Report Overview

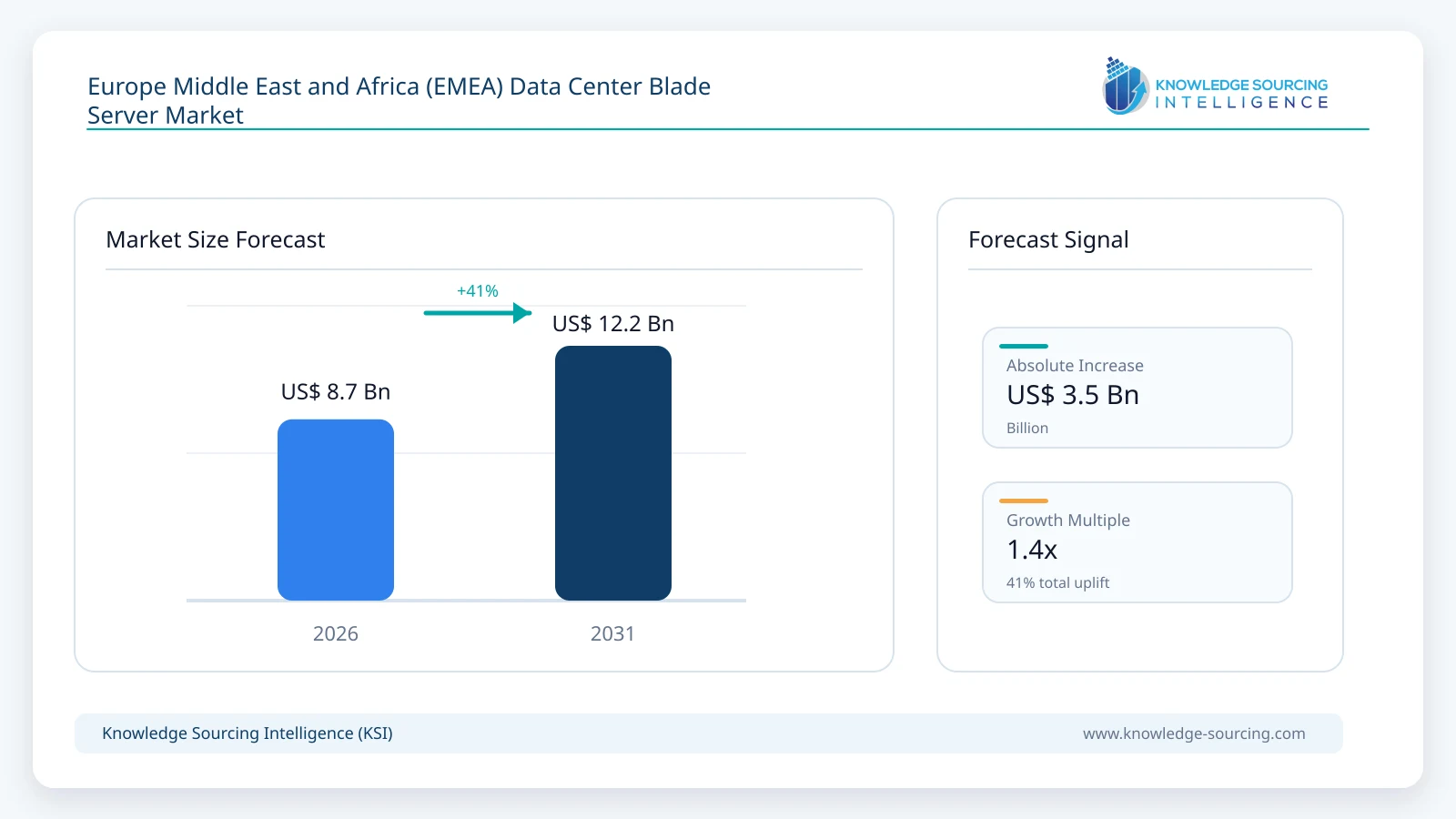

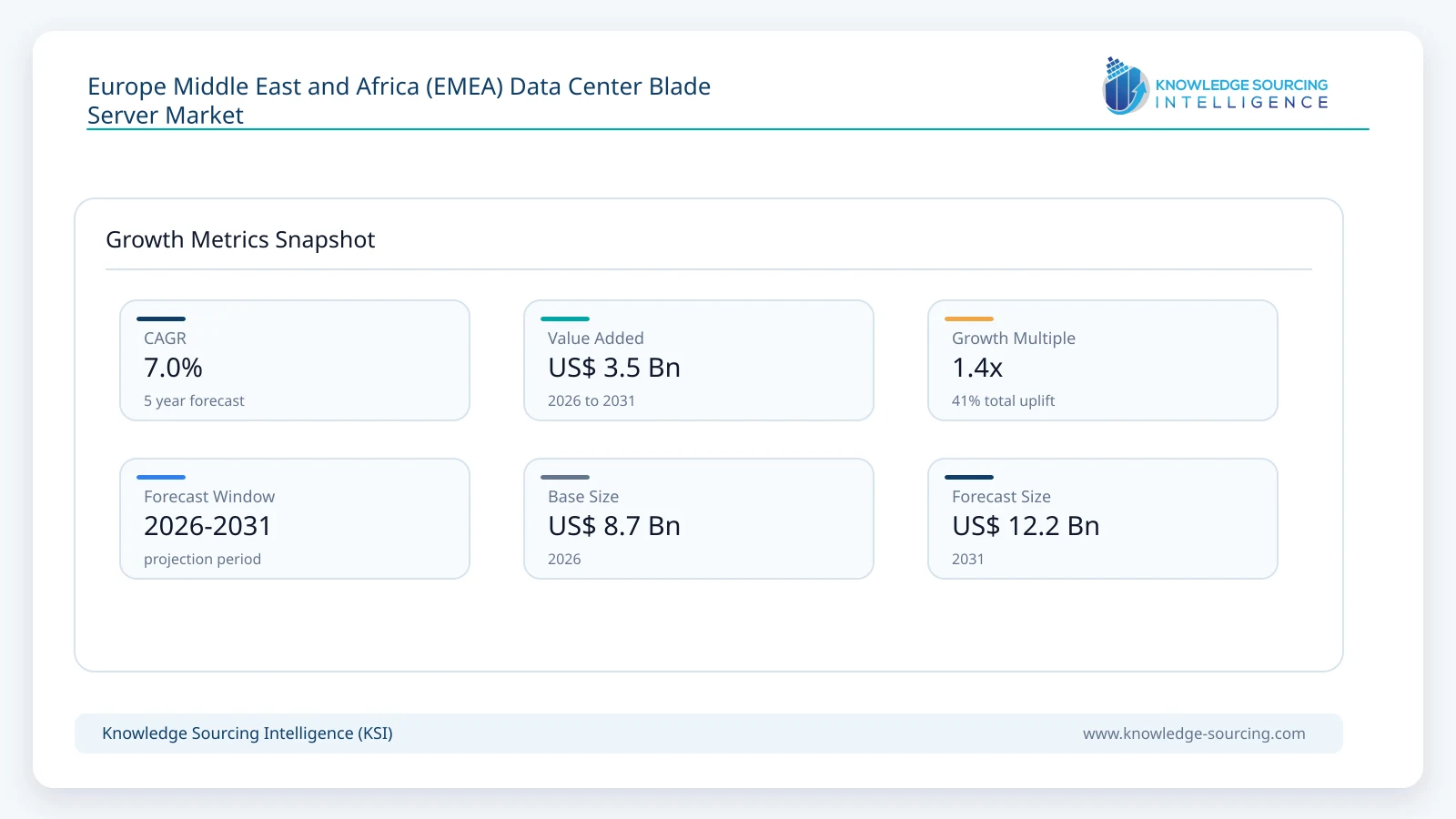

The Europe, Middle East and Africa (EMEA) Data Center Blade Server Market is forecast to grow at a CAGR of 7.05%, reaching USD 12.20 billion in 2031 from USD 8.68 billion in 2026.

