

| Forecast Unit | USD Billion |

| Growth Rate | 11.5% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Service Type, Packaging Type, Device Type, Application, Geography |

| Geographical Segmentation | Americas, Europe Middle East and Africa (EMEA), Asia Pacific (APAC) |

| Companies |

|

Market Segmentation

By Service Type

By Packaging Type

By Device Type

By Application

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. OSAT MARKET BY SERVICE TYPE

5.1. Introduction

5.2. Packaging

5.3. Testing

5.4. Other

6. OSAT MARKET BY PACKAGING TYPE

6.1. Introduction

6.2. Ball Grid Array (BGA) Packaging

6.3. Chip-scale Packaging (CSP)

6.4. Stacked Die Packaging

6.5. Multi-Chip Packaging

6.6. Quad Flat and Dual-inline Packaging

7. OSAT MARKET BY DEVICE TYPE

7.1. Introduction

7.2. Logic Devices

7.3. Memory Devices

7.4. Analog and Mixed-Signal Devices

7.5. Others

8. OSAT MARKET BY APPLICATION

8.1. Introduction

8.2. Communication

8.3. Consumer Electronics

8.4. Automotive

8.5. Computing and Networking

8.6. Industrial

8.7. Others

9. OSAT MARKET BY GEOGRAPHY

9.1. Introduction

9.2. Americas

9.2.1. USA

9.3. Europe Middle East and Africa (EMEA)

9.3.1. Germany

9.3.2. Netherlands

9.3.3. Others

9.4. Asia Pacific (APAC)

9.4.1. China

9.4.2. Japan

9.4.3. Taiwan

9.4.4. South Korea

9.4.5. Others

10. COMPETITIVE ENVIRONMENT AND ANALYSIS

10.1. Major Players and Strategy Analysis

10.2. Market Share Analysis

10.3. Mergers, Acquisitions, Agreements, and Collaborations

10.4. Competitive Dashboard

11. COMPANY PROFILES

11.1. ASE Group (ASE Technology Holdings)

11.2. Amkor Technology Inc.

11.3. Powertech Technology Inc.

11.4. ChipMOS Technologies Inc.

11.5. King Yuan Electronics Co., Ltd.

11.6. Jiangsu Changjiang Electronics Technology Co., Ltd.

11.7. UTAC Holdings Ltd.

11.8. Lingsen Precision Industries Ltd.

11.9. Tongfu Microelectronics Co.

12. APPENDIX

12.1. Currency

12.2. Assumptions

12.3. Base and Forecast Years Timeline

12.4. Key benefits for the stakeholders

12.5. Research Methodology

12.6. Abbreviations

Navigate

Trusted by the world's leading organizations