Highlights:

- 1Expansion of enterprise AI, virtualization, and hybrid cloud infrastructure continues to stimulate demand for high-density blade server deployments.

- 2Large enterprises remain the most commercially important customer segment because of extensive computing requirements and centralized data center operations.

- 3Western Europe leads procurement volumes, while Saudi Arabia and the United Arab Emirates present attractive investment opportunities through hyperscale and government-backed digital infrastructure projects.

- 4Integration of AI-assisted infrastructure management, software-defined operations, and liquid-ready server designs is influencing product development.

- 5European energy efficiency regulations and national digital infrastructure programmes encourage investment in modern, lower-power computing platforms.

- 6Competition increasingly centres on integrated infrastructure solutions, lifecycle services, and enterprise support capabilities rather than hardware pricing alone.

The Europe Middle East and Africa (EMEA) data center blade server market represents an important segment of enterprise computing infrastructure, supplying high-density server platforms that support virtualization, private and hybrid cloud deployments, artificial intelligence (AI) workloads, high-performance computing (HPC), enterprise databases, and mission-critical business applications. Blade servers integrate compute resources into a modular chassis, allowing organizations to improve space utilization, simplify management, reduce cabling complexity, and enhance power efficiency compared with traditional rack-mounted architectures. Their value proposition is particularly attractive for organizations operating large-scale data centers where infrastructure density, operational continuity, and centralized management directly influence operating costs.

Demand across EMEA continues to be shaped by enterprise modernization programmes rather than conventional hardware refresh cycles alone. Financial institutions, telecommunications operators, public-sector organizations, healthcare providers, cloud service providers, and multinational manufacturers are investing in new computing platforms capable of supporting AI-enabled analytics, software-defined infrastructure, containerized applications, and edge computing environments. Buyers increasingly evaluate blade servers based on lifecycle cost, workload compatibility, energy efficiency, security capabilities, automation support, and integration with existing management software instead of focusing solely on processor performance.

Regional investment patterns remain diverse. Western Europe continues to account for substantial procurement activity because of mature cloud adoption, expanding colocation capacity, and enterprise digital infrastructure upgrades. Meanwhile, Gulf Cooperation Council (GCC) countries are investing heavily in hyperscale facilities and sovereign cloud infrastructure to diversify national economies and strengthen digital capabilities. South Africa serves as an important gateway for digital infrastructure investment across Sub-Saharan Africa, supported by expanding internet connectivity, financial services modernization, and cloud adoption.

Procurement strategies have also become more sophisticated. Enterprise buyers increasingly favour modular infrastructure capable of supporting future processor generations, GPU integration, higher memory capacities, and software-defined management. Many organizations are adopting phased procurement models, allowing infrastructure expansion without replacing complete server estates. This approach reduces capital expenditure risk while supporting long-term capacity planning.

Another characteristic of the market is the growing influence of sustainability objectives. Electricity prices across several European countries, combined with corporate carbon reduction targets, have shifted purchasing priorities toward energy-efficient server platforms with advanced cooling compatibility, intelligent workload management, and improved power utilization. Consequently, infrastructure decisions increasingly involve collaboration between information technology teams, facilities managers, sustainability departments, and procurement specialists.

The supplier ecosystem combines global server manufacturers with component suppliers, channel partners, systems integrators, and managed service providers. Vendors compete through integrated hardware and software portfolios, lifecycle support services, infrastructure management platforms, and long-term enterprise relationships. Rather than competing exclusively on hardware specifications, suppliers increasingly differentiate themselves through automation capabilities, predictive maintenance, workload optimization, cybersecurity features, and flexible financing arrangements.

Market Drivers

Expansion of Hybrid Cloud and Enterprise Virtualization

Many organizations across EMEA continue to operate mixed computing environments combining on-premises infrastructure with public cloud services. This operating model requires highly reliable server platforms capable of hosting virtualized workloads while maintaining operational flexibility. Blade servers satisfy these requirements through centralized administration, simplified resource allocation, and efficient infrastructure scaling. Vendors have responded by enhancing compatibility with hybrid cloud management platforms, enabling customers to manage physical and virtual resources through unified operational frameworks.

Growth in Artificial Intelligence and High-Performance Computing Workloads

AI model development, inference applications, engineering simulations, and advanced analytics require higher processing density and memory bandwidth than conventional enterprise workloads. Enterprises are therefore investing in modular server infrastructure capable of supporting accelerator cards and future processor upgrades. Suppliers continue expanding blade server portfolios designed for GPU-enabled environments while improving thermal management and power delivery systems to accommodate increasingly demanding computational workloads.

Data Sovereignty and Regulatory Compliance Requirements

Governments and regulated industries across Europe and parts of the Middle East increasingly require sensitive information to remain within national or regional jurisdictions. Financial institutions, healthcare organizations, and government agencies consequently continue investing in privately controlled infrastructure instead of transferring all workloads to public cloud providers. Blade server platforms support these deployments by offering scalable computing environments that satisfy operational resilience, security, and compliance objectives.

Continued Investment in Hyperscale and Colocation Data Centers

Cloud providers, colocation operators, and managed service providers continue expanding regional capacity to accommodate rising enterprise computing requirements. These operators prioritize infrastructure density, standardized deployment, and efficient maintenance processes. Blade architectures align well with these operational objectives by enabling rapid provisioning, simplified hardware replacement, and improved utilization of available data center space.

Market Restraints and Challenges

High Initial Infrastructure Investment

Although blade servers improve long-term operational efficiency, deployment requires investment in chassis systems, networking infrastructure, storage integration, cooling, and management software. Smaller organizations frequently find these upfront costs difficult to justify, particularly when workload requirements remain relatively modest. Vendors increasingly address this challenge through financing options, subscription-based infrastructure services, and flexible procurement agreements.

Increasing Competition from Hyperconverged Infrastructure

Many organizations now evaluate hyperconverged infrastructure (HCI) alongside blade server deployments. HCI simplifies deployment by integrating compute, storage, and virtualization into unified platforms. This alternative can reduce infrastructure complexity for mid-sized enterprises, creating competitive pressure for conventional blade server suppliers. Manufacturers therefore continue enhancing management software and interoperability to maintain competitiveness.

Power Availability and Data Center Energy Constraints

Electricity supply limitations, rising utility costs, and stricter sustainability objectives affect infrastructure expansion across several EMEA markets. Data center operators increasingly assess power consumption alongside computing performance during procurement. Suppliers consequently invest in improved processor efficiency, intelligent power management, and advanced cooling compatibility to reduce operational energy requirements.

Semiconductor Supply Chain Volatility

Although supply conditions have improved compared with previous disruptions, component availability remains sensitive to geopolitical developments, advanced semiconductor manufacturing capacity, and logistics constraints. Extended procurement lead times can delay infrastructure projects and complicate enterprise budgeting. Many organizations now diversify supplier relationships and maintain longer procurement planning cycles to reduce supply risk.

Major Segment Analysis

Large Enterprises

Large enterprises represent the most commercially significant organization size segment within the EMEA data center blade server market. These organizations typically operate multiple regional data centers supporting thousands of virtual machines, enterprise applications, customer-facing digital platforms, and mission-critical databases. Their procurement decisions prioritize infrastructure reliability, lifecycle management, cybersecurity, scalability, and operational continuity rather than initial acquisition cost alone.

Demand remains particularly strong among financial institutions, telecommunications providers, government agencies, multinational manufacturers, and large healthcare organizations managing complex workloads with stringent availability requirements. These buyers frequently standardize infrastructure across multiple facilities, creating opportunities for long-term supply agreements and managed lifecycle services.

Competition within this segment extends beyond server performance. Suppliers differentiate through integrated management software, predictive maintenance capabilities, workload optimization, security certifications, and comprehensive support services. Enterprise customers also favour suppliers capable of providing global service coverage, local technical expertise, and consistent product roadmaps. As organizations continue modernizing legacy infrastructure while preparing for AI-enabled workloads, this segment is expected to remain the primary contributor to market revenue.

Competitive Landscape

The competitive environment consists of globally established infrastructure vendors including Dell Technologies Inc., Cisco Systems, Inc., Huawei Technologies Co., Ltd., International Business Machines Corporation (IBM), Lenovo Group Limited, Inspur Electronic Information Industry Co., Ltd., Fujitsu Limited, NEC Corporation, and Hewlett Packard Enterprise (HPE). Competition centres on integrated infrastructure ecosystems rather than standalone server hardware.

Suppliers differentiate through processor support, workload optimization, infrastructure automation, cybersecurity capabilities, AI-enabled systems management, and comprehensive enterprise support services. Strategic partnerships with processor manufacturers, virtualization software providers, cloud platform vendors, and systems integrators strengthen customer value propositions. Geographic expansion, localized technical support, sustainability-focused product development, and lifecycle management services remain important competitive factors across the EMEA region.

Recent Developments

June 2026: Dell Technologies introduced the Dell PowerEdge XE8812 server at ISC 2026 in Hamburg, Germany, featuring NVIDIA Vera Rubin NVL4 architecture and supporting up to 144 GPUs per rack for high-performance AI and HPC data centre deployments across EMEA.

April 2026: Hewlett Packard Enterprise (HPE) expanded its HPE ProLiant Compute portfolio by launching new edge server platforms, including the EL220 and EL240 Gen12 systems and an enhanced ProLiant DL145 Gen11, supporting AI and mission-critical workloads in distributed environments.

March 2026: Hewlett Packard Enterprise expanded AI-optimised enterprise infrastructure offerings supporting next-generation compute-intensive workloads. The development strengthens enterprise readiness for large-scale AI deployments across regional data centers.

Regulatory and Policy Environment

The regulatory framework influencing the EMEA data center blade server market combines cybersecurity requirements, environmental legislation, energy efficiency standards, and data governance policies. Within Europe, the General Data Protection Regulation (GDPR) continues influencing enterprise infrastructure decisions by encouraging organizations to maintain secure processing environments for sensitive information. The NIS2 Directive strengthens cybersecurity obligations for operators of essential services and digital infrastructure, increasing investment in resilient computing platforms.

The European Union's Energy Efficiency Directive and sustainability initiatives encourage data center operators to improve energy performance while reducing environmental impact. Several European governments also support national cloud infrastructure programmes and digital sovereignty initiatives that stimulate investment in domestic computing capacity. Across the Middle East, national digital transformation strategies and sovereign cloud programmes continue supporting construction of advanced data center infrastructure capable of hosting government and regulated industry workloads.

Outlook and Strategic Implications

The EMEA data center blade server market is expected to remain closely linked to enterprise AI adoption, hybrid cloud expansion, and modernization of mission-critical computing infrastructure through the forecast period. Organizations are expected to prioritize scalable platforms capable of accommodating higher processor densities, GPU acceleration, advanced networking technologies, and software-defined management without extensive infrastructure replacement.

Investment decisions will increasingly balance computational performance with energy consumption, operational resilience, and regulatory compliance. Procurement teams are expected to favour suppliers offering integrated lifecycle services, automation capabilities, flexible financing models, and long-term product roadmaps. Sustainability objectives will continue influencing hardware selection as electricity costs and environmental reporting requirements receive greater board-level attention.

Competitive positioning is likely to depend on ecosystem strength rather than hardware specifications alone. Vendors capable of integrating AI infrastructure, advanced systems management, cybersecurity, and comprehensive support services into unified enterprise solutions will be better positioned to secure long-term contracts. Despite ongoing challenges related to power availability, supply chain resilience, and infrastructure investment costs, continued expansion of cloud services, AI workloads, digital government programmes, and enterprise modernization initiatives is expected to sustain demand for blade server infrastructure across the Europe, Middle East, and Africa region through 2031.

Europe, Middle East and Africa (EMEA) Data Center Blade Server Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 8.68 billion |

| Total Market Size in 2031 | USD 12.20 billion |

| Forecast Unit | Billion |

| Growth Rate | 7.05% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Data Center Type, Service, Organization Size, Vertical, Geography |

| Companies |

|

Market Segmentation

By Data Center Type

- Tier 1

- Tier 2

- Tier 3

- Tier 4

By Service

- Consulting Services

- Installation & Deployment Services

- Support & Maintenance Services

By Organization Size

- Large Enterprises

- Medium Enterprises

- Small Enterprises

By Vertical

- IT and Telecom

- Manufacturing

- Media and Entertainment

- Banking, Financial Services, and Insurance (BFSI)

- Retail

- Government

- Healthcare

- Others

By Geography

- United Kingdom

- Germany

- France

- Italy

- Spain

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of EMEA

Table of Contents

1. INTRODUCTION

1.1. Market Definition

1.2. Market Segmentation

2. RESEARCH METHODOLOGY

2.1. Research Data

2.2. Assumptions

3. EXECUTIVE SUMMARY

3.1. Research Highlights

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Porter's Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of New Entrants

4.3.4. Threat of Substitutes

4.3.5. Competitive Rivalry in the Industry

4.4. Value Chain Analysis

5. EUROPE, MIDDLE EAST AND AFRICA (EMEA) DATA CENTER BLADE SERVER MARKET BY DATA CENTER TYPE

5.1. Introduction

5.2. Tier 1

5.3. Tier 2

5.4. Tier 3

5.5. Tier 4

6. EUROPE, MIDDLE EAST AND AFRICA (EMEA) DATA CENTER BLADE SERVER MARKET BY SERVICE

6.1. Introduction

6.2. Consulting Services

6.3. Installation & Deployment Services

6.4. Support & Maintenance Services

7. EUROPE, MIDDLE EAST AND AFRICA (EMEA) DATA CENTER BLADE SERVER MARKET BY ORGANIZATION SIZE

7.1. Introduction

7.2. Large Enterprises

7.3. Medium Enterprises

7.4. Small Enterprises

8. EUROPE, MIDDLE EAST AND AFRICA (EMEA) DATA CENTER BLADE SERVER MARKET BY VERTICAL

8.1. Introduction

8.2. IT and Telecom

8.3. Manufacturing

8.4. Media and Entertainment

8.5. Banking, Financial Services, and Insurance (BFSI)

8.6. Retail

8.7. Government

8.8. Healthcare

8.9. Others

9. EUROPE, MIDDLE EAST AND AFRICA (EMEA) DATA CENTER BLADE SERVER MARKET BY GEOGRAPHY

9.1. Introduction

9.2. United Kingdom

9.3. Germany

9.4. France

9.5. Italy

9.6. Spain

9.7. Saudi Arabia

9.8. United Arab Emirates

9.9. South Africa

9.10. Rest of EMEA

10. COMPETITIVE ENVIRONMENT AND ANALYSIS

10.1. Major Players and Strategy Analysis

10.2. Emerging Players and Market Lucrativeness

10.3. Mergers, Acquisitions, Agreements, and Collaborations

10.4. Vendor Competitiveness Matrix

11. COMPANY PROFILES

11.1. Dell Technologies Inc.

11.2. Cisco Systems, Inc.

11.3. Huawei Technologies Co., Ltd.

11.4. International Business Machines Corporation (IBM)

11.5. Lenovo Group Limited

11.6. Inspur Electronic Information Industry Co., Ltd.

11.7. Fujitsu Limited

11.8. NEC Corporation

11.9. Hewlett Packard Enterprise (HPE)

Navigate

Trusted by the world's leading organizations